All posts by Robert Wright

Mortgage vs super: where should I put my extra money?

By Robert Wright /February 16,2024/

It’s a dilemma many of us face – are we better off directing extra money to our mortgage or super? As with most financial decisions, it’s not a one size fits all approach and here are some factors to consider in deciding what’s right for you.

Key takeaways:

- There may be tax advantages when you contribute to super, especially if you salary sacrifice or you’re eligible to claim a tax deduction for personal super contributions.

- The power of compounding returns could mean that even small contributions to your super over many years could make the world of difference.

- By making extra mortgage repayments, coupled with any potential increase in the value of your property, you will build equity in your property at a faster rate than if you were to make just the minimum repayments.

Building the case for super over mortgage

You might think your super is already being taken care of – after all, that’s what your employer’s compulsory Superannuation Guarantee contributions are all about. But these contributions alone often aren’t enough to ensure you achieve the retirement lifestyle you want to live.

Making extra contributions to your super is a great way to boost your retirement savings. As an investment vehicle, super is a very tax effective way to save for the future.

The power of compounding returns

Super is a long term investment, at least until you retire, and potentially much longer if you leave your money in super and draw a pension after you retire.

This long investment term, coupled with the rate of tax on your super investment (generally 15%), means your money can add up and generate further investment returns on those returns. This is known as compound returns, or compounding.

The expenses of daily life can be considerable. Thinking about directing money to super might not seem like a priority when we feel overwhelmed by the effort to save a deposit for a home, paying down debt, and the costs of raising a family.

However, the benefit of compounding returns means that even small, frequent contributions can make a big difference down the track. It’s about striking a balance that is right for you today and remember, nothing has to be forever. As your life changes, you can simply adjust your contributions strategy to suit your needs.

Building super early

To maximise your retirement savings while allowing compounding returns to do the heavy lifting, the best approach is to start early. The longer compounding continues, the bigger your savings could be. Entering retirement debt free is an attractive prospect. It can be easy to think that you need to repay your debt before you can start thinking about saving for retirement. However, it doesn’t have to be one or the other.

You can see the difference small, regular contributions could make to your final retirement income using the MoneySmart retirement planner calculator.

Tax benefits of super

From a tax point of view, super can be incredibly beneficial. Salary sacrificing some of your before-tax salary or making a voluntary after-tax contribution for which you can claim a tax deduction, can be effective ways to not only grow your retirement savings but also reduce your taxable income.

One great benefit of investing in super is that concessional (before tax) contributions are taxed at a maximum rate of 15%. This can be higher though if you earn over $250,000.

Mortgage repayments are usually made from your take home pay after you’ve paid tax at your marginal tax rate. Your marginal tax rate could be as high as 47%. So, depending on your circumstances, making a voluntary deductible contribution to super or salary sacrificing may result in an overall tax saving of up to 32%.

There is a limit on the amount you can contribute into super every year. These are referred to as contribution caps. Currently, the annual concessional contributions cap is $27,500. If you’re eligible to use the catch-up concessional contributions rules, you may be able to carry forward any unused concessional contributions for up to 5 years. If you exceed these caps, you may be liable to pay more tax.

Tax on super investment earnings

The initial tax savings are only part of the story. The tax on earnings within the super environment are also low.

The earnings generated by your super investments are taxed at a maximum rate of 15%, and eligible capital gains may be taxed as low as 10%. Once you retire and commence an income stream with your super savings, the investment earnings are exempt from tax, including capital gains.

Also, when it comes time to access your super in retirement, if you’re aged 60 or over, amounts that you access as a lump sum are generally tax free.

However, it’s important to remember that once contributions are made to your super, they become ‘preserved’. Generally, this means you can’t access these funds as a lump sum until you retire and reach your preservation age, between 55 and 60 depending on when you were born.

Before you start adding extra into your super, it’s a good idea to think about your broader financial goals and how much you can afford to put away because with limited exceptions, you generally won’t be able to access the money in super until you retire.

In contrast, many mortgages can be set up to allow you to redraw the extra payments you’ve made or access the amounts from an offset account.

Building the case for reducing your mortgage over super

For many people, paying off debt is the priority. Paying extra off your home loan now will reduce your monthly interest and help you pay off your loan sooner. If your home loan has a redraw or offset facility, you can still access the money if things get tight later.

Depending on your home loan’s size and term, interest paid over the term of the loan can be considerable – for example, interest on a $500,000 loan over a 25-year term, at a rate of 6% works out to be over $460,000. Paying off your mortgage early also frees up that future money for other uses.

Before you start making additional payments to your mortgage, it’s suggested that you should first consider what other non-deductible debt you may have, such as credit cards and personal loans. Generally, these products have higher interest rates attached to them so there is greater benefit in reducing this debt rather than your low interest rate mortgage.

Conclusion: mortgage or super

It’s one of those debates that rarely seems to have a clear-cut winner – should I pay off the mortgage or contribute extra to my super?

The answer, probably somewhat annoyingly, is that it depends on your personal circumstances.

There is no one size fits all solution when it comes to the best way to prepare for retirement. On the one hand, contributing more to your super may increase your final retirement income. On the other, making extra mortgage repayments can help you clear your debt sooner, increase your equity position and put you on the path to financial freedom.

When weighing up the pros and cons of each option, there are a few key points to keep in mind.

One of the key questions to consider is what is the likely balance you’ll need in your super? Work backwards starting with working through what retirement looks like for you, the type of lifestyle you’d like, and how much you need to live on each year.

From there, you can start to consider your sources of income in retirement. This is likely to include super but could also include a full or part Age Pension, or income from an investment property or other sources.

You can then start thinking about your current balance, contributions strategies and whether you’re on track to have enough saved to supplement your other retirement income sources.

The MoneySmart retirement planner calculator can help you to estimate how much super you may have in retirement and how long your super may last. You also need to think about how you plan to spend your money in retirement.

In most cases, there isn’t one set strategy that you should follow and it can quickly change as you grow older, start a family and reach retirement age. You should also consider whether you’ll need to access any additional funds you put aside before you reach retirement. If it’s in your super, it’s locked away. If it’s in your mortgage, there are generally options to redraw.

Home ownership and comfortable retirement are financial goals that many strive towards. If you reach a point where there’s some surplus cash flow to consider where to put your extra money, it’s a good dilemma to have.

Life is complex, so it pays to speak with a financial adviser before you make any big financial decisions when it comes to your super or mortgage.

Source: MLC

Falling inflation – what does it mean for investors?

By Robert Wright /February 16,2024/

Key points

- Inflation is in retreat thanks to improved supply and cooling demand. A further fall is likely this year.

- Australian inflation remains relatively high – but this mainly reflects lags rather than a more inflation prone economy.

- Profit gouging or wages were not the cause of high inflation.

- The main risks relate to the conflict in the Middle East escalating and adding to supply costs; a surprise rebound in economic activity and sticky services inflation; and floods, the port dispute and poor productivity in Australia.

- Lower inflation should be positive for investors via lower interest rates, although this benefit may come with a lag.

- The world is now a bit more inflation prone so don’t expect a return to near zero interest rates anytime soon.

Introduction

The surge in inflation coming out of the pandemic and its subsequent fall has been the dominant driver of investment markets over the last two years – first depressing shares and bonds in 2022 and then enabling them to rebound. But what’s driving the fall, what are the risks and what does it mean for interest rates and investors? This article looks at the key issues.

Inflation is in retreat

Inflation appears to be falling almost as quickly as it went up. In major developed countries it peaked around 8% to 11% in 2022 and has since fallen to around 3% to 4%. It’s also fallen in emerging countries.

Source: Bloomberg, AMP

What’s driving the fall in inflation?

The rise in inflation got underway in 2021 and reflected a combination of massive monetary and fiscal stimulus that was pumped into economies to protect them through the pandemic lockdowns that was unleashed as spending (first on goods then services) at a time when supply chains were still disrupted. So it was a classic case of too much money (or demand) chasing too few goods and services. Its reversal since 2022 reflects the reversal of policy stimulus as pandemic support measures ended, pent up or excess savings has been run down by key spending groups, monetary policy has gone from easy to tight and supply chain pressures have eased. In particular, global money supply growth which surged in the pandemic has now collapsed.

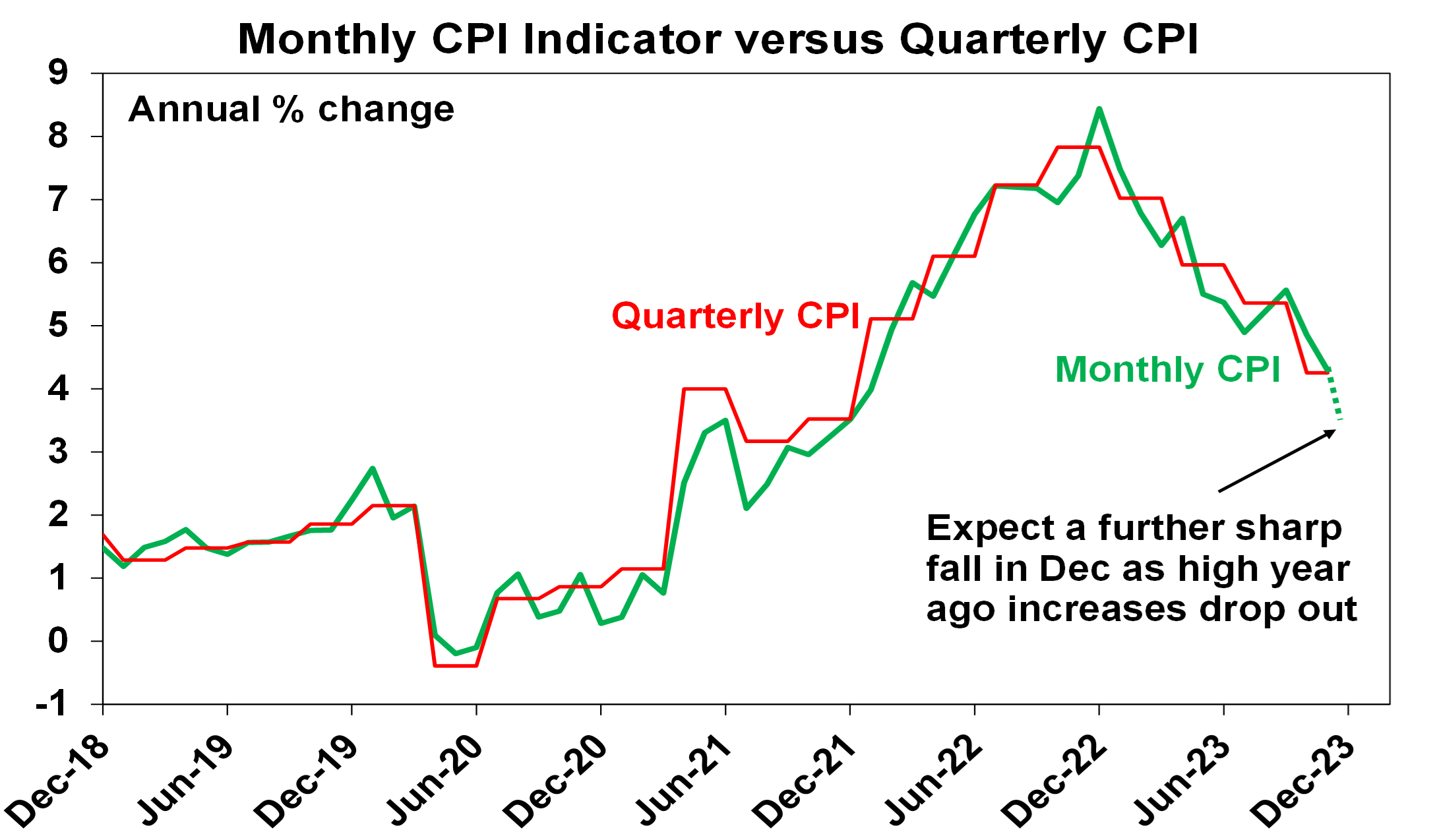

Why is Australian inflation higher than other countries?

While there has been some angst about Australian inflation (at 4.3% year on year in November) being higher than that in the US (3.4%), Canada (3.1%), UK (3.9%) and Europe (2.9%), this mainly reflects the fact that it lagged on the way up and lagged by around 3 to 6 months at the top. The lag partly reflects the slower reopening from the pandemic in Australia and the slower pass through of higher electricity prices. So we saw inflation peak in December 2022, whereas the US, for instance, peaked in June 2022. But just as it lagged on the way up it’s still following other countries down with roughly the same lag. In fact, with a very high 1.5% month on month implied rise in the Monthly CPI Indicator to drop out from December last year, monthly CPI inflation is likely to have dropped to around 3.3% to 3.7% year on year in December last year, which is more in line with other countries.

Source: Bloomberg, AMP

What about profit gouging?

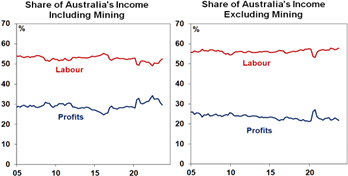

There has been some concern that the surge in prices is due to “price gouging” with “billion dollar profits” cited as evidence. In fact, the Australian Government has set up an inquiry into supermarket pricing. There are several points to note in relation to this. First, it’s perfectly normal for any business to respond to an increase in demand relative to supply by raising prices. Even workers do this (e.g. asking for a pay rise and leaving if they don’t get one when they are getting lots of calls from headhunters). It’s the way the price mechanism works in allocating scarce resources. Second, national accounts data don’t show any underlying surge in the profit share of national income, outside of the mining sector. Finally, blaming either business or labour (with wages growth picking up) risks focusing on the symptoms of high inflation not the fundamental cause, which was the pandemic driven policy stimulus and supply disruption. This is not to say that corporate competition can’t be improved.

Source: ABS, RBA, AMP

What is the outlook for inflation?

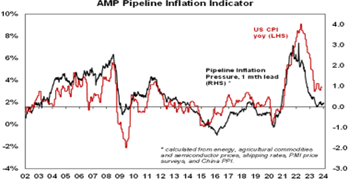

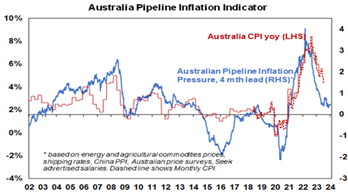

Our US and Australian Pipeline Inflation Indicators continue to point to a further fall in inflation ahead.

Source: Bloomberg, AMP

This is consistent with easing supply pressures, lower commodity prices and slowing demand. It’s not assuming recession, but it is a high risk and if that occurred it would likely result in inflation falling below central bank targets. Out of interest, the six month annualised rate of core private final consumption inflation in the US, which is what the Fed targets, has fallen below its 2% inflation target. In Australia, it’s expected that the quarterly CPI inflation to have fallen to around 3% year on year by year end. The return to the top of the 2% to 3% target is expected to come around one year ahead of the RBA’s latest forecasts.

What are the risks?

Of course, the decline in inflation is likely to be bumpy and some say that the “last mile” of returning it to target might be the hardest. There are five key risks to keep an eye on in terms of inflation:

- First, the escalating conflict in the Middle East has the potential to result in inflationary pressures. Disruption to Red Sea/Suez Canal shipping is already adding to container shipping rates due to extra time in travelling around Africa. So far this has seen only a partial reversal of the improvement in shipping costs seen since 2022 and commodity prices and the oil price remain down. The US and its allies are likely to secure the route relatively quickly such that any inflation boost is short lived. The real risk though, is if Iran is drawn directly into the conflict, threatening global oil supplies.

- Economic activity could surprise on the upside again keeping labour markets tight, fuelling prices and wages, and hence sticky services inflation.

- Central banks could ease before inflation has well and truly come under control in a re-run of the stop/go monetary policy of the 1970s.

- In Australia, recent flooding could boost food prices and delays associated with industrial disputes at ports could add to goods prices. At present though, the floods are not on the scale of those seen in 2022 and it’s expected that any impact from both to be modest (at say 0.2%).

- Finally, and also in Australia if productivity remains depressed, 4% wages growth won’t be consistent with the 2% to 3% inflation target.

What lower inflation means for investors?

High inflation tends to be bad for investment markets because it means higher interest rates; higher economic uncertainty; and for shares, a reduced quality of earnings. All of which means that shares tend to trade on lower price to earnings multiples when inflation is high, and growth assets trade on higher income yields. We saw this in 2022 with bond yields surging, share markets falling and other growth assets pressured.

Source: Bloomberg, AMP

So, with inflation falling, much of this goes in reverse as we started to see in the last few months. In particular:

- Interest rates will start to come down. The Fed is expected to start cutting in May and the European Central Bank (ECB) to start cutting around April, both with 5 cuts this year. There is some chance that both could start cutting in March. The RBA is expected to start cutting around June, with 3 cuts this year.

- Shares can potentially trade on higher price-to-earnings (PEs) than otherwise.

- Lower interest rates with a lag are likely to provide some support for real assets like property.

Of course, the main risk is if economies slide into recession, which will mean another leg down in share markets before they start to benefit from lower interest rates. This is not our base case but it’s a high risk.

Concluding comment

Finally, while inflation is on the mend cyclically, it’s worth remembering that from a longer term perspective we have likely now entered a more inflation prone world than the one prior to the pandemic, reflecting bigger government; the reversal of globalisation; increasing defence spending; decarbonisation; less workers and more consumers as populations age. So short of a very deep recession, don’t expect interest rates to go back to anywhere near zero anytime soon.

Source: AMP

Australian household wealth

By Robert Wright /February 16,2024/

Is high Australian household wealth a source of support for consumers?

Key points

- Australia ranked as having one of the lowest rates of disposable income growth per capita amongst OECD countries in mid 2023.

- An increasing income tax burden and mortgage repayments have weighed on income growth, despite solid wages and salaries.

- But, household balance sheets in Australia look stronger compared to incomes. Household wealth increased in 2023, as home prices rose.

- However, growth in household wealth will decline in 2024 as home prices are expected to fall. Household incomes will also be under pressure as earnings growth slows from a softening labour market.

- As a result, high household wealth holdings will not be enough to offset a challenging environment for households in 2024, despite some easing in cost of living challenges.

Introduction

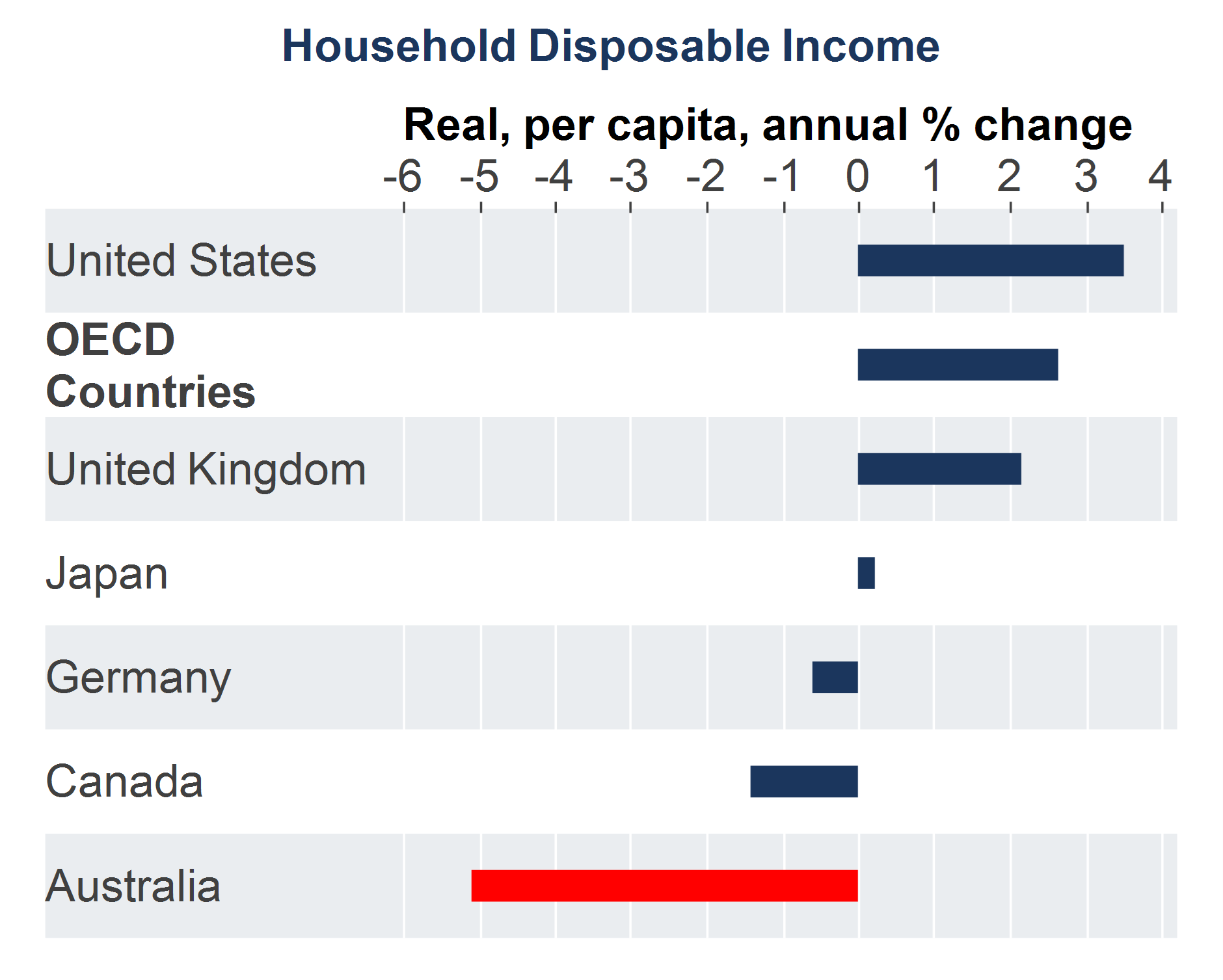

Household income data from the OECD showed that Australia had one of the lowest rates of annual real household disposable income per person compared to its OECD peers (see the chart below). Over the year to June 2023, Australia’s real per capita household disposable income was down by 5.1%, compared to a 2.6% rise across OECD countries.

Source: AMP, Macrobond

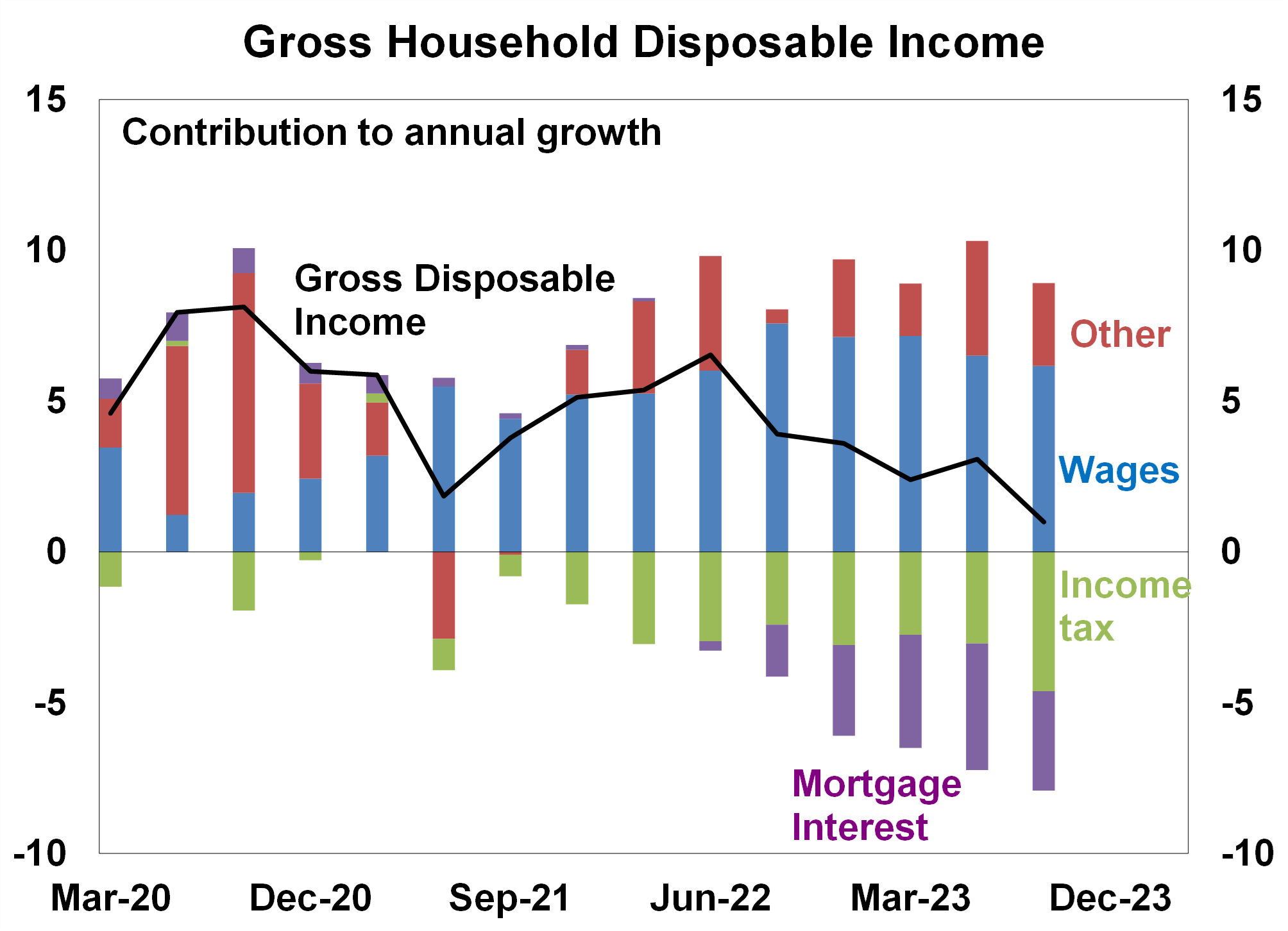

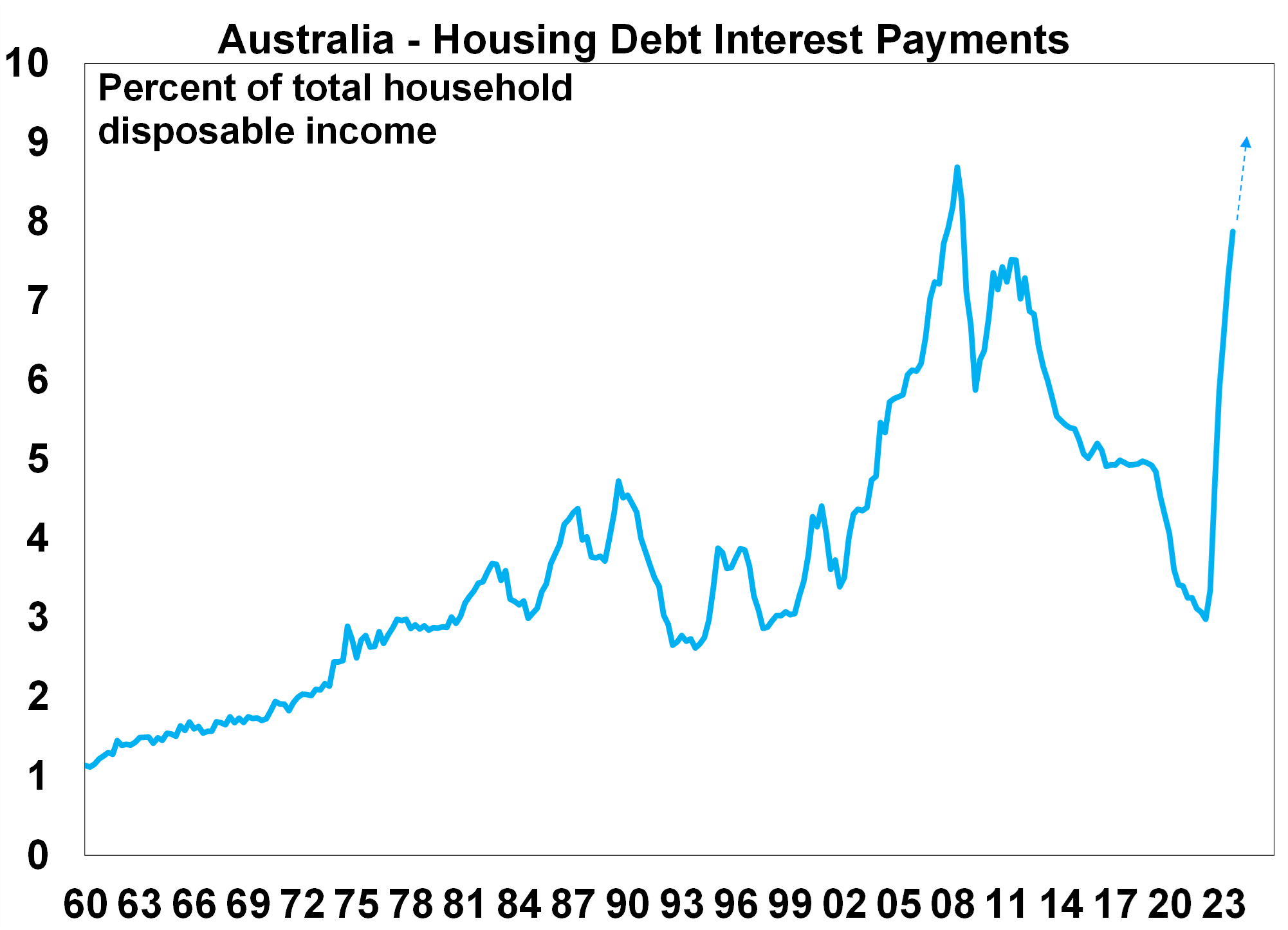

This occurred despite very healthy labour market conditions in Australia which saw employment growth running above 3.0% per annum all year, the unemployment rate remaining below 3.9% and underemployment continuing to be low, all of which boosted wages growth. Despite this positive earnings backdrop, the income tax burden increased in 2023 as households have been moving into higher income tax brackets (otherwise known as “bracket creep”), as well as the end of income tax concessions. Mortgage interest repayments are also an increasing drag on incomes (see the chart below) as the cash rate has been increased by 425 basis points since May 2022. Australia’s very high population growth in 2023 (running at 2.4% over the year to June 2023) also masked a fall in household disposable income growth per person, relative to other OECD countries.

Source: ABS, AMP

Just looking at household income accounts does not show everything about the position of households. In a country like Australia where home ownership rates are high (66% of Australian households own their home, with or without a mortgage), looking at household wealth is also important.

Household wealth in Australia

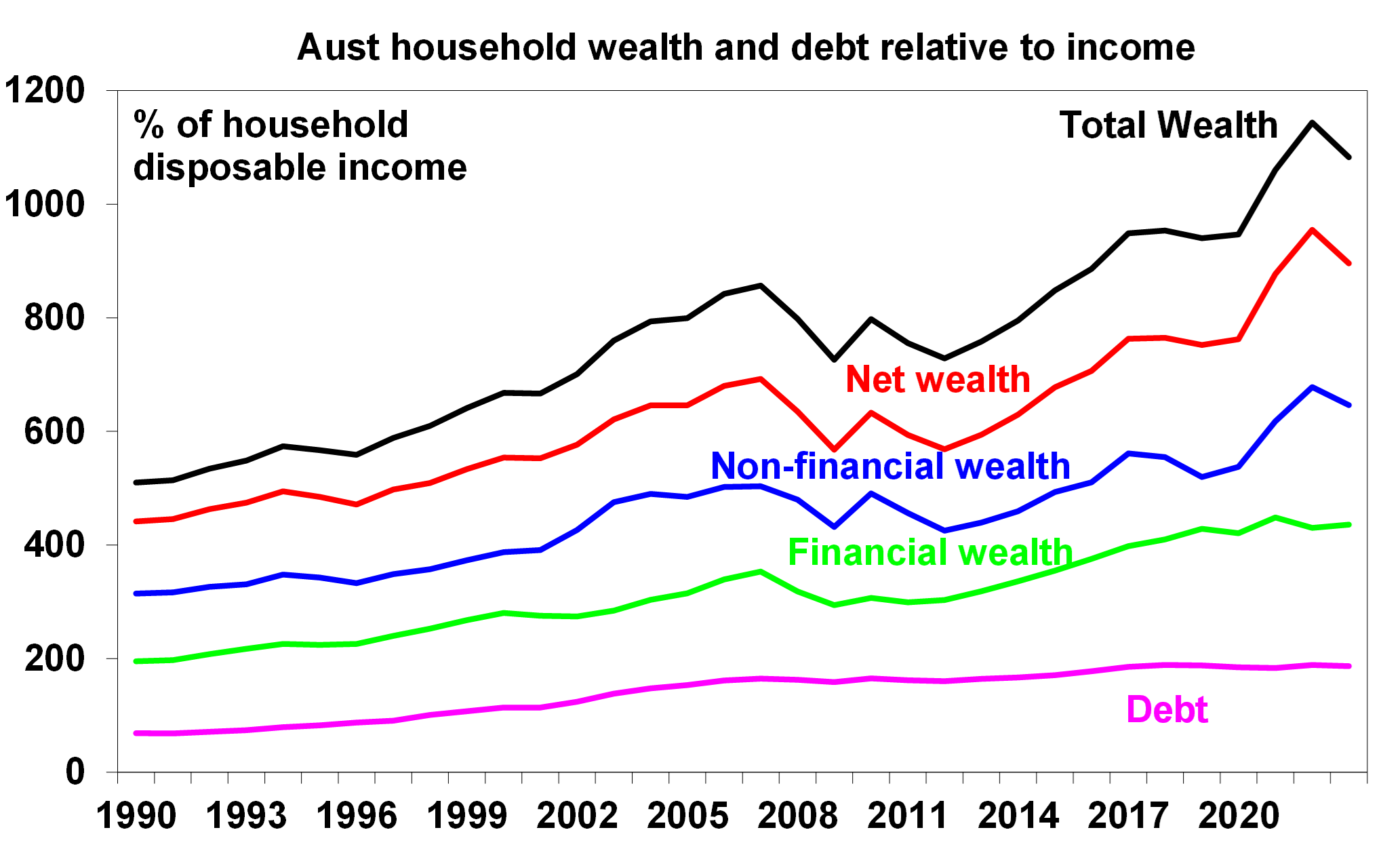

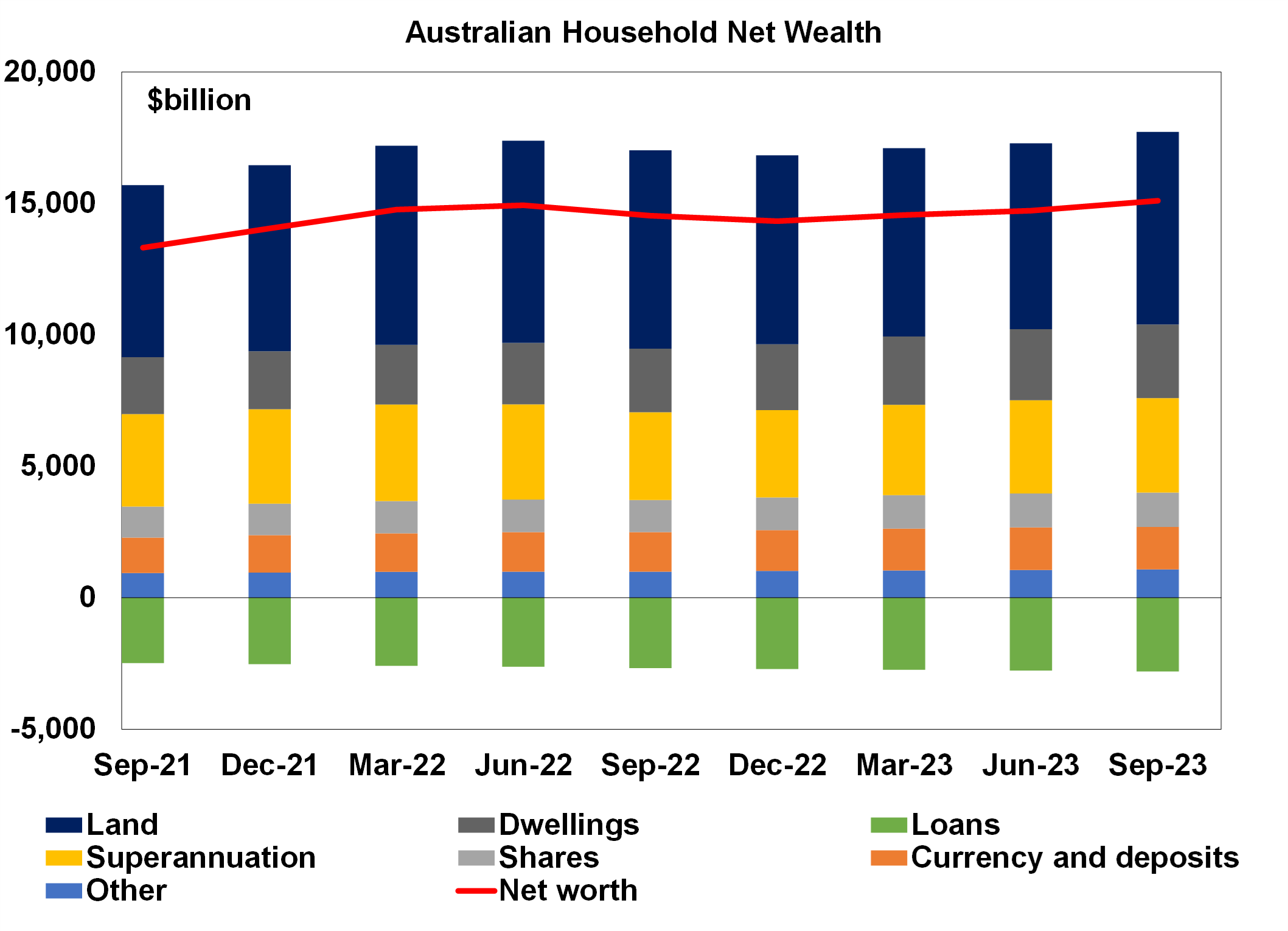

The Australian Bureau of Statistics estimates the value of a household’s assets, liabilities and therefore wealth. Net worth or wealth is calculated as a household’s total assets minus its liabilities. Total wealth is close to 11 times the size of household disposable income (or 1083%) and net wealth is 896% of income. The latest data for the year to June 2023 showed a slight fall in wealth as a share of income, after it reached a record high in 2022 – see the chart below. Non financial wealth is worth 647% of income, larger than financial wealth at 436% and well surpassing household debt, which is 187% of income.

Source: RBA, AMP

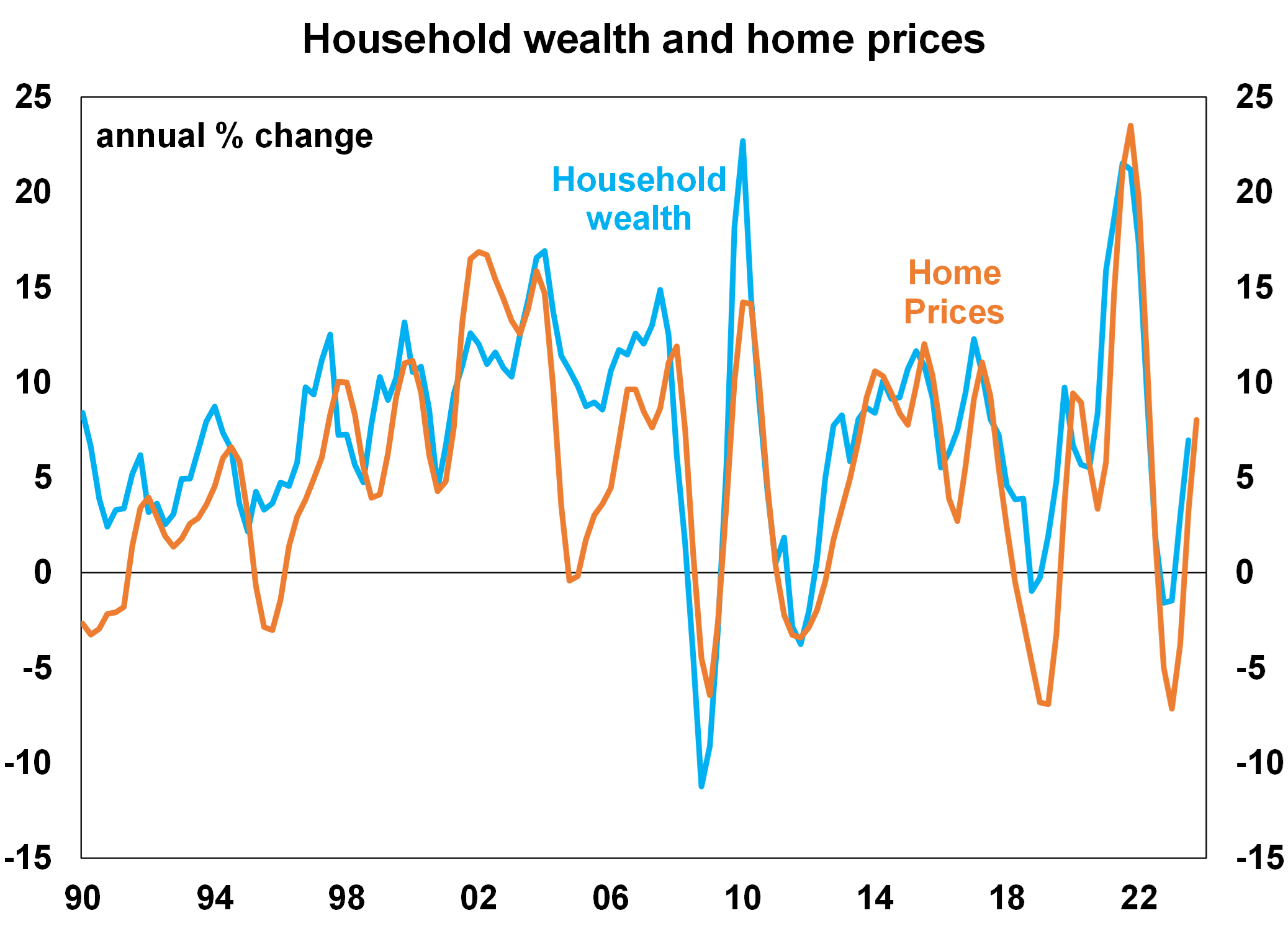

Around 70% of Australian household wealth is tied to the value of homes (which is made up of land and dwellings) and moves closely in line with home prices (see the chart below). Household wealth rose throughout 2023, in line with solid growth in home prices.

Source: ABS, AMP

Other components of household wealth are shown in the chart below. Assets include superannuation, shares and currency and deposits. Loans which are mostly for housing are the source of household liabilities.

Source: ABS, AMP

How does household wealth compare around the world?

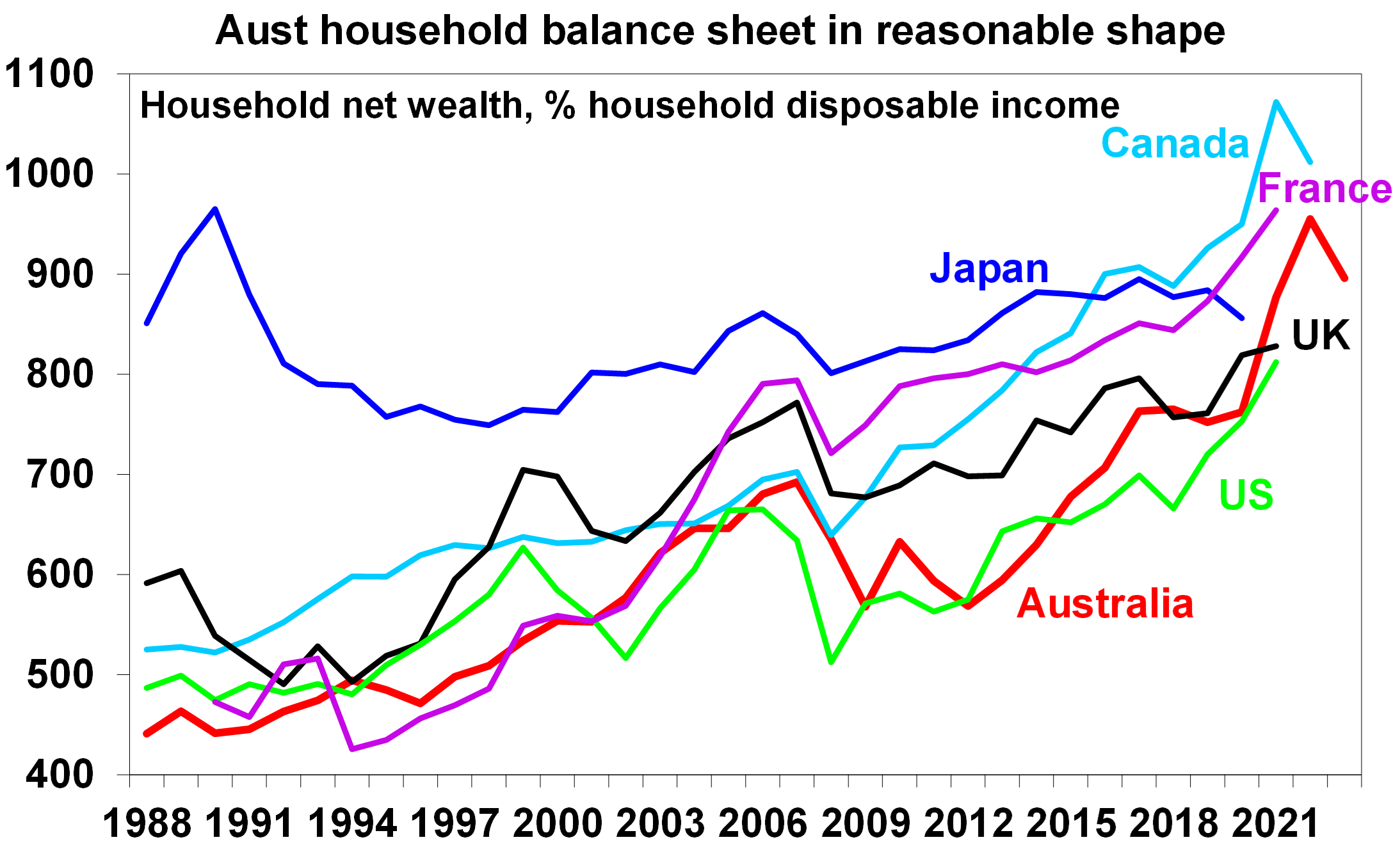

Australian household wealth, as a share of household disposable income, is at the top end of its OECD peers (see the chart below).

Source: OECD, AMP

High holdings of wealth could be considered a source of support for households, especially against record levels of household debt in Australia. This is a concept known as the “wealth effect”. When household wealth increases, households feel more secure with their financial position and household savings tend to decrease which lifts consumer spending. When wealth decreases, households feel less secure which leads to an increase in savings and decline in spending. However, this relationship does not always work. Most recently in the pandemic, household wealth rose in 2021/22 alongside the lift in home prices but the savings ratio also surged thanks to government driven stimulus cheques. Since then, the household savings ratio has been falling but growth in total consumer spending has been low. We expect that the household savings rate will continue to fall in 2024 as it normalises after the pandemic but growth in consumer spending will still be low.

Implications for investors

Households dealt with a cost of living challenge in 2023 because of high inflation and rising interest rates. Inflation is expected to slow in 2024 and we expect the RBA to start cutting interest rates by mid year which should ease the repayment burden for households with a mortgage, as mortgage interest repayments as a share of income are rising to a record high (see the chart below).

Source: ABS, AMP

So, while cost of living issues should improve for consumers, household wealth will come under pressure in 2024 as we expect home prices will decline by 3.0% to 5%. This is likely to occur alongside a slowing in household incomes as the labour market weakens and the unemployment rate increases. This environment is expected to be negative for consumer spending and GDP growth. We see GDP growth rising by 1.2% over the year to June 2024, below the RBA’s forecast of 1.8% and anticipate the unemployment rate to increase to 4.5% by mid year. This should see the RBA cutting interest rates by June and we expect a total of 3 rate cuts in 2024.

Wealth inequality between households is also an issue in Australia. The top 20% of households (by income quintile) owned 63% of total household wealth in 2019-20 but the bottom income quintile (the bottom 20%) owned less than 1.0% of all household wealth. In Australia, there is also increasing generational wealth gap, with wealth across older households increasing significantly over recent decades but this has not been the case for younger Australians. There are numerous government policies that could address these issues of wealth inequality, including improving the housing affordability issue (through lifting housing supply and/or looking at the favourable treatment of housing investment) and doing a tax review (looking at broadening the GST and examining the merits of a wealth or death tax), which could help the wealth inequality issue.

Source: AMP

As scams evolve, so can you

By Robert Wright /February 16,2024/

As scams continue to evolve, it’s important to stay on top of the latest information.

Here are some tips for staying protected against some of the most common scams impacting Australians today and red flags to watch out for.

What can you do to stay protected?

Anyone can fall victim to a scam. As well as learning more about the different types of scams and how to spot them, start a conversation with family members or friends. You might know the red flags to watch out for, but do your loved ones? Raising awareness and educating yourself and others are important steps to help combat scams and even prevent them from happening in the first place.

Three scams to watch out for

Impersonation scams

Have you ever received a call and it just didn’t feel right? It may have been part of an impersonation scam, which is when a scammer impersonates a bank or other service company by phone or SMS, asking you to authorise transactions, make a payment, or provide personal information.

According to the Australian Government’s Anti-Scam Centre, three in four reported scams include some form of impersonation of a legitimate entity1.

So how can you be sure next time that person calling you is really from where they say they’re from? Here’s a few things to remember:

- most financial institutions will never ask you to transfer funds to another account

- never share passwords with anyone

- avoid using phone numbers or links from text messages

- check contact information using a trusted source such as the company’s website.

Investment scams

As of 9 November 2023, Australians have lost $240 million to investment scams2. Investment scams are often sophisticated which means they can be hard to spot. Investment opportunities offering fast results and big returns can have the potential makings of a scam.

Common investment scams include:

- unsolicited investment offers such as cryptocurrency, fake corporate or treasury bonds, and fake share IPOs (Initial Public Offerings), claiming to be from reputable businesses

- fake endorsement of an investment or other business opportunities from celebrities

- early access to superannuation with a fee.

Buyer/seller scams

Buying or selling on an online selling platform is great when it’s quick and hassle-free. But scammers are popping up everywhere, so it’s harder to stay safe online. Here are five red flags to look out for:

- being approached by someone who has no profile photo

- the price seems too good to be true

- a request for personal information such as your phone number or email

- the buyer overpays for an item and wants you to refund the excess amount

- the buyer wants to pay using a gift card or wants to send a prepaid shipping label.

1scamwatch.gov.au

2scamwatch.gov.au as at 9 November 2023

Source: Macquarie