Tag Archives: Budgetting

How much super do I need to retire in Australia?

By Robert Wright /August 22,2025/

The amount of super you need to support your retirement will depend on what kind of lifestyle you’re hoping to enjoy and how much income you’ll be earning in addition to your super savings. Income from the Age Pension, part-time work and other financial investments will affect the amount of super you need to retire comfortably.

The Association of Superannuation Funds of Australia (ASFA) provides yearly total income recommendations based on the type of retirement you’re aiming for. Depending on how much income you expect to receive from other sources, you can then estimate how much super you’ll need to reach the “comfortable” or “modest” benchmarks.

The table below gives you an idea of how much retirement income you might need to enjoy a comfortable, or modest retirement, and compares these benchmarks against how much you can receive on the Age Pension.

| Comfortable lifestyle | Modest lifestyle | Maximum rate of Age Pension | |

| Single | $52,383 | $33,386 | $29,874.00 |

| Couple | $73,875 | $48,184 | $22,518.60 (each) a year |

Budgets for various households and living standards for those aged 65-84 (March quarter 2025)

Source: ASFA Retirement Standard

The amount of super you need will also depend on what you’re earning from full or part-time work, the Age Pension and other investments.

To enjoy a comfortable retirement, AFSA suggests that single people will need $595,000 in super savings at age 67, and couples will need $690,000. But your own individual goal will depend on your other income streams and personal situation.

In addition to the total amount of super you have, the way you access it once you retire can also impact your retirement wealth. For example, your super earnings might be subject to more tax if you plan to withdraw lump sums, compared to setting up a super income stream like an account-based pension.

What’s the difference between a comfortable and modest retirement in Australia?

A comfortable retirement means you can look forward to a broad range of leisure and recreational activities, with a good standard of living. ASFA guidelines suggest you’ll be able to purchase things like private health insurance, a reasonable car, good clothes and a range of electronic equipment. You’ll enjoy domestic and occasionally international, holiday travel.

According to ASFA, you can expect a modest retirement to be better than living on the government Age Pension. However, you’ll only be able to enjoy a fairly basic lifestyle.

See the charts below to get a more detailed understanding of what sort of services and luxuries you might be able to enjoy, based on your retirement savings.

| Comfortable lifestyle | Modest lifestyle | Age Pension | |

| Medical | Top level private health insurance, doctor/specialist visits, pharmacy needs | Basic private health insurance, limited gap payments | No private health insurance. |

| Technology | Fast reliable internet/telco subscription, computer/android mobile/streaming services | Basic mobile, modest internet data allowance | Very basic mobile and limited internet connectivity |

| Transport | Own a reasonable car, car insurance and maintenance/upkeep | Owning a cheaper, older, more basic car | Limited budget to own, maintain or repair a car |

| Lifestyle | Regular leisure activities including club membership, cinema visits, exhibitions, dance/yoga classes | Infrequent leisure activities, occasional trip to the cinema | Rare trips to the cinema |

| Home | Home repairs, updates and maintenance to kitchen and bathroom appliances over 20 years | Limited budget for home repairs, household appliances | Struggle to pay for repairs, such as leaky roofs or major plumbing problem |

| Haircuts | Regular professional haircuts | Budget haircuts | Less frequent haircuts, or self haircuts |

| Home cooling and heating | Confidence to use air conditioning in the home, afford all utilities | Need to keep a close watch on all utility costs and make sacrifices | Limited budget for home heating in winter |

| Eating out | Occasional restaurant meals, home delivery meals, take away coffee | Limited meals out at inexpensive restaurants, infrequent home delivery or take away | Only local club special meals or inexpensive take away |

| Clothing | Replace worn out clothing and footwear items, modest wardrobe updates | Limited budget to replace or update worn items

|

Very basic clothing and footwear budget

|

| Travel | Annual domestic trip to visit family, one overseas trip every seven years | Annual domestic trip or a few short breaks

|

Occasional short break or day trip in your own city |

Annual budgets for households and living standards for those aged 65-84 (March quarter 2025)

Source: ASFA Retirement Standard

Do I need a second income stream in retirement?

This will come down to your personal circumstances, and what kind of lifestyle you’re hoping to enjoy when you retire.

Planning ahead is a great idea if you want to supplement your super with additional streams of income. For example, you could:

- build up your financial investments

- top up your super with salary sacrifice or a personal super contribution

- find part-time employment

- apply for the Age Pension.

What government benefits could I receive?

When you retire, you might be eligible for government benefits like the Age Pension or a concession card. This will depend on your age, your residency status, and your financial situation.

As of 20 March 2025, the maximum Age Pension is:

- $1,149 per fortnight for singles ($29,874 a year).

- $866 each per fortnight for couples ($22,516 a year).

If you’re eligible for the Age Pension, you may also be able to access additional government payments, such as:

- Carer allowance: If you provide daily care to an elderly person or someone with a disability or a serious illness.

- Rent assistance: To help cover your rent if you’re renting privately.

If you’re receiving the Age Pension, the government will automatically send you a Pensioner Concession Card. Even if you’re not eligible for the Pensioner Concession Card, you might still be able to get a Commonwealth Seniors Health Card, subject to being eligible.

Either of these cards will allow you to access:

- cheaper medicines on the Pharmaceutical Benefits Scheme (PBS)

- bulk billing for doctor’s appointments

- reduced out of hospital expenses through Medicare.

Note that there may be additional concessions from state or territory governments, or from local councils and businesses.

How can I set myself up for the retirement I want?

Your first step will be to create a clear vision for the retirement you want. Ask yourself: What type of lifestyle do you want to enjoy in retirement? Modest, comfortable, or would you like even more freedom? Use the table above to figure out what you’d like your retirement to look like.

Secondly, are you currently on track to achieve this goal?

If you’re not quite on track to reach your goal, you can start thinking about strategies to boost your retirement wealth. This might include topping up your current super savings, working part-time, or building up your other financial investments.

If you’re unsure about the best way to set yourself up for a retirement which supports your personal goals, a financial adviser can help steer you in the right direction.

Calculating how much super is needed for retirement

A retirement calculator helps you estimate how much money you’ll need for the retirement lifestyle you want – and how much money you might have when you retire, based on your super savings and other assets.

The calculator will also show you the impact of potential investments, fees and voluntary contributions to your super and your retirement wealth.

Consider the ASFA benchmarks for a modest and comfortable retirement, other income streams like part-time work or investments and your own financial goals when determining how much super you’ll need when you retire.

How can I grow my super?

Topping up your super is a good way to boost your retirement wealth and may provide tax-concessions in the short term.

Currently, your employer must pay 12% of your ordinary time earnings into your nominated super fund. These contributions are called Superannuation Guarantee (SG) contributions. However, there are a few different ways you can contribute more of your own money towards your super.

As super compounds each year, even a small contribution can go a long way towards building up your retirement wealth so you can enjoy the type of retirement you want.

If you’re still not sure about the best way to set yourself up for retirement, consider speaking with a financial adviser. They’ll review your personal situation and help you find the solution which best suits your life stage, financial goals and risk tolerance.

Source: Colonial First State

Reserve Bank cuts interest rates by 0.25 percentage points in August in unanimous decision

By Robert Wright /August 22,2025/

In short:

The Reserve Bank cut interest rates by 0.25 percentage points in August to 3.6 per cent, after July’s shock ‘on hold’ decision.

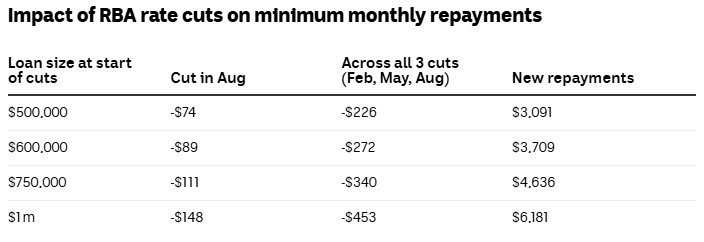

The average owner-occupier with a $750,000 mortgage as of February will see their minimum monthly repayment fall $111 if their bank passes on the cut, taking the cumulative reduction this year to $340, according to Canstar.

What’s next?

The next RBA rates decision will be delivered on September 30. After that, there are two further meetings this year, in November and December.

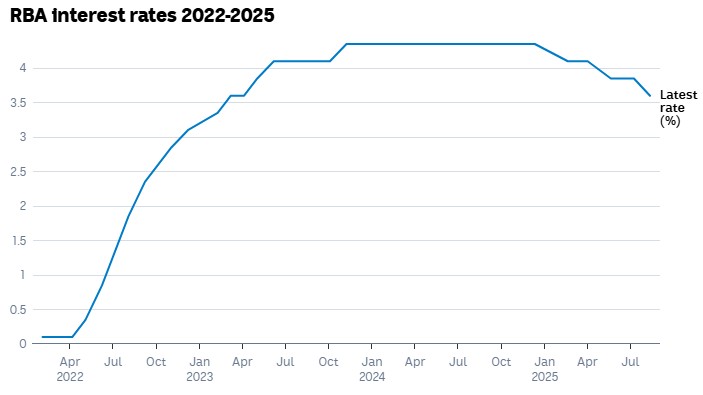

The Reserve Bank has delivered its third interest rate cut of 2025, with a 0.25 percentage point reduction at its August board meeting.

That takes the cash rate to 3.6 per cent for the first time since April 2023.

The move had been overwhelmingly anticipated by financial markets and economists after the surprise decision to hold rates steady in July.

It was a unanimous decision by board, which had been divided last month.

Tuesday’s cut follows a further easing of inflation in the June quarter, which RBA governor Michele Bullock last month highlighted as the crucial piece of data the monetary policy board was waiting for.

“Updated staff forecasts for the August meeting suggest that underlying inflation will continue to moderate to around the midpoint of the 2–3 per cent range, with the cash rate assumed to follow a gradual easing path”, the post-meeting statement read.

ABC News / Source: Reserve Bank of Australia

The inflation pull back, alongside “labour market conditions easing slightly, as expected”, led the board to deem “further easing of monetary policy was appropriate”.

“This takes the decline in the cash rate since the beginning of the year to 75 basis points”, the RBA board noted in its statement.

The central bank cut interest rates at its February and May board meetings.

Before that, the RBA’s cash rate had sat at 4.35 per cent since November 2023, after a series of 13 rate hikes, beginning in May 2022.

Treasurer Jim Chalmers described it as a “very welcome relief for millions of Australians”.

“It means the lowest interest rates for more than two years”, he said shortly after the decision.

“It reflects the substantial and sustained progress we’ve made on inflation in a volatile and uncertain global environment”, the treasurer noted in a statement.

Cash rate at 3.6pc, further rate cuts expected

The Australian dollar fell following the decision, dipping just below 65 US cents as Ms Bullock addressed a media conference in Sydney.

The RBA governor indicated the board was prepared to cut interest rates further if necessary.

“The forecasts imply that the cash rate might need to be a bit lower than it is today to keep inflation low and stable, and employment growing, but there is still a lot of uncertainty”, Ms Bullock told reporters.

“The board will continue to focus on the data to guide its policy response”.

Where are rates heading?

The Reserve Bank’s economic outlook suggests further room to cut interest rates, but it’s not all good news for most working-age Australians.

Betashares chief economist, David Bassanese has forecast further interest rate cuts, with the next easing more likely in November, rather than at the next meeting in September.

“Indeed, the [central] bank’s own forecasts of underlying inflation stabilising at 2.6 per cent over coming quarters incorporate further declines in the cash rate in line with current market expectations”, he wrote.

“That said, barring a major growth scare, the RBA does not seem in any rush to cut interest rates.

“All up, my base case remains that a rate cut on Melbourne Cup day is an odds on favourite –following release of the June quarter consumer price index report in late October”.

The governor would not be drawn on what specific cash rate the central bank considers to be “neutral” – that is, the level where the rate is not stimulating or putting a handbrake on the economy.

Instead, she gave a “very wide range” of between 1 and 4 per cent, and noted a neutral rate is for when there is an absence of economic shocks.

“We are very often not in the absence of shocks … we’ve got shocks, particularly at the moment”.

While the central bank’s forecasts put inflation around target over the period ahead, it has downgraded its growth forecasts.

It now expects gross domestic product (GDP) expanded 1.6 per cent over the year to June (compared to 1.8 per cent forecast in May); and GDP growth to only pick up to 1.7 per cent by the end of the year (it had previously forecast 2.1 per cent).

“Its forecasts assume that the cash rate will continue to ‘follow a gradual easing path’, implying that without further easing growth and inflation will be lower and unemployment higher”, AMP chief economist, Shane Oliver said.

AMP has forecast further rate cuts in November, February and May to take the cash rate to 2.85 per cent.

“We continue to see further rate cuts as growth remains sub par, the risks to unemployment are on the upside, underlying inflation is likely to remain around the 2.5 per cent target and monetary policy remains tight”, Dr Oliver wrote.

How much will home loan repayments fall?

Some lenders were quick off the mark to confirm they would be passing on the interest rate cut to home loan customers, with Macquarie, Commonwealth Bank, Westpac, ANZ, NAB and AMP among the first handful of announcements.

The cumulative effect of three rate cuts so far this year have added up to a substantial reduction in minimum mortgage repayments for many home loan borrowers.

According to calculations by financial comparison site Canstar, the savings from this month’s cut range from $74 on a half a million dollar mortgage, to $148 on a $1 million home loan.

Based on an owner-occupier paying principal and interest with 25 years remaining in Feb 2025 at the RBA average existing customer variable rate. Calculations assume the banks pass on each cut in full to existing variable customers the month after.

Source: Canstar.com.au

The numbers are based on an owner-occupier repaying principal and interest, who had 25 years remaining on their loan in February.

The estimates assume borrowers were paying the average variable rate of 5.79 per cent, which would fall to 5.54 per cent after Tuesday’s 0.25 percentage point cut, and that lenders pass on cuts in full to existing variable customers the following month.

Home loan borrowers are not obliged to lower repayments, and, in fact, most do not – last month, Commonwealth Bank released data showing only one in 10 eligible home loan customers reduced their mortgage direct debits after the rate cut in May.

If borrowers continue to make repayments above the minimum required, they will pay down more of the principal as the interest reduces, and pay off their loan faster.

Source: ABC News

Using the bucket strategy to make your money last longer

By Robert Wright /February 28,2025/

How do you find the sweet spot between using your retirement savings to enjoy a comfortable standard of living, and investing so you won’t run out of money in the future? It’s a big question for many retirees.

Two in three retirees (69%) are concerned about running out of money in retirement, according to new research from Colonial First State (CFS)*.

A total of 41% said they sometimes felt so concerned about running out of money that it affected how they used their retirement savings and their current standard of living. A further 28% said this fear affected them significantly. Just one in three said they never worried about it.

With that in mind, it’s worth understanding what’s known as the ‘bucket strategy’ for how to manage your savings in retirement.

This strategy was conceived as a way for retirees to balance spending with the need to preserve capital and invest to grow your future retirement savings to last the distance.

How much you put into each bucket, and how you invest those buckets will depend on your level of retirement savings, the lifestyle you want in retirement, your risk appetite and any other income you may have. It’s worth getting financial advice to ensure this approach is right for you.

What is the bucket strategy?

Simply put, the bucket strategy involves keeping your money in different investment types designed to deliver short term, medium term and long term returns.

- Short term bucket: This is money you think you’ll need to access in the next one to three years. Consider keeping it in cash, such as high yield savings accounts or term deposits with staggered maturity dates.

This is money to live on and perhaps an emergency fund for those unexpected expenses, such as when your washing machine stops working or your car conks out.

There should be enough to get you through a market downturn if needed, so you don’t need to cash in higher growth investments and turn paper losses into real ones or sell units in your pension investment option when they may have experienced a short term drop in value.

Factor in any other income, such as the Age Pension if you receive it, or any work income, and set aside money to cover the rest.

- Medium term bucket: Consider holding money you may need in the next four to six years in income producing, relatively ‘safe’ assets like high quality bonds, fixed income investments, low risk, dividend paying stocks or a balanced pension investment option.

This bucket is designed to help your retirement savings keep pace with inflation. If you hold too much in cash, your retirement savings won’t grow very quickly.

- Long term bucket: This is the money you want to invest to grow over the long term. It can be kept in higher growth investment types that are often seen as higher risk, such as a growth pension investment option or growth shares.

This should be money you won’t need to touch for seven to 10 years, which gives it time to grow irrespective of any short term market volatility that may occur.

More than half your retirement savings may be generated from earnings on your pension investment option after you have retired^, so it’s worth quarantining a good amount in your long term bucket.

How does it work?

The bucket strategy is intended to balance the need to preserve your capital in retirement by putting some of your savings into low risk cash options.

This enables retirees to access income when you need it without dipping into higher growth investments that will grow your retirement savings over the long term and can therefore provide peace of mind about spending while also helping your retirement savings last longer.

It can be particularly beneficial in times of market volatility, such as if there is a market downturn, to prevent you having to sell higher risk investments at an inopportune time.

Keeping all your retirement savings in conservative investment options or cash that may not keep pace with inflation may be low risk but it won’t provide you with the best retirement outcomes over the long term.

As the funds in bucket 1 are used, consider topping it up from bucket 2, or even bucket 3, depending on market conditions, what you’re invested in, and how your investments are performing.

As mentioned, how much you put into each bucket, and how you invest those buckets will differ depending on your individual situation. It’s worth getting financial advice to ensure this approach is right for you.

And this strategy may require more active management of your retirement savings than some people may be comfortable with.

But the bucket strategy offers built in diversification by incorporating different investment types and time frames and can be useful for helping you decide how much to spend and how much to invest for the long term.

* Financial literacy and retirement study conducted between July and September 2024. Respondents included 834 retiree respondents.

^ Calculations by CFS. Projection starts at age 25 (with salary of $100,000), retirement at age 65 and super lasts until age 92. Superannuation earnings, tax on earnings, investment and administration fees, and yearly indexation of contributions and income stream payments, are based on the default assumptions used in ASIC’s Moneysmart calculator, available at moneysmart.gov.au as at August 2024.

Source: CFS

Mortgage vs super: where should I put my extra money?

By Robert Wright /February 16,2024/

It’s a dilemma many of us face – are we better off directing extra money to our mortgage or super? As with most financial decisions, it’s not a one size fits all approach and here are some factors to consider in deciding what’s right for you.

Key takeaways:

- There may be tax advantages when you contribute to super, especially if you salary sacrifice or you’re eligible to claim a tax deduction for personal super contributions.

- The power of compounding returns could mean that even small contributions to your super over many years could make the world of difference.

- By making extra mortgage repayments, coupled with any potential increase in the value of your property, you will build equity in your property at a faster rate than if you were to make just the minimum repayments.

Building the case for super over mortgage

You might think your super is already being taken care of – after all, that’s what your employer’s compulsory Superannuation Guarantee contributions are all about. But these contributions alone often aren’t enough to ensure you achieve the retirement lifestyle you want to live.

Making extra contributions to your super is a great way to boost your retirement savings. As an investment vehicle, super is a very tax effective way to save for the future.

The power of compounding returns

Super is a long term investment, at least until you retire, and potentially much longer if you leave your money in super and draw a pension after you retire.

This long investment term, coupled with the rate of tax on your super investment (generally 15%), means your money can add up and generate further investment returns on those returns. This is known as compound returns, or compounding.

The expenses of daily life can be considerable. Thinking about directing money to super might not seem like a priority when we feel overwhelmed by the effort to save a deposit for a home, paying down debt, and the costs of raising a family.

However, the benefit of compounding returns means that even small, frequent contributions can make a big difference down the track. It’s about striking a balance that is right for you today and remember, nothing has to be forever. As your life changes, you can simply adjust your contributions strategy to suit your needs.

Building super early

To maximise your retirement savings while allowing compounding returns to do the heavy lifting, the best approach is to start early. The longer compounding continues, the bigger your savings could be. Entering retirement debt free is an attractive prospect. It can be easy to think that you need to repay your debt before you can start thinking about saving for retirement. However, it doesn’t have to be one or the other.

You can see the difference small, regular contributions could make to your final retirement income using the MoneySmart retirement planner calculator.

Tax benefits of super

From a tax point of view, super can be incredibly beneficial. Salary sacrificing some of your before-tax salary or making a voluntary after-tax contribution for which you can claim a tax deduction, can be effective ways to not only grow your retirement savings but also reduce your taxable income.

One great benefit of investing in super is that concessional (before tax) contributions are taxed at a maximum rate of 15%. This can be higher though if you earn over $250,000.

Mortgage repayments are usually made from your take home pay after you’ve paid tax at your marginal tax rate. Your marginal tax rate could be as high as 47%. So, depending on your circumstances, making a voluntary deductible contribution to super or salary sacrificing may result in an overall tax saving of up to 32%.

There is a limit on the amount you can contribute into super every year. These are referred to as contribution caps. Currently, the annual concessional contributions cap is $27,500. If you’re eligible to use the catch-up concessional contributions rules, you may be able to carry forward any unused concessional contributions for up to 5 years. If you exceed these caps, you may be liable to pay more tax.

Tax on super investment earnings

The initial tax savings are only part of the story. The tax on earnings within the super environment are also low.

The earnings generated by your super investments are taxed at a maximum rate of 15%, and eligible capital gains may be taxed as low as 10%. Once you retire and commence an income stream with your super savings, the investment earnings are exempt from tax, including capital gains.

Also, when it comes time to access your super in retirement, if you’re aged 60 or over, amounts that you access as a lump sum are generally tax free.

However, it’s important to remember that once contributions are made to your super, they become ‘preserved’. Generally, this means you can’t access these funds as a lump sum until you retire and reach your preservation age, between 55 and 60 depending on when you were born.

Before you start adding extra into your super, it’s a good idea to think about your broader financial goals and how much you can afford to put away because with limited exceptions, you generally won’t be able to access the money in super until you retire.

In contrast, many mortgages can be set up to allow you to redraw the extra payments you’ve made or access the amounts from an offset account.

Building the case for reducing your mortgage over super

For many people, paying off debt is the priority. Paying extra off your home loan now will reduce your monthly interest and help you pay off your loan sooner. If your home loan has a redraw or offset facility, you can still access the money if things get tight later.

Depending on your home loan’s size and term, interest paid over the term of the loan can be considerable – for example, interest on a $500,000 loan over a 25-year term, at a rate of 6% works out to be over $460,000. Paying off your mortgage early also frees up that future money for other uses.

Before you start making additional payments to your mortgage, it’s suggested that you should first consider what other non-deductible debt you may have, such as credit cards and personal loans. Generally, these products have higher interest rates attached to them so there is greater benefit in reducing this debt rather than your low interest rate mortgage.

Conclusion: mortgage or super

It’s one of those debates that rarely seems to have a clear-cut winner – should I pay off the mortgage or contribute extra to my super?

The answer, probably somewhat annoyingly, is that it depends on your personal circumstances.

There is no one size fits all solution when it comes to the best way to prepare for retirement. On the one hand, contributing more to your super may increase your final retirement income. On the other, making extra mortgage repayments can help you clear your debt sooner, increase your equity position and put you on the path to financial freedom.

When weighing up the pros and cons of each option, there are a few key points to keep in mind.

One of the key questions to consider is what is the likely balance you’ll need in your super? Work backwards starting with working through what retirement looks like for you, the type of lifestyle you’d like, and how much you need to live on each year.

From there, you can start to consider your sources of income in retirement. This is likely to include super but could also include a full or part Age Pension, or income from an investment property or other sources.

You can then start thinking about your current balance, contributions strategies and whether you’re on track to have enough saved to supplement your other retirement income sources.

The MoneySmart retirement planner calculator can help you to estimate how much super you may have in retirement and how long your super may last. You also need to think about how you plan to spend your money in retirement.

In most cases, there isn’t one set strategy that you should follow and it can quickly change as you grow older, start a family and reach retirement age. You should also consider whether you’ll need to access any additional funds you put aside before you reach retirement. If it’s in your super, it’s locked away. If it’s in your mortgage, there are generally options to redraw.

Home ownership and comfortable retirement are financial goals that many strive towards. If you reach a point where there’s some surplus cash flow to consider where to put your extra money, it’s a good dilemma to have.

Life is complex, so it pays to speak with a financial adviser before you make any big financial decisions when it comes to your super or mortgage.

Source: MLC