All posts by Robert Wright

Five long term global trends and implications for markets

By Robert Wright /March 07,2023/

This article looks at some longer term structural trends in the economy and their impact on economic growth and investments.

1. A decline in routine based jobs

Fear of technology replacing jobs has been around for years, although concern around this risk appears to have waned in recent times, as impacts of the pandemic on labour markets has taken focus. New technology is constantly displacing some jobs but it is also creating new ones in its place. The jobs most at risk are routine based jobs, because this type of work can be replicated, learned and taught by machinery and automatic intelligence. In Australia, there has been a long term decline in manual and cognitive routine based jobs. In the late 1980s, routine manual jobs were 40% of the workforce and are now around 26% of the workforce while routine cognitive jobs were 26% of the workforce in the late 1980s and are now worth 19% (see chart). Similar medium term trends are evident across other developed countries. Non routine jobs (either manual or cognitive) are less at risk of being displaced by technology because they are harder to replicate and often need a human element (for example in jobs related to health, childcare or teaching). Problems in recent years with self driving cars also shows the difficulties associated with technology.

Middle income households tend to be most susceptible to routine based jobs so this trend will increase inequality and could put downward pressure on wages growth in the long run. The OECD (Organisation for Economic Co-operation and Development) in a report done in 2018, estimated that around 14% of jobs (in the OECD) are at high risk from automation, with large variations across countries (countries at higher risk include Slovakia, Slovenia, Greece and Spain while the countries at the lowest risk include Norway, Australia, Finland and Sweden). The workforces that are more at risk tend to have a lower educated workforce, a weak tradeable services sector and have a low urbanisation rate. In Australia, around 7% of jobs are estimated to be at high risk of automation and in the US its slightly higher at 10%. The government has a role to play in ensuring that the transition to new types of employment for impacted employees is managed through training programs, appropriate university curriculum and ensuring that funding is targeting those areas at the highest risk of job losses due to automation.

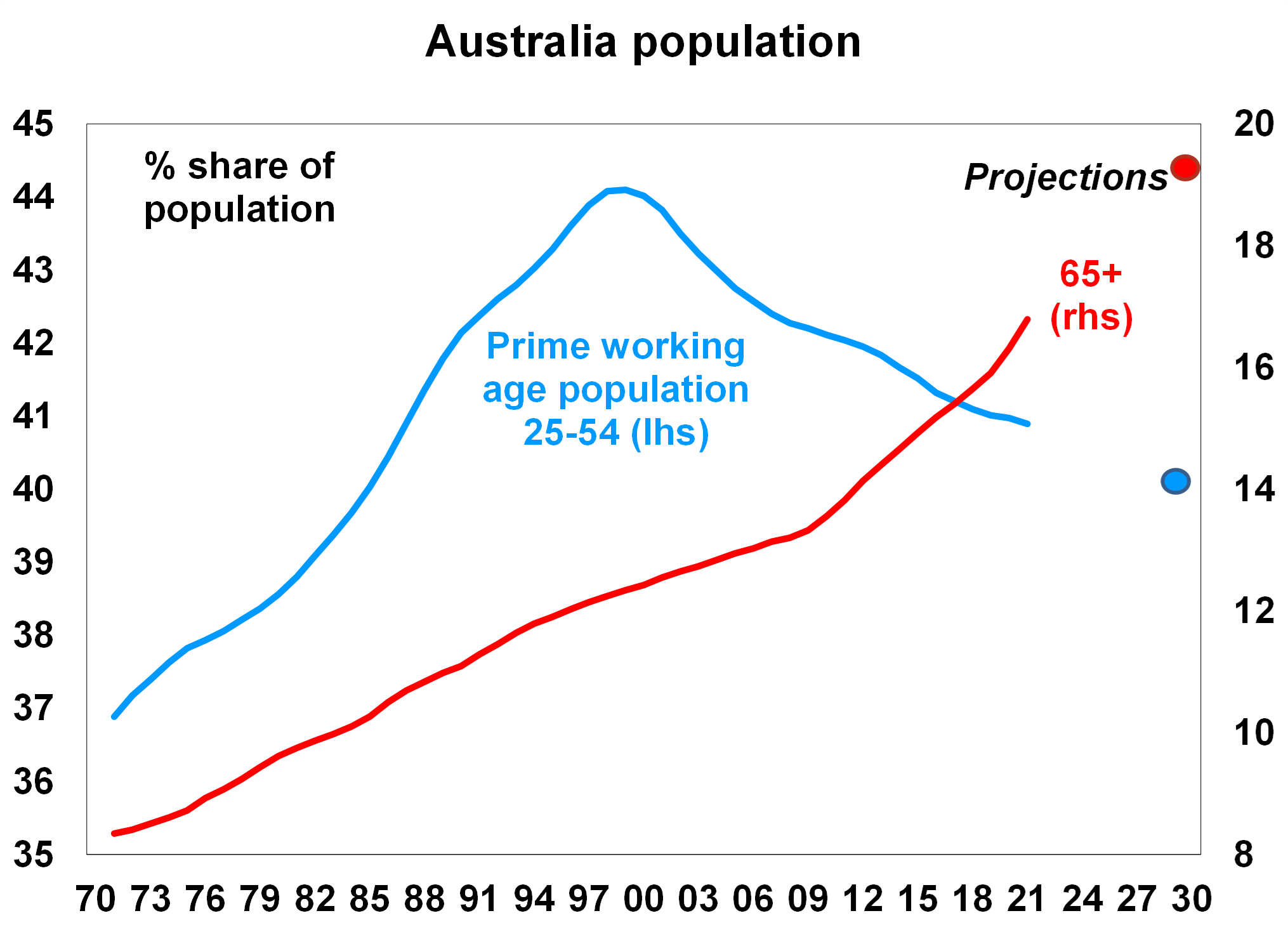

2. An ageing population and an increase in the ‘dependency ratio’

The global population, especially in major developed countries, is ageing which has been a long term trend as the birth rate has declined. In Australia, the share of the prime working age population (those aged between 25-54) peaked at 44% of the population in 1999 and has been falling slowly since then, currently at around 41% and projected to be around 40% by the end of the decade. In contrast, the share of the population that is aged 65+ is expected to keep climbing to just under 20% by 2030, up from 17% now (see chart). An ageing population will put upwards pressure on the ‘dependency ratio’ (the sum of those aged under 15 and over 65 as a share of the whole population) which will detract from national savings (people who work increase savings while the very young and old drain savings) which is inflationary in the long term.

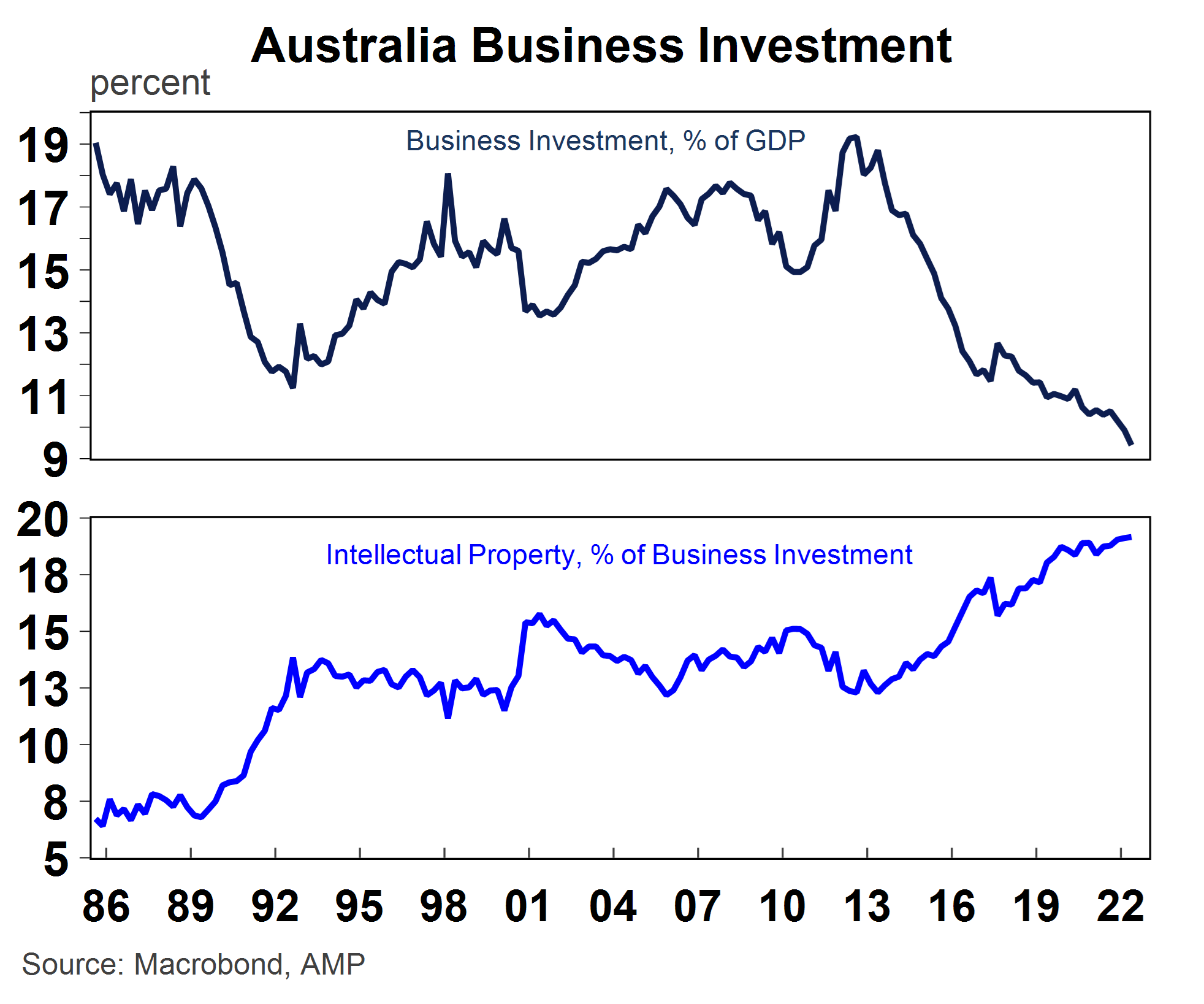

3. A decline in business investment as a share of GDP but a lift in intellectual property as a share of investment

In many developed countries, private business investment is declining as a share of the economy, in place of a rising services sector which is less investment intensive. In Australia, business investment often goes through cycles because of the dominance of the mining sector (at its peak mining investment reached 11% of GDP). After the last mining investment boom (which ended in 2012 after business investment was 19% of GDP), investment has been on a gradual decline and is now 9.4% of GDP (see chart). While there may be ups and downs in the cycle from the mining investment contribution and the usual wear and tear associated with depreciation, private business investment is likely to decline further as a share of GDP because of the changing nature of business investment. The typically large scale buildings and structures, machinery and equipment type of investment is being replaced with less ‘heavy’ types of investment, like intellectual property with the rising importance of the tech sector in all industries. A less capital intensive economy could weigh on long run productivity growth, although the impact is probably marginal as intellectual property investment should still boost productivity growth.

4. A multi polar world means more geopolitical risks

The US economy has been increasing in importance to the global economy since the end of the Second World War. The rising significance of the US economy to global trade, cultural influences, military presence and economic power has been increasingly consistent with a unipolar world, especially as the United Kingdom and the Eurozone have had challenging economic conditions in the past decade.

However, the balance of power has been shifting in recent years as the Chinese economy grows and becomes a larger share of the global economy (see chart). In purchasing power parity (PPP) terms (which adjusts individual country prices into a global comparison after accounting for exchange rates and purchasing power in each country which allows a better sense of living standard comparison) the Chinese economy is already the largest in the world (at 19% versus the US at 16%). If we also account for India then China and India make up 26% of the global economy compared to the US, UK and the Eurozone at 27% (in PPP terms). But we are currently at a crossroads, with China and India about to take over as a larger share of the global economy. On our estimates China and India will be 34% of the global economy by 2045, versus 22% for the US, UK and Eurozone (if growth rates continue at its current pace). As a result, the global economy is increasingly moving towards a multi-polar world as the balance of power shifts away from the US. This shift in the balance of power will keep geopolitical tensions and risks high over coming years as the US and China compete for global control, particularly in the technological space. Investors should be prepared for periodic inflammations in geopolitical tensions and heightened risks of conflict or war, keeping volatility in share markets high. Concerns over the growing Chinese economy are expected to again be a feature of both the Democratic and Republican party campaigns in the 2024 US Presidential election. However, in Australia, the relationship with China looks to be improving with a recent meeting between Australian PM Albanese and China’s President Xi Jinping seemingly the most positive in years.

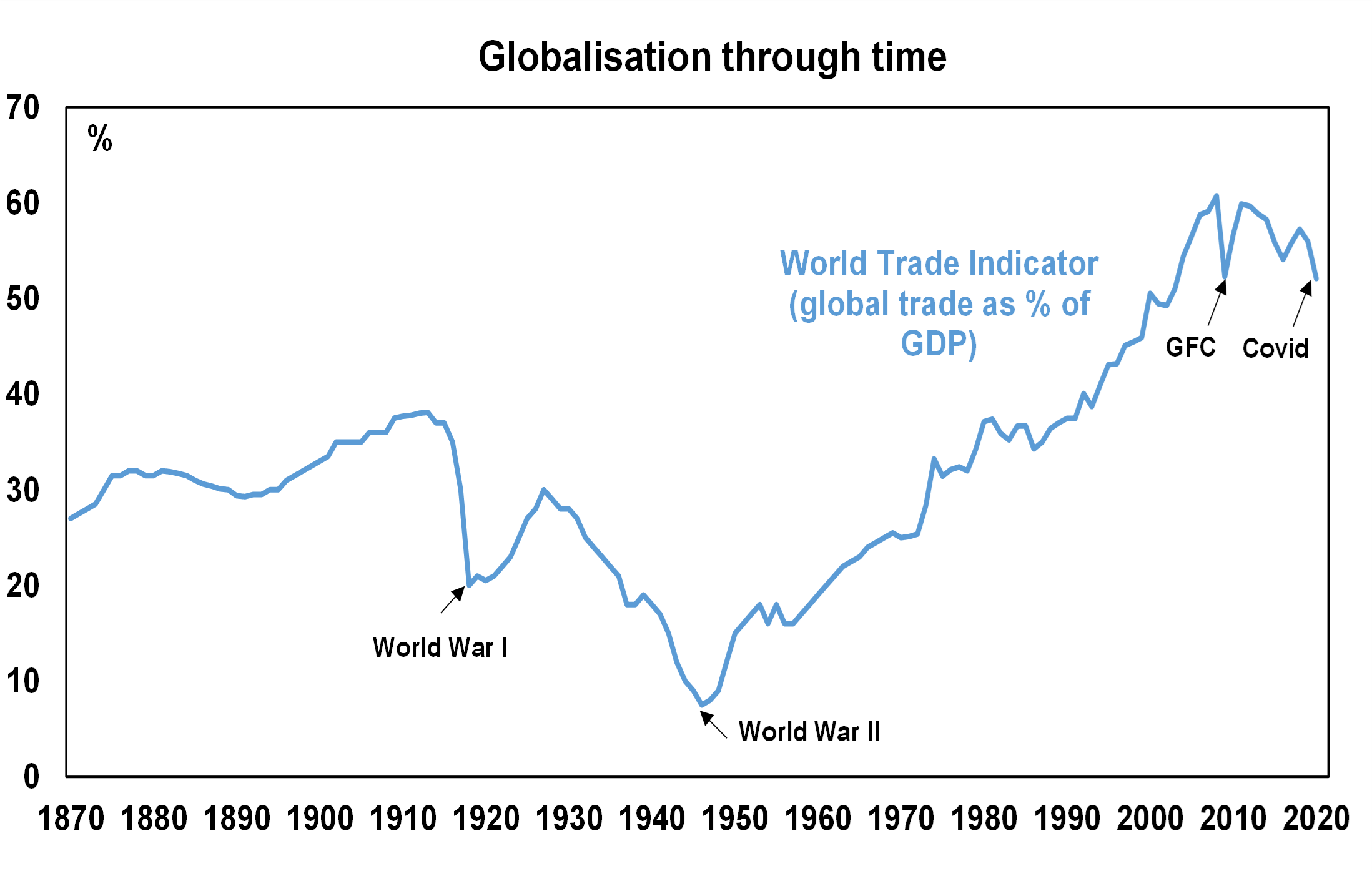

5. Peak globalisation is inflationary

Globalisation looked to be reaching a peak before COVID-19 broke out, with global trade (the sum of exports and imports) declining as a share of GDP since the Global Financial Crisis in 2008 (the chart shows that global trade was 56% of GDP in 2019, below its peak of ~61% before the GFC), as countries decided to become more self-sufficient after seeing the contagion impacts of the GFC. COVID-19 dealt another blow to global trade as closed borders and transport delays led to a push towards bringing as much production onshore as possible, or at least to closer countries (‘nearshoring’ or ‘friendshoring’). Given that globalisation was disinflationary because production was transferred to countries to the most efficient producer (which most often ended up being the lowest cost producer) some reversal in the globalisation trend will be more inflationary for the global economy.

Source: AMP

Why investing for retirement is different

By Robert Wright /March 07,2023/

When you’re still employed and earning a salary, there’s money coming in you can rely on. In retirement, in the absence of a regular salary you’ll need to find a new way to secure enough income to cover your living costs.

Investing your money is one way to make the most of your savings and provide an income in retirement but if you’re expecting savings and investment earnings to help cover your expenses, it’s important to get your strategy right.

Why timing matters

When accumulating super for retirement, you can afford to be patient. With years ahead to top up your super, you can stay invested during falls in the share market and wait for markets and your assets to bounce back. For the few years just before and after retirement, it’s a different story. This period, known as the ‘retirement risk zone’, is the time when you have most to lose from a fall in the value of investments. Your super has likely reached its peak in value and you want to make the most of these savings for your future retirement income.

In order to protect your savings and provide you with income throughout your retirement, it’s important to be aware of three key risks:

1. Living longer

Australians are living longer than ever before. Life expectancy has grown by more than 30 years in the last century1. Living off retirement savings for 20-30 years or more introduces the very real risk of running out of money. So it’s no wonder more than half of Australians aged 50+ are worried about outliving their savings according to a 2019 National Seniors Australia survey.

We’re lucky that we live in a country that if your retirement savings run out; the Age Pension is there as a safety net but these regular payments may not be enough to maintain the lifestyle you’ve been enjoying in retirement. You could also be left with limited funds and options for aged care, if you should need it. That’s why it’s so important to make a financial plan early in your retirement so that you can help to protect your income now and in the future.

2. Inflation

Inflation measures the change in the cost of living over time and represents an important and often underestimated risk to your financial security in retirement. Given your retirement could last 20 plus years, there’s a good chance your savings and income will be affected by inflation. At an average annual inflation rate of 2.5%2, a dollar today is worth roughly half what it was 25 years ago. Even this modest year on year rise in the price of goods and services can put you at risk of having an income that no longer covers your living expenses from year to year.

3. Share market performance

Share market performance is a risk for investors with exposure to investments such as shares, bonds and commodities. If you’re worried about market collapses similar to the Global Financial Crisis (GFC) in 2008, you’re not alone. A 2018 National Seniors Australia survey found that 7 out of 10 older Australians share your concerns.

Falls in the value of investments are impossible to predict and can make a big difference to income and financial security throughout your retirement. When investments earn negative returns, your retirement savings are falling in value. Crucially, if you also need to make regular withdrawals to pay for living expenses, it’s a twofold blow for your overall financial position in retirement. Less savings now means more potential for outliving those savings later in life.

Protecting your income and future in retirement

Diversifying your investments – balancing growth and defensive assets for example can limit the impact of market risks and inflation on your retirement savings. However, even with a well diversified portfolio, your super and Age Pension may not provide you enough income for your entire retirement. If you’d like the peace of mind that comes with a regular income for life, a lifetime annuity might be right for you.

Using a portion of your savings or super, you can invest in a lifetime annuity and receive regular income payments for life. It can act as a safety net ensuring that you will receive income for life, regardless of how long you live.

Talk to an adviser about the benefits of a lifetime annuity and whether it might be right for you.

[1] Australian Bureau of Statistics, Life Expectancy improvements in Australia over the last 125 years, 18 October 2017.

[2] Australian Bureau of Statistics, 70 years of inflation in Australia, Andrew Glasscock, 2017. Fig 2.

Source: Challenger

What are asset portfolios?

By Robert Wright /March 07,2023/

Building your wealth for the long term starts with a sound investment strategy; but with so many options outside your superannuation fund, from bonds to managed funds, where should you begin?

Understand your risk profile and timeframe

Almost every type of investment comes with some level of risk. There’s a risk you could lose money, as well as the possibility your investments won’t achieve your financial goals within the timeframe you need. As a general rule, the higher the risk the greater the potential return and the longer you should consider keeping that investment.

So first you need to understand what type of investor you are and recognise that this may change as you get closer to retirement.

When time is on your side, you may decide you can afford to take some calculated risks with your investment portfolio. That might place you at the ‘aggressive’ or ‘moderate to high growth’ end of the risk profile spectrum but if you’re planning to scale back on paid work soon, you may feel more ‘defensive’ or ‘conservative’ with your investment approach, to protect the value of the capital you’ve already built up.

To work out your risk profile, think about how you feel about short term fluctuations in the value of your investments. Would it keep you awake at night or would you be comfortable riding it out?

A market correction when you’re close to retirement could have a disproportionate impact on a larger portfolio so it’s also worth considering two risk profiles, one for your superannuation and one for your other investments.

What are asset classes?

An asset class is a type of investment – broadly speaking, these are cash, fixed interest, property or shares. Each has a different level of risk and return.

| Cash (defensive asset) | Fixed interest (defensive asset) |

| Investing in cash (such as term deposits) provides stable, low risk income (usually as interest payments). Traditionally, around 30 percent of assets are held in cash and term deposits[1]. It’s a good idea to have some cash available at short notice and these investments usually have a short timeframe. | Investing in government or corporate bonds, mortgages or hybrid securities operate like a reverse loan – they pay you a regular interest payment over a fixed term. You usually hold fixed interest investments for one to three years. |

| Property securities (growth asset) | Australian and international shares (growth asset) |

| You can invest in property that is listed on share markets, including commercial, retail, hotel and industrial property. The potential returns can be medium to high but you may need to hold these investments for three to five years. | Shares (or equities) give you a part ownership of an Australian or international company. Your potential returns include capital growth (or loss) and income through dividends, which may be franked. Depending on the type of share, these are considered medium to high growth assets and you may need to hold them for up to seven years. |

All about diversification

Spreading your investments across a range of assets to reduce your risk is known as diversification – basically it lets you avoid putting all your eggs in one basket.

Diversification can reduce the volatility within your portfolio and the risk of a large drop due to any market downturn. Given it can also take time to sell certain investments (such as property), it’s smart to have short term as well as long term investments within your portfolio. There are no guarantees – diversification won’t fully protect you against loss but it can even out your returns.

Other ways to invest in shares

Investing in a managed fund gives you access to different equities, bonds and other assets, with a focus on a specific investment objective. Pooling your money with a group of investors lets you invest in opportunities that would otherwise be out of reach and diversify your risk. There are many different types of managed funds, with different risk profiles and investment approaches, including single sector or multi sector funds or index funds.

Review your investments regularly

It’s important to keep an eye on your investments to make sure your portfolio is balanced and you’re on track to meeting your financial goals. If you invest in a managed fund, you may only need to review it once a year. If you are investing directly, you’ll need to monitor market changes much more frequently.

It’s also worth getting advice from a financial adviser before you change your investment allocation, as selling assets may result in a tax liability. They can also give you an independent perspective on your investment goals and risk profile.

Source: Colonial First State

[1] http://www.afr.com/personal-finance/why-its-time-to-rebalance-your-portfolio-20160321-gnnbrt

Can super secure a woman’s future?

By Robert Wright /March 07,2023/

Here are some stark numbers on the difference between men and women at the point when they retire:

- 80% of women are retiring without the super balance they need to fund a comfortable lifestyle.

- On retirement, women’s average superannuation account balance is around $70,000 less than men.

To be balanced, we should remember there are many situations where the shortfall in a woman’s super balance is offset by them sharing their partner’s super but that assumes away a lot of life possibilities – particularly divorce and the early death of a male partner – and also a woman’s sense of financial independence.

Women also live longer than men. A woman who was 45 in 2020 could expect to live till 86 – that’s three years longer than her male counterpart. So female retirees are more exposed to the dreaded FORO – fear of running out.

Why the shortfall?

Why do women have less super than men? There are multiple often intertwined answers.

More women work in low paid fields like hospitality and care services. They’re also more likely to work part time. That’s one reason the lockdowns of the past two years did more damage to female balance sheets.

Many women take time out of the workforce to have children and act as principal caregiver, especially during the early years of their children’s lives. The ASFA (Association of Superannuation Funds of Australia) estimates women accumulate a ‘super baby debt’ of up to $50,000 – they have $50,000 less in their super because they’ve prioritised children. Compulsory super is based on a percentage of your earnings being saved for retirement. So the less you earn over your lifetime the less you save.

Women are also more likely to have time away from work to care for their parents. If Generation X is the ‘squeezed generation,’ looking after the generation before and after, then Generation X women may be the ones squeezed hardest.

Expanding knowledge, shrinking the gap

Closing the knowledge gap is nearly as important as closing the contribution gap.

The first step is understanding where you stand – so checking with your super fund or adviser to understand exactly how much super you have and how much you’ll need to support a comfortable lifestyle.

Many super fund managers have easy to use calculators that answer those questions. For a rule of thumb, ASFA suggests single people need $545,000 in retirement savings to fund a comfortable retirement. Couples need around $640,000. Obviously these numbers are only guides and assume that you fully own your own home at retirement. It’s important you consider your own situation and expectations.

The calculators we discuss above can give you an individual view of the return difference between different investment strategies. Historically, funds that invest more aggressively (i.e. with more in shares and property and less in cash) have tended to outperform over the long term* and that means more money to retire on.

The more you put in…

Women seeking to set themselves up for a truly comfortable retirement need to first get a handle on their super and their retirement objectives, then accustom themselves to taking a little more risk in the investment strategy.

Given that it’s highly tax effective, many would argue that women should be pouring as much money into super as they can afford. Obviously that decision is a highly personal one that must take account of a whole range of factors. Fortunately, Australian governments, left and right, are committed to making super work, so there are some excellent strategies women of all income levels can use to get more gold into their pot. Here’s a very concise look at some of those opportunities.

How you can retire with more

1. Make additional contributions

Simply put, women who are likely to take time out of work should weigh up the benefits of putting more money into super when they can to build up a retirement savings buffer.

Firstly, make sure your employer is contributing in line with their Superannuation Guarantee responsibilities – currently, they need to contribute 10.5% of your income to super on your behalf. (There’s a cap of $27,500 a year on these so called concessional contributions). You can also make salary sacrifice contributions, where you forgo income and direct it into your super. Those contributions also count towards the $27,500 limit.

If you don’t reach the cap in a given year, you can accumulate those unused portions for up to five years. When you have the funds available you can then ‘catch up’ by investing up to your annual $27,500 cap and any unused cap from previous year(s). You can’t use this catch up approach if your super balance is over $500,000 but for many women it’s an excellent way to consider adding to their super even if they’ve had a few years out of the workforce or on part time income.

2. Bring forward contributions

You can also make non-concessional contributions of up to $110,000 a year into your super. These are contributions you make after tax, for example from your savings. For younger women in high paying jobs, putting extra money into super, perhaps by investing a bonus, inheritance or proceeds from a property sale – may be an effective way to load up your super. Or if you do it later in your career, it’s another way to catch up.

The government also allows you to ‘bring forward’ some contributions investing up to three times the annual non-concessional contribution in one year – that’s $330,00. Again, if you have the funds, it may be a good way to make a focused push at increasing your super balance. As of July 2022, this option is available to any women under 75 (previously it was 67). So even women very close to retirement can use this strategy to improve their super situation.

3. Spouse contributions

Couples working together on their super strategies can make up for some of the inherent disadvantages women face when saving for retirement.

Spouse contributions can be part of that approach. They allow one member of a couple to contribute up to $3,000 into the super fund of their spouse and receive a tax offset of up to $540 for doing so. The offset works on a sliding scale depending on the income of the ‘receiving’ spouse. To get the maximum offset the receiving spouse must earn less than $37,000 and there’s no offset once they earn over $40,000, but for many women, beefing up their super via extra contributions may be even more valuable than a tax offset.

Playing as a team

Couples that work together to accumulate the maximum possible super balance can have more flexibility and options in retirement.

One way couples can do this is through managing their individual $1.7 million super balance cap. The cap limits the amount of super you can transfer into a tax-free retirement income stream such as a super pension or annuity.

A twisty path to a beautiful place

As you can see from this list of contribution strategies, there are numerous ways in which women can maximise their super balance and therefore improve their chance of a comfortable retirement lifestyle. But there are also a plethora of limits, caps and complexities to navigate.

*Past performance is not indicative of future performance.

Source: Perpetual