All posts by Robert Wright

What is risk appetite?

By Robert Wright /May 28,2024/

Risk is about tolerating the potential for losses. Understanding your risk appetite allows you to make well informed decisions about your money.

For some people, risk means excitement and opportunity. For others, it invokes feelings of fear and discomfort. We all experience a degree of risk in our everyday lives – whether it’s simply walking down the street or having investments in the share market. Everyone has a risk profile that defines their willingness to accept risk. It’s usually shaped by age, lifestyle and goals and is likely to change over time.

Risk is about tolerating the potential for losses, the ability to withstand market movements and the inability to predict what’s ahead[1]. In financial terms, risk is the chance that an outcome will differ from the expected outcome or return. It includes the possibility of losing some or all of your original investment[2]. Often you may not be aware of your risk appetite until you’re facing a potential loss, so loss aversion becomes a significant factor when making decisions related to risk.

What is risk appetite and risk tolerance?

Risk appetite and risk tolerance are used interchangeably but are different.

Risk appetite is a broad description of the amount of risk an investor is willing to accept to achieve their objectives. It’s a statement or series of statements that describes their attitude towards risk taking[3].

Risk tolerance is the practical application of risk appetite3 and considers the degree of variability in returns an investor is willing to bear.

As an investor, you should have a good understanding of your attitude towards risk. If you take on too much risk, you might panic and sell at a bad time. But if you don’t expose yourself to enough risk, you may be disappointed with your returns and potentially unable achieve your objectives.

How do I work out my risk appetite?

Think about how you might answer these questions:

- How much money do I have to invest?

- How much money am I willing to lose?

- How worried would I be if share markets fell dramatically?

- Am I planning to track your investments daily?

- Would I consider investing in different types of investments?

Your age, income and investment objectives all help determine your risk appetite.

Age: generally younger investors with a longer time horizon to invest are more willing to take greater risk with their money to earn higher potential returns. Older investors with a shorter investment timeframe may be more cautious as they’ll need their money to be more readily available and have less time to recover from a loss.

Income: people who earn more money and have a higher disposable income can typically afford to take greater risks with their investments.

Investment objectives: be clear about why you’re investing and when you think you’ll need to withdraw your money, as well as how long you need the money to last. Saving for a holiday or a deposit on a home is quite different from investing for your retirement.

Risk and Return

The relationship between risk and return underpins all financial decisions. The more risk an investor is willing to take, the greater the potential return. However, investors expect to be compensated for taking on this additional risk and should realise that taking on more risk doesn’t guarantee higher returns.

What type of investor are you?

- High: willing to risk losing more money for the possibility of better returns.

- Moderate: willing to endure short-term loss for the prospect of better long-term growth opportunities.

- Conservative: willing to accept lower returns for a higher degree of liquidity or stability.

Whatever your risk appetite, you should always consider both risk and return before making decisions about what to do with your money. Although shares and property are generally considered to be higher-risk investments, even more conservative investments like bonds can experience short-term losses. No investment is completely risk free.

This explains why smart investors typically have a diversified portfolio that includes several different types of investments.

Risk and Diversification

Don’t think that just because your friends invest in shares you should too. If you don’t have a lot to invest or you’ll want to access your money in a few years, shares may not be the right type of investment for you.

By understanding your risk appetite and being honest about what you want to achieve, you’re more likely to be comfortable with your investment decisions. A financial adviser can help you understand your risk appetite, as well as create a portfolio that suits you.

The simplest way to minimise investment risk is through diversification. A well diversified portfolio will usually include different asset classes, like shares, property, bonds and cash, with exposure across different industries, markets and countries. The idea is to reduce the correlation between the different types of investment and have a good balance of assets which move in different directions and at different times. So, if some of your assets perform poorly, others may be performing well, offsetting the poor performers.

Although diversification doesn’t guarantee you won’t suffer a loss, it’s an effective way to minimise risk and help investors realise their financial goals.

Make informed decisions

You should monitor both your risk appetite and your investment portfolio over time.

Your risk appetite is likely to change as you get older, and as your income or family situation changes.

Similarly, you should review your portfolio to ensure the risk level is still suited to your overall investment objectives. Financial markets are constantly changing, which means the underlying assets you’re invested in could change too.

If you’re a confident investor, you should check that it’s still on track to generate the level of return you want and importantly, at a comfortable level of risk. If you prefer to speak with a financial adviser, they too can help you undertake regular reviews and rebalance your portfolio, as necessary.

By understanding your risk appetite, you’re in a better position to make well informed and transparent financial decisions. It will help you identify opportunities to take on more risk where appropriate or see where you’re exposed to unnecessary risk and adjust accordingly. You’ll also avoid being caught up in the emotion of market activity, where panic can lead to a poorly timed and costly decision.

[1] Charles Schwab: How to Determine Your Risk Tolerance Level https://intelligent.schwab.com/public/intelligent/insights/blog/determine-your-risk-tolerance-level.html.

[2] Investopedia https://www.investopedia.com/terms/r/risk.asp.

[3] Australian Government Department of Finance: Defining Risk Appetite and Tolerance https://www.finance.gov.au/government/comcover/education/risk-appetite-and-tolerance.

Source: BT

Will cash remain king?

By Robert Wright /May 28,2024/

Cash has been one of the best performing defensive assets over the past three years. When compared with global bonds (a riskier asset class), a typical portfolio of term deposits would have returned a cumulative 12.6% in comparison to -8.5% for global bonds over the three years to December 2023. With interest rates expected to stay higher for longer, cautious investors would be right to question whether other asset classes are worth the risk. But are the tides changing?

On paper cash still appears to be king; however, these healthy returns are attributed to accelerated inflation and rising interest rates, an environment we may be moving away from. Inflation has been trending downwards for months and rate cuts are predicted to begin before the end of 2024.

In this paper we explain why we believe now is a good time to revisit your asset allocation.

What is a bond?

A bond is a loan made by an investor to a borrower, generally a company or government. Typically, the borrower pays the investor interest (coupons) periodically over the term of the loan and then returns the initial value (principal) of the loan back to the investor at an agreed upon future date.

Bond values are linked to the borrowers perceived ability to pay back the loan as well as interest rates. For example, when interest rates rise, newly issued bonds offer higher coupons, making them more attractive and equivalent existing bonds with lower coupons less attractive, reducing their value.

How do bonds differ from term deposits?

Bonds are expected to provide higher returns over the long term because investors require compensation for assuming investment risk. Bonds also provide the opportunity for capital growth as well as higher income. This compares with term deposits where interest payments are lower but guaranteed by a bank – providing more security. Whilst income is guaranteed, the real value of a term deposit often diminishes over time due to inflation, which erodes your purchasing power (figure 1).

Figure 1 also shows that bonds are subject to greater risk over shorter time horizons which means they won’t be suitable for everyone. Your initial investment can go down in value and when you invest in funds this can be offset through the distributions, reducing your income. This primarily occurs when interest rates are rising and become unpredictable as they have in recent times.

Investors need to determine, with support from their adviser, whether trading term deposits capital guarantee for the potential increased return of a bond investment is suitable to their circumstances.

Why now?

In an environment where inflation is trending down and rates are expected to be cut, long term bonds should perform well as this is the environment when you typically experience the most capital growth (see figure 2). Term deposit rates are also forward looking. In other words, you don’t need to wait for central banks to reduce cash rates before you start to see term deposit returns fall. There are already signs of this happening. Whilst very recent, 1-year term deposit rates came down by 0.05% in January and we expect this trend to continue (although this won’t necessarily be a smooth journey). Whilst seemingly insignificant, this could be meaningful for larger investors. Particularly where capital growth has no role to play and investors don’t require the capital guarantee of cash.

What happens if the economy deteriorates?

If a recession were to occur, interest rates are more likely be cut quicker to encourage spending, resulting in bond prices rising. This would be supported by increased demand as investors move away from higher risk assets such as equities. If we don’t enter a recession and achieve a soft-landing scenario, rates will likely trend down more slowly to bring inflation in line with central banks’ targets; once again favouring bonds due to the inverse relationship between interest rates and bond values.

Conclusion

We believe it is critical to take a diversified approach to investing to help manage portfolio risks through different market conditions. The balance and mix of assets will depend on each investor’s ability and willingness to take on investment risk as well as how much of their capital they need guaranteed.

That said, we believe now is a great time to be reassessing your asset allocation. Investors looking for capital growth who don’t need capital guarantees should consider introducing bonds into, or back into, their investment portfolio and doing so before central banks begin to cut rates.

While cash rates may seem alluring, it is important to remember the distinct roles bonds and cash play in a portfolio. Cash is best reserved for short-term spending needs that require a guarantee as it will not provide the long-term capital growth and inflation protection of other assets.

It may seem daunting as we have been through a period of significant market volatility but over the long term, we have high conviction that bonds will provide better risk adjusted return outcomes for investors who are able to take on the increased risks offered by bonds.

As always, we recommend speaking to your financial adviser to get tailored advice based on your unique circumstances prior to making any investment changes.

Source: Perpetual

Seven lasting impacts from the COVID pandemic

By Robert Wright /May 28,2024/

Key points

- Seven key lasting impacts from the Coronavirus pandemic are: “bigger” government; tighter labour markets; reduced globalisation and increased geopolitical tensions; higher inflation; worse housing affordability; working from home; and a faster embrace of technology.

- On balance these make for a more fragmented and volatile world for investment returns. But it’s not all negative.

Introduction

It’s four years since the COVID lockdowns started. The pandemic ended when it morphed into the less deadly Omicron variant in late 2021, but just as a sound can reverberate around a room the effects of the pandemic continue to reverberate in economies. Putting aside the long-term health impacts this note looks at 7 key lasting economic impacts.

- Bigger government and more public debt

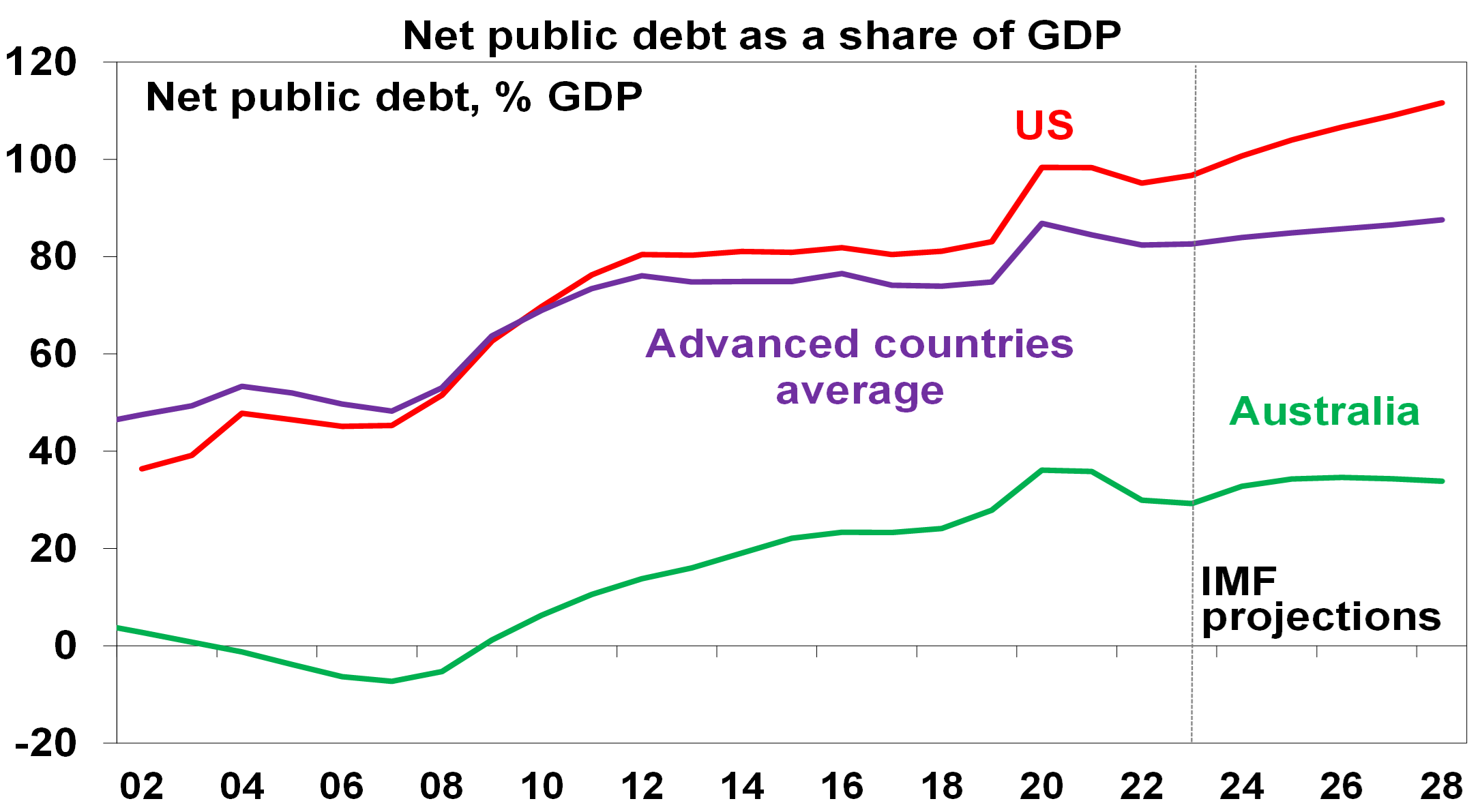

The malaise of the 1970s ushered in “smaller” government in the 1980s in the Thatcher, Reagan, Hawke and Keating era. But the political pendulum started to swing back to “bigger” government after the GFC and COVID has given it another push. Memories of the problems of high government intervention in the 1970s have faded and there is rising support for the view that government is the solution to most problems – via regulation, taxes, spending or education campaigns. The pandemic added to support for “bigger” government: by showcasing the power of government to protect households and businesses from shocks; enhancing perceptions of inequality; and adding support to the view that governments should ensure supply chains by bringing production back home. It’s combining with a desire for governments to pick and subsidise clean energy “winners”.

Source: IMF, Australian Government, AMP

IMF projections for government spending in advanced countries show it settling nearly 2% of GDP higher than pre-COVID levels. The success of governments in protecting households from the worst of the pandemic has also reinforced expectations they would do the same in the next crisis. The pandemic ushered in even bigger public debt just as the GFC did. While high inflation helped lower debt to GDP ratios in 2022 it’s settling at higher levels than pre-pandemic.

Source: IMF, AMP

Implications – While there may initially be a feel good factor, the long-term outcome of “bigger” government is likely to be less productive economies, lower than otherwise living standards and less personal freedom. It will take time before this becomes apparent though. Meanwhile, higher public debt means: less flexibility to respond with fiscal stimulus to a crisis; a greater incentive for politicians to inflate their way out; and interest payments being a high share of tax revenue.

- Tighter labour markets and faster wages growth

In the pre-pandemic years, wages growth was relatively low and a key driver was high levels of underemployment, particularly evident in Australia. After the pandemic, labour markets have tightened reflecting the rebound in demand post pandemic, lower participation rates in some countries and a degree of labour hoarding as labour shortages made companies reluctant to let workers go. As a result, wages growth increased, possibly breaking the pre-pandemic malaise of weak wages growth.

Source: ABS, AMP

Implications – Tighter labour markets run the risk that wages growth exceeds levels consistent with 2% to 3% inflation.

- Reduced globalisation/more geopolitical tensions

A backlash against globalisation became evident last decade in the rise of Trump, Brexit and populist leaders pushing a nationalist gender when the benefits of free trade were being questioned. Also, geopolitical tensions were on the rise with the relative decline of the US and faith in liberal democracies waning resulting in a shift from a unipolar world dominated by the US, to a multipolar world as regional powers (Russia, Iran, Saudi Arabia and notably China) flexed their muscles. The pandemic inflamed both – with supply side disruptions adding to pressure for the onshoring of production; conflict over the source of and management of coronavirus; it heightened tensions between the west and China; and it appears to have added to nationalism and populism. So, the days of global free trade agreements and falling defence spending seem long gone for now. Rather we are seeing more protectionism (e.g. with subsidies and regulation favouring local production) and increased defence spending.

Implications – Reduced globalisation risks leading to reduced potential economic growth for the emerging world and reduced productivity if supply chains are managed on other than economic grounds. And combined with increased geopolitical tensions resulting in more defence spending it could result in a more inflation prone world than was the case.

- Higher prices, inflation and interest rates

A big downside of the pandemic support programs was the surge in inflation. The combination of massive money printing along with a big increase in government payments to households (e.g. Job Keeper) resulted in a massive boost to spending once lockdowns were lifted which combined with supply chain disruptions, also flowing from the pandemic, to cause a surge in inflation. Inflation is now starting to come under control as the monetary easing and spending boost has been reversed and supply has improved again but the pandemic has likely ushered in a more inflation prone world by boosting “bigger” government; adding to a reversal in globalisation; and adding to geopolitical tensions. All of which combine with aging populations to potentially result in more inflation.

Implications – Higher inflation than seen pre-pandemic means higher than otherwise interest rates over the medium term which reduces the upside potential for growth assets like shares and property.

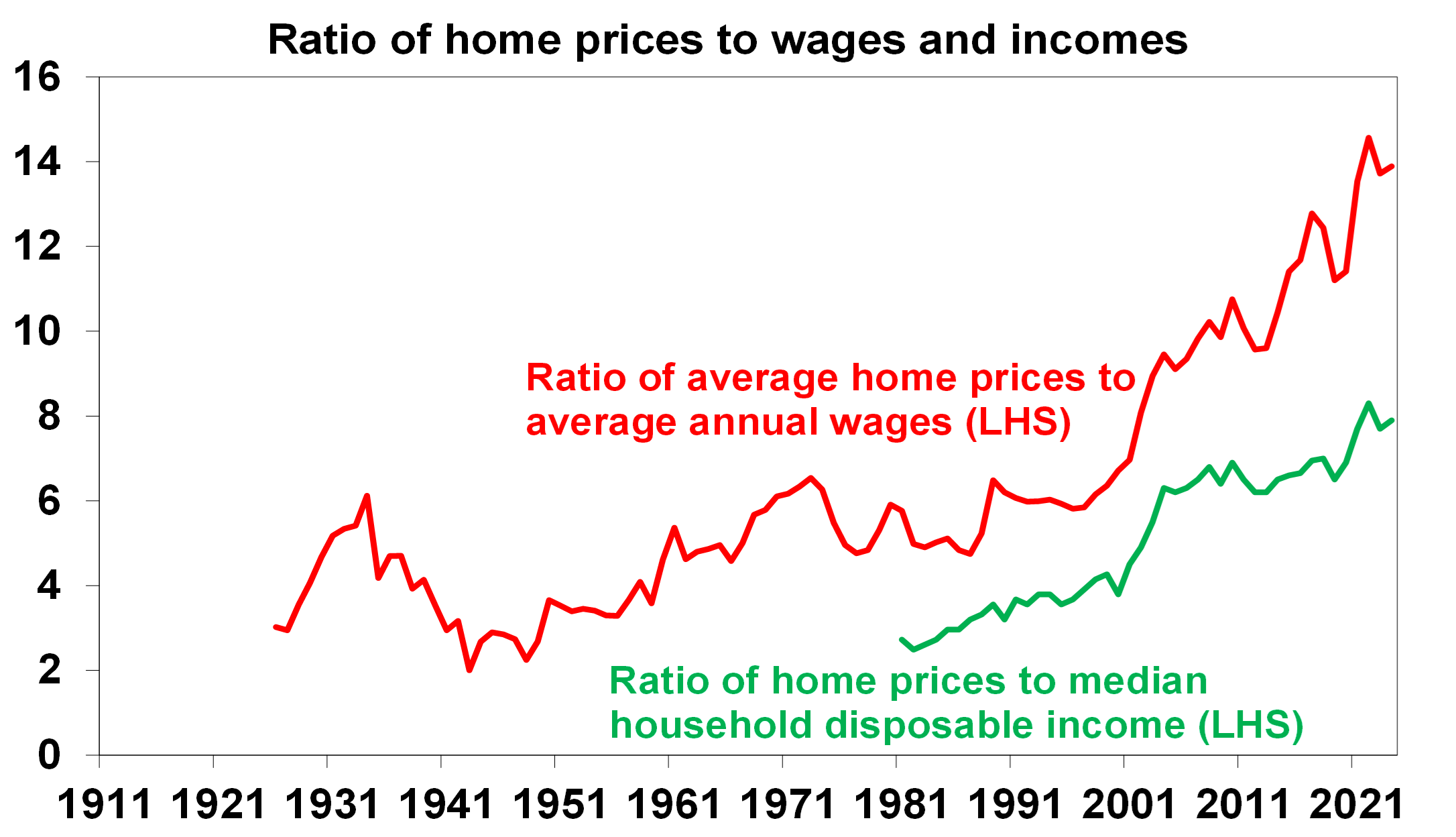

- Worse housing affordability

At the start of the pandemic, it was thought the economic downturn and higher unemployment and a freeze in immigration would cause a collapse in home prices and they did initially fall. But not by much as it was quickly turned around by policy measures to support household income, allow a pause in mortgage payments and slash interest rates and mortgage rates to record lows. What’s more the lockdowns and working from home drove increased demand for houses over units and interest in smaller cities and regional locations. As a result, Australian home prices surged to record levels. Meanwhile the impact of higher interest rates in the last two years on home prices was swamped by housing shortages as immigration surged in a catch up. The end result is now record low levels of housing affordability for buyers (who are hit by a double whammy of higher prices relative to incomes – see the next chart – and higher mortgages rates) and renters (who have seen surging rents).

Source: ABS, CoreLogic, AMP

Implications – Ever worse housing affordability means ongoing intergenerational inequality and even higher household debt.

- Working from home likely here to stay

While there has been a return to the office, for many its only two or three days a week. Basically, the lockdowns resulted in a step jump towards working from home (WFH). A UK study of over 2000 firms is indicative. It showed that while around 90.8% of employees were fully onsite in 2018, last year this had fallen to 62.3%, with 30.2% with hybrid (working in the office and at home) arrangements. Similarly, the ABS found 37% of employed people in Australia regularly worked from home. Of course, this masks a huge range with industries with a high proportion of computer-based workers having more hours working at home. And firms expect this to remain the case. There are huge benefits to physically working together around culture, collaboration, idea generation and learning but there are also benefits to working from home with no commute time, greater focus, less damage to the environment, better life balance and for companies – lower costs, more diverse workforces and happier staff. So the ideal is probably a hybrid model. The proportion of workers in a hybrid model may even rise as new firms are quicker to embrace WFH.

Working arrangements for UK employees

Source: K Shah, and others, Managers say working from home here to stay, CEPR

Implications – Less office space demand as leases expire resulting in higher vacancy rates/lower rents, more people living in cities as vacated office space is converted and reinvigorated life in suburbs and regions.

- Faster embrace of technology

Lockdowns dramatically accelerated the move to a digital world. Everyone was forced to embrace new online ways of doing things. Many have now embraced online retail, working from home and virtual meetings. It may be argued that this fuller embrace of technology will enable the full productivity enhancing potential of technology to be unleased. The rapid adoption of AI will likely help.

Implications – This has meant a faster embrace of online retailing (up from 7% of retailing pre-pandemic to around 11%) at the expense of traditional retailing, virtual meeting attendance becoming the norm for many (even in the office) and business travel settling at a lower level.

Concluding comments

Perhaps the biggest impact is that the pandemic related stimulus broke the back of the ultra-low inflation seen pre-pandemic. Together with bigger government and reduced globalisation, this means a more inflation-prone world. So, a return to pre-pandemic ultra-low inflation and interest rates looks unlikely. It’s not all negative though – apart from the faster technology uptake, the global and Australian economies have come through the last four years in far better shape than might have been imagined at the start of the lockdowns!

Source: AMP

Millions to get more Age Pension starting from 20 March 2024

By Robert Wright /May 28,2024/

Government Age Pension payments increased on 20 March, so if you’re one of the millions of eligible Australians, you’ll have a little more to spend.

The increases are designed to help address inflation and cost of living increases. Here’s what happened.

Age Pension payments increase in March 2024 due to indexation

Here are the maximum Age Pension payment rates that came into effect from 20 March, which are paid fortnightly, along with their respective annual equivalents. Single payments rose by $19.60 per fortnight, while combined payments for couples increased by $29.40.

Maximum Age Pension payments from 20 March 2024

| Fortnightly* | Annually* | |

| Single | $1,116.30 | $29,023.80 |

| Previous payment | $1,096.70 | $28,514.20 |

| Couple (each) | $841.40 | $21,876.40 |

| Previous payment | $826.70 | $21,494.20 |

| Couple (combined) | $1,682.80 | $43,752.80 |

| Previous payment | $1,653.40 | $42,988.40 |

*Includes basic rate plus maximum pension and energy supplements

The payment rate increased 1.8%, indexed to inflation. Payments last increased in September 2023 and are likely to change again when they are next assessed this coming September.

Tip: Depending on how much super you have, you may be eligible to receive Age Pension payments in addition to income from your super savings.

Income and assets test thresholds increase for the Age Pension

The government reviews the Age Pension income and assets test thresholds in July each year. The upper thresholds also increase in March and September each year in line with Age Pension payment increases.

Whether you are eligible for the Age Pension depends on your age, residency and your income and assets.

If your income and assets are below certain limits (also known as thresholds), you may be eligible.

When determining how much you’re entitled to receive under the income and assets tests, the test that results in the lower amount of Age Pension applies.

Here are the income and assets test thresholds that apply as at 20 March, compared with previous thresholds.

Assets test thresholds comparison

The lower assets test threshold determines the point where the full Age Pension starts to reduce, while the upper assets test thresholds determine what the cutoff points are for the part Age Pension.

If the value of your assets falls between the lower and upper assets test thresholds, your entitlement will reduce.

The higher your assessable assets, the lower the amount of Age Pension you are eligible to receive.

Your family home is exempt from the assets test but, your investments, household contents and motor vehicles may be included.

Asset test thresholds from 20 March 2024

| Full Age Pension limit | Part Age Pension cutoff | |

| Single – Homeowner | $301,750 (unchanged) | $674,000 |

| Previous threshold | $301,750 | $667,500 |

| Single – Non-homeowner | $543,750 (unchanged) | $916,000 |

| Previous threshold | $543,750 | $909,500 |

| Couple (combined) – Homeowner | $451,500 (unchanged) | $1,012,500 |

| Previous threshold | $451,500 | $1,003,000 |

| Couple (combined) – Non-homeowner | $693,500 (unchanged) | $1,254,500 |

| Previous threshold | $693,500 | $1,245,000 |

Income test thresholds comparison

The lower income test threshold determines the point where the full Age Pension starts to reduce, while the upper income test threshold determines what the cutoff point is for the part Age Pension.

Income includes things like payment for employment or self-employment activities, rental income, and a deemed rate of income from financial investments such as managed funds, super (if you are over the Age Pension age) or account-based pensions commenced after 1 January 2015.

Income doesn’t include things like emergency relief payments.

Income test thresholds from 20 March 2024

| Full Age Pension limit | Part Age Pension cutoff | |

| Single | $204 per fortnight (unchanged) | $2,436.60 per fortnight |

| Previous threshold | $204 per fortnight | $2,397.40 per fortnight |

| Couple (combined) | $360 per fortnight (unchanged) | $3,725.60 per fortnight |

| Previous threshold | $360 per fortnight | $3,666.80 per fortnight |

If you have income between the lower and upper income test thresholds, your entitlement will reduce as your level of income rises.

For example, the Age Pension payment for a single person earning more than $204 per fortnight will reduce by 50 cents for each dollar earned over $204.

For a couple earning more than $360 per fortnight combined, the Age Pension payment for each person will reduce by 25 cents for each dollar earned over $360.

Tip: The Work Bonus may allow you to receive more income from working, without reducing your Age Pension.

The maximum Work Bonus balance that you can accrue is $11,800.

Source: Colonial First State