All posts by Robert Wright

Federal Election 2025

By Robert Wright /May 23,2025/

During the Federal Election campaign, the Government made a number of election promises, which may impact your finances. There were also a number of support measures proposed in the recent Federal Budget. What could this mean for you?

These announcements are proposals only and may or may not be made law. The information below, including the policy details and proposed start dates, is based on the information announced as at 5 May 2025. You should speak to your financial adviser to discuss how these proposals could apply to you.

Election promises

Taxation

$1,000 instant tax deduction for work-related expenses, proposed from 1 July 2026.

What’s proposed?

Taxpayers who have eligible work-related expenses may be able to claim a tax deduction of up to $1,000 without having to keep individual receipts. It will still be possible to claim work-related expenses above this limit, however evidence will be needed.

Who could benefit?

The deduction will be available to people with ‘labour income’. This doesn’t include income from running a business or from investments, where the usual rules will continue to apply.

$20,000 small business instant asset write-off extension, proposed from: 1 July 2025 to 30 June 2026.

What’s proposed?

The higher instant asset write-off threshold of $20,000, which currently applies until 30 June 2025, is proposed to be extended for another 12 months until 30 June 2026. The threshold is available for more than one asset. Eligible businesses can continue to place assets valued at $20,000 or more into a depreciation pool, where a deduction of 15% can be claimed in the first income year and 30% thereafter.

Who could benefit?

Small businesses with an aggregated annual turnover below $10 million will be able to claim an immediate tax deduction for the full cost of eligible assets costing less than $20,000 that are first used or installed ready for use by 30 June 2026.

Help for home buyers

Expanded ‘Help to Buy’ scheme, proposed from: to be confirmed.

What’s proposed?

The Government has proposed to expand access to the Help to Buy scheme to more home buyers by increasing the property price caps and income test thresholds, which determine eligibility to participate in the scheme.

The scheme is a shared equity scheme, which allows eligible home buyers to purchase a home with a smaller deposit, of as little as 2%. The Commonwealth will contribute up to 30% of the purchase price of an existing home and up to 40% of the purchase price of a new home.

The Help to Buy scheme is expected to open for applications later this year. Although the Federal Government has legislated the scheme, the States and Territories need to pass legislation for it to operate in each jurisdiction.

Who could benefit?

Increasing the income cap and property price caps will enable more people to participate in the scheme.

For singles, the income cap will increase from $90,000 to $100,000. For joint applicants (and single parents), the income cap will increase from $120,000 to $160,000.

The property price cap will depend on the location of the property and details can be found in the Government’s media release.

Participants must meet a number of eligibility rules and conditions, including repaying the Government when the home is sold or when certain changes occur in their circumstances. So it’s very important to understand the rights and responsibilities of participating in the scheme before making an application.

Previously announced measures

Cost of living support

The below proposals were announced by the Government in the March 2025 Federal Budget.

Energy bill relief extended for six months, proposed from: July 2025.

What’s proposed?

The Government will provide further energy rebates in addition to the bill credits people have received since July 2024. The rebate will be applied automatically to electricity bills between 1 July and 31 December 2025, in two quarterly instalments of $75.

Who could benefit?

All Australian households and eligible small businesses will receive the additional energy rebate. It’s expected the eligibility rules that apply to small businesses (quarterly power consumption) will not change.

Lower cap for PBS medicines, proposed from: January 2026.

What’s proposed?

The maximum cost of Pharmaceutical Benefits Scheme (PBS) medicines will decrease from $31.60 to $25 per script.

Who could benefit?

This will benefit people who don’t hold a concession card and would otherwise pay the maximum amount to fill a script. It doesn’t apply if the script is for a medicine not on the PBS, which may cost more than $25. Pensioners and Commonwealth concession cardholders will continue to pay the subsidised rate of $7.70 per PBS script until 1 January 2030. This is an existing measure.

Student loans to be cut by 20%, proposed from: 1 June 2025.

What’s proposed?

Student loans will be reduced by 20% before the annual indexation (at a rate of 3.2%) is applied on 1 June 2025.

Who could benefit?

The changes will benefit all people who have Higher Education Loan Program (HELP) Student Loans, VET Student Loans, Australian Apprenticeship Support Loans, Student Start-up Loans and Student Financial Supplement Scheme, based on their outstanding 1 June 2025 balance.

Importantly, voluntary loan repayments that are processed before 1 June will reduce the loan balance that’s indexed on 1 June. However, the 20% debt reduction will be applied to the 1 June balance. So if this proposal is legislated, before making a voluntary repayment, it’s worth doing the numbers to see if it’s best to make a voluntary repayment before or after the 20% reduction and indexation is applied on 1 June. The table below provides an example which shows the difference between making a $5,000 voluntary repayment before and after 1 June, where the outstanding debt balance is $30,000.

| Outstanding debt today | Voluntary repayment before 1 June | Loan balance on 1 June (after 20% reduction and indexation applied)

|

Voluntary repayment after 1 June | Outstanding balance |

| $30,000 | $0 | $24,768 | $5,000 | $19,768 |

| $30,000 | $5,000 | $20,640 | $0 | $20,640 |

Reduced student loan repayment obligations, proposed from: 1 July 2025.

What’s proposed?

The minimum income that can be earned before student loan repayments need to be made is proposed to increase. This is in addition to the standard indexation of the income repayment thresholds which ordinarily happens on 1 July each year. Also, the way repayments are calculated will be changed.

Who could benefit?

People with student debts will benefit from lower compulsory loan repayments in 2025/26 and beyond, if their ‘repayment income’ is above the minimum threshold at which loan repayments need to be made and less than $180,000.

The minimum income threshold is $54,435 in 2024/25 and will automatically increase to $56,156 on 1 July. Also, the Government has proposed:

- increasing the minimum income threshold to $67,000; and

- calculating repayments on just the repayment income earned above the income threshold, not on total income.

The list of qualifying student loans is the same as those to be eligible for the 20% debt reduction on 1 June 2025 (see above).

Expanded ‘First Home Guarantee’ program, proposed from: to be confirmed.

What’s proposed?

Help will be extended to all first home buyers under the Commonwealth’s First Home Guarantee Scheme. The scheme enables home buyers to purchase their first home with as little as a 5% deposit. The Government provides a guarantee for the remaining portion of the deposit (up to 15%), to ensure the first home buyer doesn’t pay Lenders Mortgage Insurance.

Currently, income limits and property price caps apply and access is only granted to a maximum of 10,000 eligible participants each year. These requirements are proposed to be removed, opening the scheme to all first home buyers.

Who could benefit?

The extension of the scheme may help first home buyers to purchase their first home sooner. It’s important to understand that purchasing a home with a smaller deposit may increase the total interest that is paid over the life of the loan.

Superannuation

The below measure was initially announced by the Government in 2023, with support reconfirmed in the 2023 Federal Budget. Legislation was introduced to Parliament to make this change law in 2024 but lapsed when the election was called. The Government will need to reintroduce and pass legislation in Parliament before this change can take effect. Given the complexity of the policy and the number of days that Parliament may sit between now and 1 July, we don’t know if the proposed start date will change if the policy is reintroduced.

Higher taxes for balances over $3 million, proposed from: 1 July 2025.

What’s proposed?

Where people have more than $3 million in super (both accumulation and retirement values) from 1 July 2026, higher taxes are to be paid on investment earnings, with payment due in the 2027 financial year.

Currently, investment earnings within the ‘accumulation phase’ of superannuation are taxed at a maximum rate of 15%. With a ‘retirement phase income stream’, such as an account-based pension once retired, investment earnings are generally tax free.

It’s proposed that from 1 July 2025, where a person has a ‘total super balance’ exceeding $3 million at the end of the financial year, an additional tax of 15% will apply to a portion of the investment earnings. The new tax will be called ‘Division 296 tax’, as that is the name of the relevant section of tax law where the proposed rules are covered.

Additional tax won’t be paid where the total super balance is less than $3 million on 30 June 2026 (the end of the first year it will apply) or the end of any following financial year.

Where to from here?

It’s important to remember these changes need to be legislated to become law. The information above is based on the announcements made to date, and there may be changes to the start dates or other details if the policies are formalised. You should speak to a financial adviser to understand more about what has been announced and how these changes could apply to you.

Source: MLC

The absurdity and calamity of US tariff policies

By Robert Wright /May 23,2025/

US tariffs are poorly designed, badly implemented and are already damaging both the US and global economies. The economic damage will only get worse as uncertainty further undermines business and consumer confidence and results in dislocation of global supply chains.

Determining the extent of economic damage, and financial market implications, is difficult because we don’t know what tariffs will actually be implemented or how many backflips there are before then. There’s no clear, defining strategy. The justification for tariffs oscillates between reinvigorating US manufacturing, raising revenue to fund tax cuts, the cost of the US providing global security, the provision of the US dollar to support global trade and financial markets, and broadly addressing an ‘unfair’ trading system. Different justifications would lead to different structures of the tariff regime. Adding to uncertainty, key individuals in the administration have different goals for tariffs.

- The obsession with bilateral trade deficits is baseless

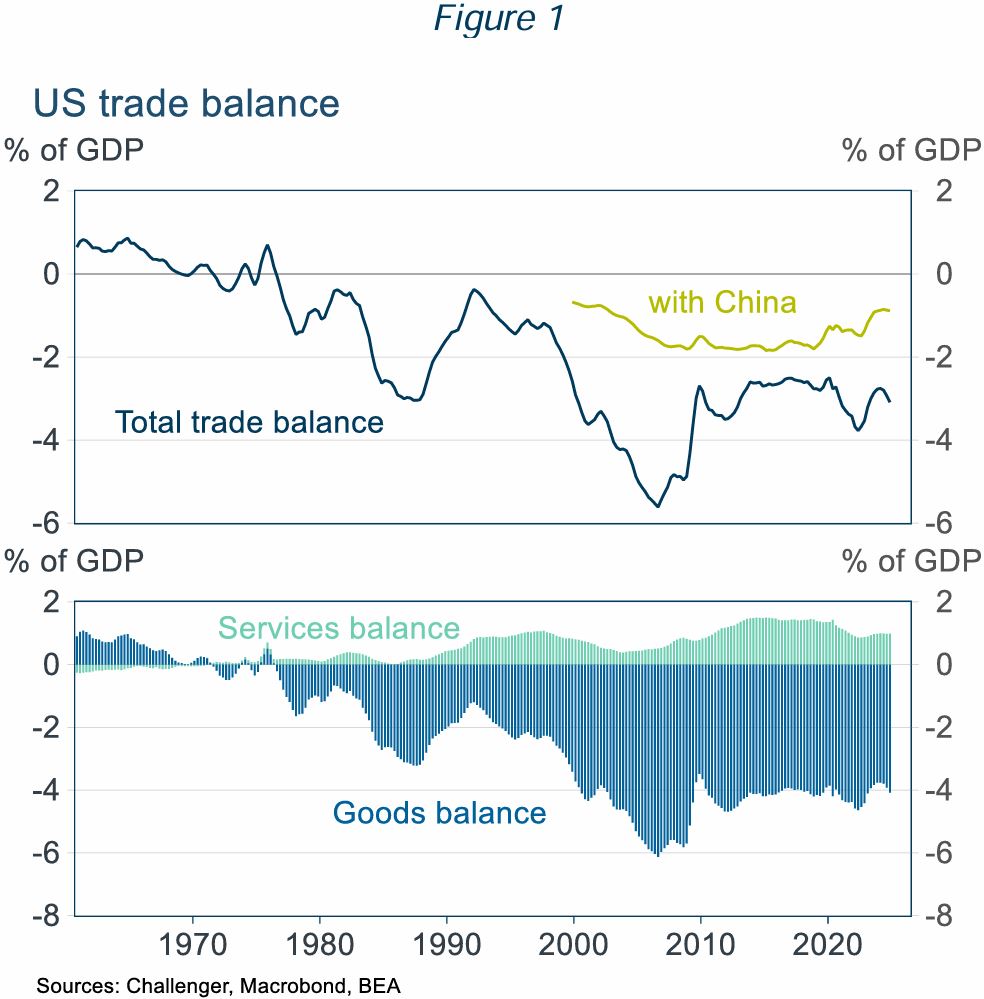

President Trump’s tariff obsession is rooted in a dislike of trade deficits. The United States has run a trade deficit since the mid-1970s (Figure 1). He attributes this deficit to unfair trade policies in other countries and an overvalued US dollar, resulting from US dollar demand given its role in international trade and finance. But the trade deficit also depends on US domestic conditions, notably the US Government’s huge fiscal deficit, currently 5% of GDP.

Balanced national trade doesn’t need bilateral balanced trade

Even if balanced trade at the country level was desirable, there is no reason for this to apply country by country. Even countries with balanced aggregate trade run large trade deficits or surpluses with almost all of their trading partners: Belgium had balanced trade with just two countries; and Canada, Finland, South Korea and South Africa each had balanced trade with just one of their trading partners. Each of these five countries had significant bilateral trade surpluses or deficits with over 150 of their trading partners. The US goal of balanced bilateral trade with every country is, frankly, bonkers.

- The calculation of tariff rates is absurd

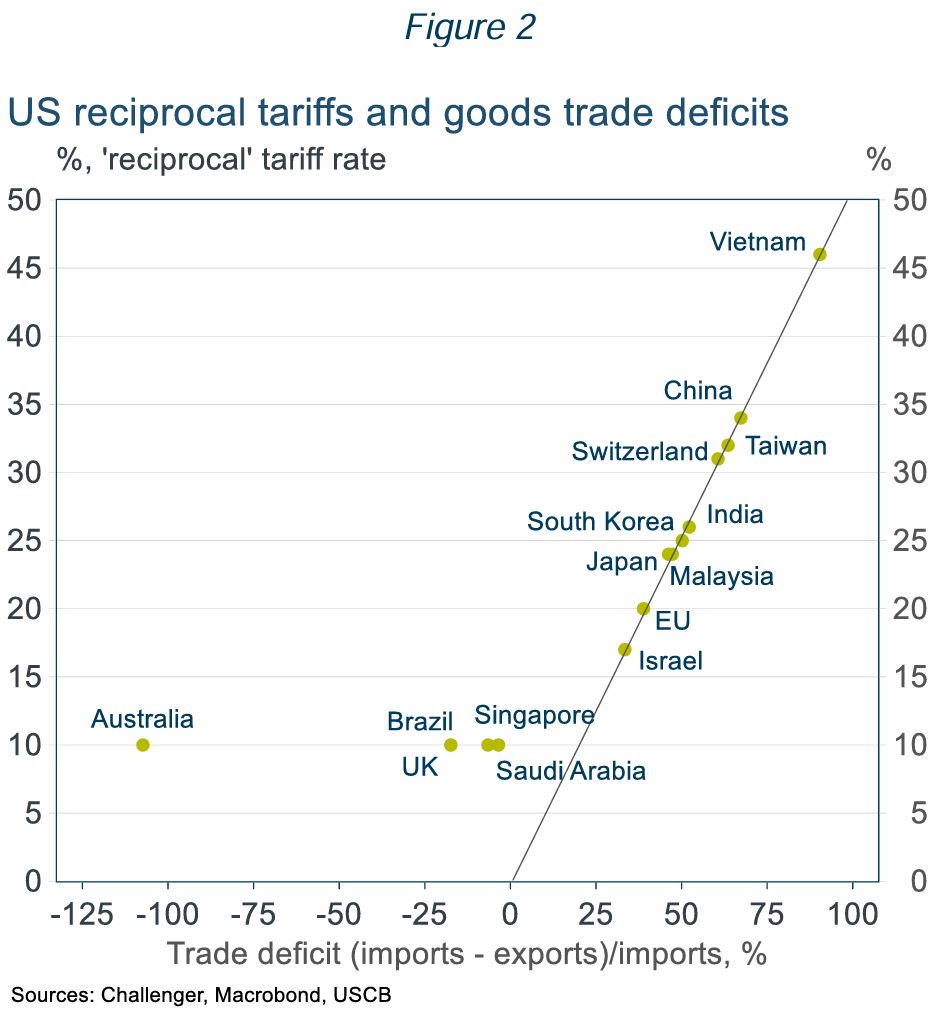

- Bilateral trade balances are meaningless but determine the US ‘reciprocal tariffs’ (Figure 2).

- Even countries the US has a trade surplus with, including Australia get a 10% tariff. If Australia applied the same logic as the US, we’d impose a tariff on the US of around 50%.

- The US has a surplus in services trade of 0.25% of GDP (partly offsetting the goods trade deficit of 1% of GDP; Figure 1) but ignores services trade in its calculation of tariffs.

- The tariffs are badly designed reflecting unclear and inconsistent goals

The US tariff regime has a mix of tariffs on specific goods (steel, aluminium, vehicles) and on specific countries (Canada, Mexico, China and the reciprocal tariffs) reflecting the varied goals of the tariffs. But many of these goals are in conflict. If, as Trump claims, tariffs raise revenue without increasing US prices by forcing foreign suppliers to absorb the tariff, then US manufacturers won’t be more competitive as US prices won’t be higher. And if tariffs are successful in boosting US production, then there would be fewer imports, and so less tariff revenue.

Several bad design elements of the tariffs mean there will be further changes:

- Different tariff rates distort trade for little benefit – for example, Apple intends to ship iPhones to the US from India rather than China as US produced iPhones would be prohibitively expensive.

- High tariffs are being applied to goods the US can’t, or won’t, ever produce – for example, some minerals and shoes (most come from China and Vietnam with 145% and 46% tariffs).

- Tariffs are being applied to inputs used by US manufacturers, increasing exporters’ costs.

- The effective trade embargo with China will be disruptive to the US economy

The 145% punitive tariff applied to China makes most imports from China prohibitively expensive. But the US economy is not ready to disengage from China, which has supplied 13% of US imports. Factories don’t pop up overnight.

Using a fine disaggregation, breaking down goods into their constituent parts, over half of US imports are from China. Alternative suppliers just don’t exist.

For finished consumer goods with very high import shares from China, large price increases and stock shortages will be disruptive to consumers and impact consumer sentiment and support for tariffs. The economic impact will be even greater for those imports predominantly sourced from China that are used as inputs in US production, such as explosives, machinery and various chemicals. For example, China is also a key source for base ingredients used in manufacturing medicines and finished medicines.

- The tariff regime won’t survive its poor design, but tariffs won’t go away completely

The US tariff regime is already unravelling with holes poked in the tariff wall.

- Reciprocal tariffs were paused until 9 July (the baseline 10% tariff still applies to all countries).

- Consumer frustration will mount facing higher prices and product shortages. For example, phones, computers and some other electronics have been exempted from the China tariffs.

- Businesses are getting traction lobbying on the cost to production from tariffs, for example there will be a partial rebate on the 25% tariffs on car parts used as inputs in US manufacturing.

- The US has said some 70 countries want to negotiate tariff reductions. Yet negotiating a detailed trade agreement takes time. The renegotiation of the US-Canada-Mexico trade agreement in President Trump’s first term took 18 months. A rushed negotiation will contain flaws.

However, President Trump strongly believes in the benefits of tariffs for promoting US manufacturing and he needs the revenue. He has committed to using tariffs to reduce income taxes, even musing that income taxes could be eradicated. But a 10% uniform tariff has been estimated to raise just $1.7 trillion over 10 years, a 20% tariff $2.6 trillion. This is substantially less than the estimated cost of $5 to 11 trillion of the tax cuts already promised by President Trump.

- What does the future hold?

There will be many more turns in the road with backflips, reduced tariffs for goods the US won’t produce or needs and new tariffs. There will be ‘deals’ reducing (but not eliminating) individual tariffs with countries committing to reduce trade barriers and import US goods (much of which will never happen).

The pause in reciprocal tariffs, after just one week, was reportedly triggered by the turmoil in bond markets which could have precipitated a financial crisis. Trump has displayed greater resolve in the face of the large fall in equity prices than in his first term. But the risk of a financial crisis, or severe recession, and sharp falls in approval ratings are likely to remain red lines that would result in some pullback.

Challenger expects ongoing tariff uncertainty and hence further volatility in markets. Aggregate tariffs will never get to the levels initially announced, but they will also be much higher than before, reducing US and global growth. Tariffs will add to US inflation, reducing the ability of the Fed to ease. Market pricing is for almost 100 basis points of cuts this year, but there’s a good chance the Fed does not even cut this year.

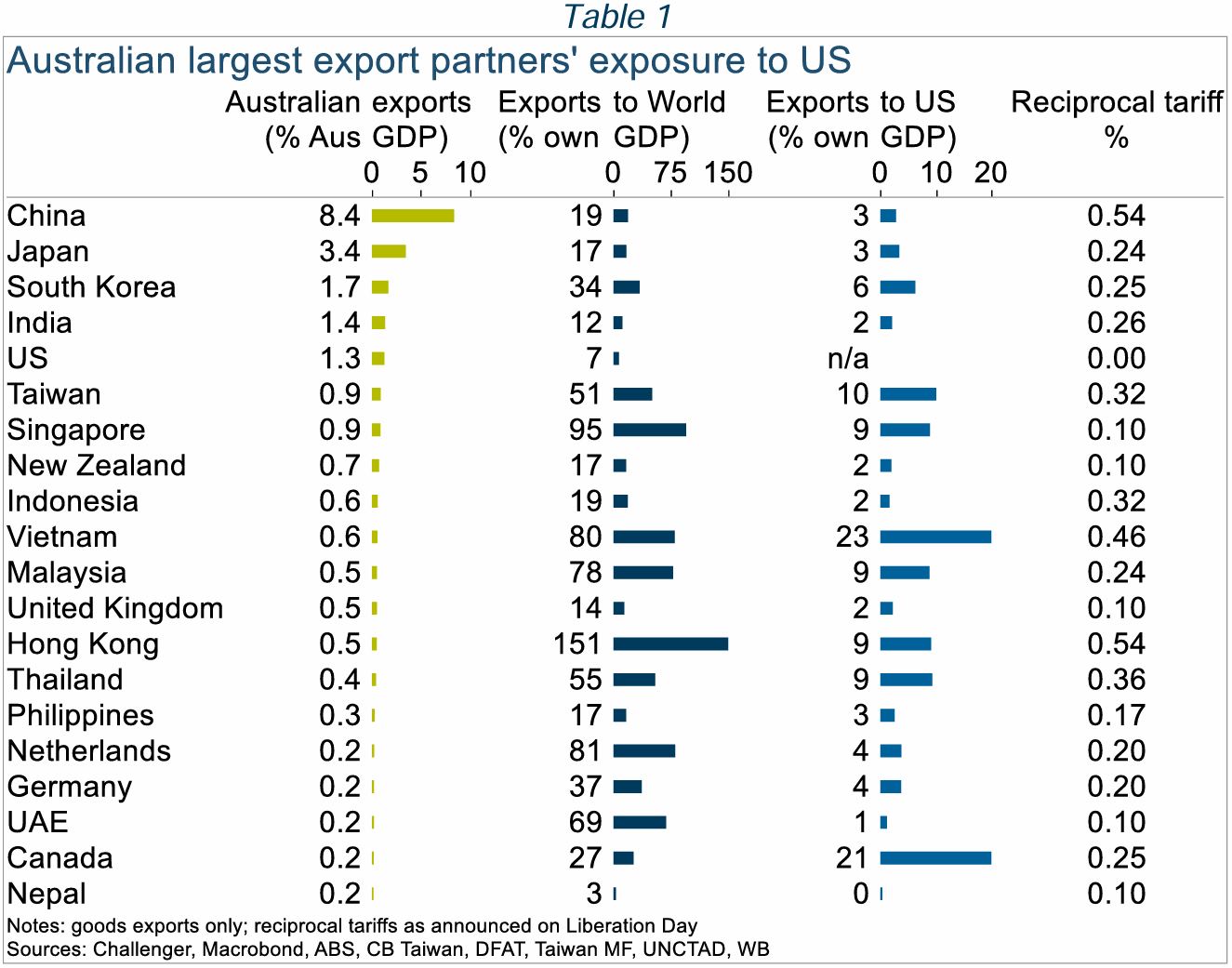

Australia will also see slower growth. We have limited direct exposure to the US economy, but our largest trading partners are more exposed (Table 1). The IMF downgraded its GDP growth forecasts for 2025 by 0.5%. Slower growth, and China’s surplus manufacturing capacity reducing Australian import prices, will lower inflation opening the path to RBA rate cuts. However, market pricing for a cash rate below 3% by December is overdone. With the worst case for US tariffs unlikely to play out, three cuts bringing the cash rate to 3.35%, around its neutral level, seems more likely.

Source: Challenger

Navigating market volatility

By Robert Wright /May 23,2025/

Financial markets have been erratic lately, understandably causing some concern for those of us with super and investments. While dips and major market events are a common feature of investing, markets generally trend upwards over time.

Most super funds invest in sharemarkets to help your money grow over in the long term. So when markets see-saw, so do super and investment balances and returns.

While this can be worrying, it’s important to remember that although the value of investments may go up and down at different times, markets tend to recover and grow over the long term. So it’s important to keep your long-term investment goals in mind.

What’s happened recently?

On 3 April, President Donald Trump announced the US would place tariffs on goods imported into the US from countries around the world. This included a 10% tariff on goods from Australia, which was the minimum rate announced on the day.

Major global economies and markets had been preparing for the announcements, but the tariffs imposed on some countries were bigger than expected. Other countries have also responded by putting similar tariffs on US goods coming into their markets.

As a result, share markets in the US and elsewhere fell sharply in the days afterwards, including the Australian Stock Exchange.

What is a tariff?

A tariff is a tax added to the cost of goods imported from a particular country or countries. It is paid to the government where the goods are being imported.

Tariffs are often used to protect domestic industries by increasing the price of foreign-made competitor products, or to raise revenue.

The cost of those items to the public will generally increase by a similar amount to the tariff.

What does this mean for markets and investments?

The US tariffs are expected to slow global trade and push up the price of some things, which could cause inflation to rise.

This could result in the Reserve Bank of Australia cutting the interest rate several times this year to prevent the economy from slowing down too much.

In the short term, you may see a negative effect on the performance of investments.

Short term volatility in response to political announcements and other geopolitical events is a common feature of investment markets.

While difficult to forecast, history shows us that markets do recover from disruptive influences – for example, from the Global Financial Crisis and the COVID-19 pandemic.

What led to this?

Since Trump’s second presidency began, uncertainty has emerged about US policy in the areas of tariffs, defence and other critical areas of government spending.

In recent months, shares have been quite weak, particularly US technology stocks. This group of stocks was optimistically priced after two years of strong growth, and therefore most at risk of uncertainty in the US market.

This has unsettled businesses amid concerns the US economy could slow. It has also fed into uncertainty in global investment markets, including the Australian sharemarket.

What does this mean for me?

As global financial markets move up and down, the value and returns of your super and investments may also change in the short term.

While this can be concerning, history shows that markets rise over time. So it’s important to keep your long-term savings and investment goals in mind and carefully consider before making any changes to your investment strategy.

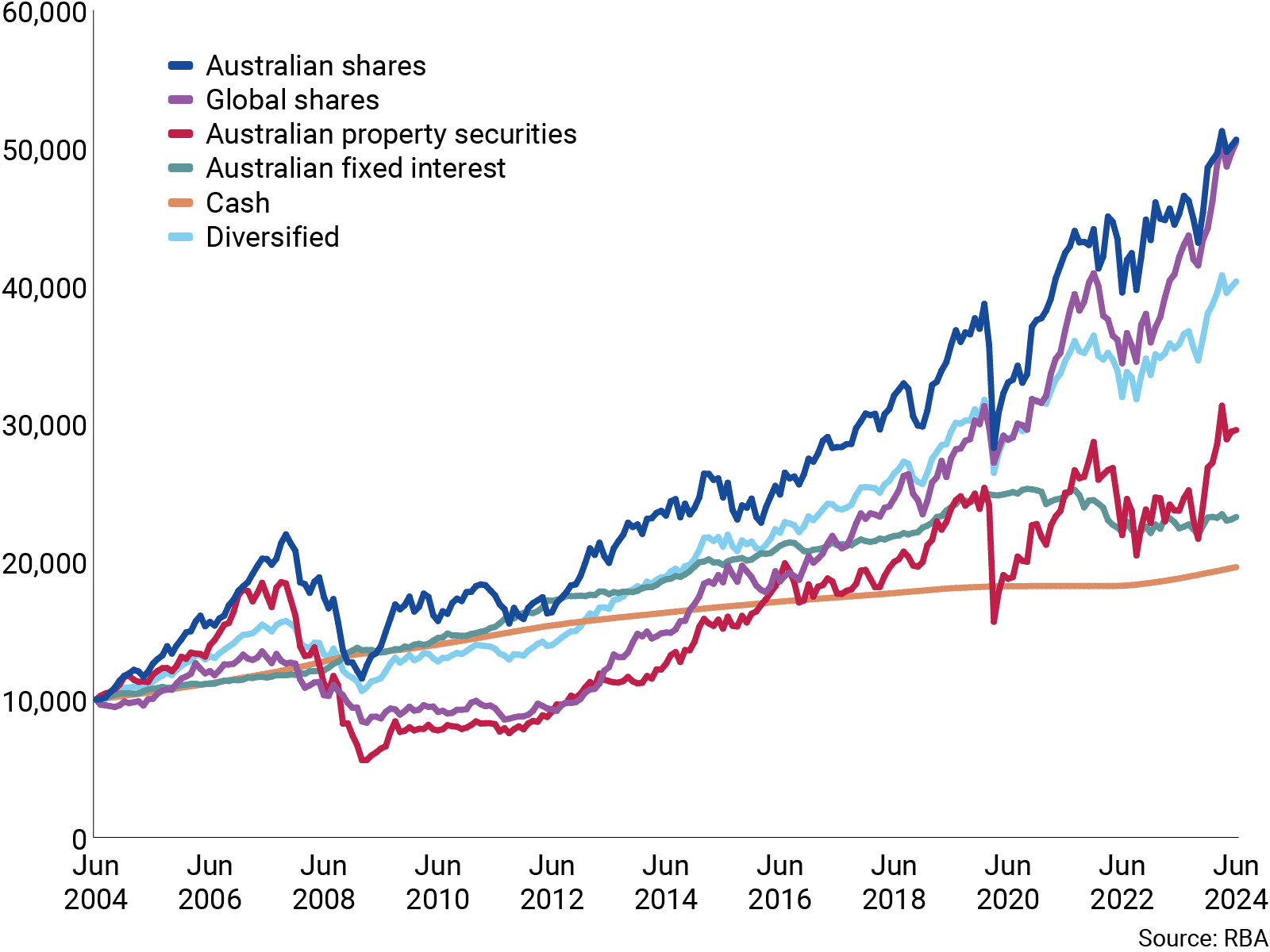

It’s understandable at times like these that some members think about changing how their money is invested. As this chart shows, the long-term trend across major investment types is positive, with shares experiencing more volatility but generating higher returns than more conservative options such as cash.

While past performance is not a guarantee of future performance, historically more time invested in the sharemarket has meant a higher return on investment.

How different investment types have performed over 20 years

It’s also worth noting that investment performance has generally been strong over the past two years, meaning the value of your investments or super may have been relatively high.

Do I need to do anything?

As with any significant market event, it’s best to avoid impulse reactions, but to take a long-term view.

Source: CFS

Spouse super contributions – what are the benefits?

By Robert Wright /May 23,2025/

If your partner is earning a low income, working part-time, or currently unemployed, boosting their super could be a smart financial move for both of you.

When your partner isn’t earning much, or is out of work, their super might not be growing enough to support them in retirement. By contributing to their super, you may not only help them but also enjoy some tax benefits yourself.

We’ll explore how the spouse contributions tax offset works and how it differs from contribution splitting.

The spouse contributions tax offset

Are you eligible?

To be entitled to the spouse contributions tax offset:

- You need to make a non-concessional contribution to your spouse’s super. This means you add money from your after-tax income and don’t claim a tax deduction for it.

- You must be married or in a de facto relationship together and are not living apart or separately.

- You must both be Australian residents.

- Your spouse’s income should be $37,000 or less for the full tax offset, and under $40,000 for a partial tax offset.

- Your spouse is under 75 years of age, and their total superannuation balance is less than the general transfer balance cap ($1,900,000 for 2024-25) as at 30 June of the prior year.

What are the financial benefits?

If eligible, you can generally make a contribution to your spouse’s super fund and claim an 18% tax offset on up to $3,000 through your tax return.

To be eligible for the maximum tax offset, which works out to be $540, you need to contribute a minimum of $3,000 and your partner’s annual income needs to be $37,000 or less. If their income exceeds $37,000, you’re still eligible for a partial offset. However, once their income reaches $40,000, you’ll no longer be eligible for any offset, but can still make contributions on their behalf.

Are there limits to what can be contributed?

You can’t contribute more than your partner’s non-concessional contributions cap, which is $120,000 per year for everyone, noting any non-concessional contributions your partner may have already made.

However, if your partner is under 75 and eligible, they (or you) may be able to make up to three years of non-concessional contributions in a single income year, under bring-forward rules, which would allow a maximum contribution of up to $360,000.

Another thing to be aware of is that non-concessional contributions can’t be made once someone’s super balance reaches $1.9 million or above as at 30 June 2024. So you won’t be able to make a spouse contribution if your partner’s balance reaches that amount. There are also restrictions on the ability to trigger bring-forward rules for certain people with large super balances (more than $1.66 million in 2024-25).

There are also different super balance limits in place if you want to take advantage of the bring-forward rules.

How contributions splitting differs

Another way to increase your partner’s super is by splitting up to 85% of your concessional super contributions with them, which you either made or received in the previous financial year. Concessional super contributions can include employer and or salary-sacrifice contributions, as well as voluntary contributions you may have claimed a tax deduction for.

What rules apply for contribution splitting?

To be eligible for contributions splitting, your partner must be between age 60 (preservation age) and 65 (and not retired).

Are there limits to how much can be contributed?

Amounts you split from your super into your partner’s super will count toward your concessional contributions cap, which is $30,000 per year for everyone.

On top of this, unused cap amounts accrued in the last 5 years can also be contributed, if they’re eligible. Note, this broadly applies to people whose total super balance was less than $500,000 on 30 June of the previous financial year.

Do all super funds allow for this type of arrangement?

You’ll need to talk to your super fund to find out whether it offers contributions splitting, and it’s also worth asking whether there are any fees.

What else you and your partner should know

- If either of you exceeds super contribution caps, additional tax and penalties may apply.

- The value of your partner’s investment in super, like yours, can go up and down, so before making contributions, make sure you both understand any potential risks.

- The government sets rules about when you can access your super. Generally, you can access it when you’ve reached age 60 (preservation age) and retire.

- While you can’t personally make further non-concessional contributions into your super once you have a total super balance of $1.9 million or above (as at 30 June of the previous financial year), it’s still possible to make contributions to your partner’s super (noting the caps).

Where to go for more information

Your circumstances will play a big part in what you both decide to do. And, as the rules around spouse contributions and contributions splitting can be complex, it’s a good idea to chat to your financial adviser to make sure the approach you and your partner take is the right one.

Source: AMP