Tag Archives: COVID

Seven lasting impacts from the COVID pandemic

By Robert Wright /May 28,2024/

Key points

- Seven key lasting impacts from the Coronavirus pandemic are: “bigger” government; tighter labour markets; reduced globalisation and increased geopolitical tensions; higher inflation; worse housing affordability; working from home; and a faster embrace of technology.

- On balance these make for a more fragmented and volatile world for investment returns. But it’s not all negative.

Introduction

It’s four years since the COVID lockdowns started. The pandemic ended when it morphed into the less deadly Omicron variant in late 2021, but just as a sound can reverberate around a room the effects of the pandemic continue to reverberate in economies. Putting aside the long-term health impacts this note looks at 7 key lasting economic impacts.

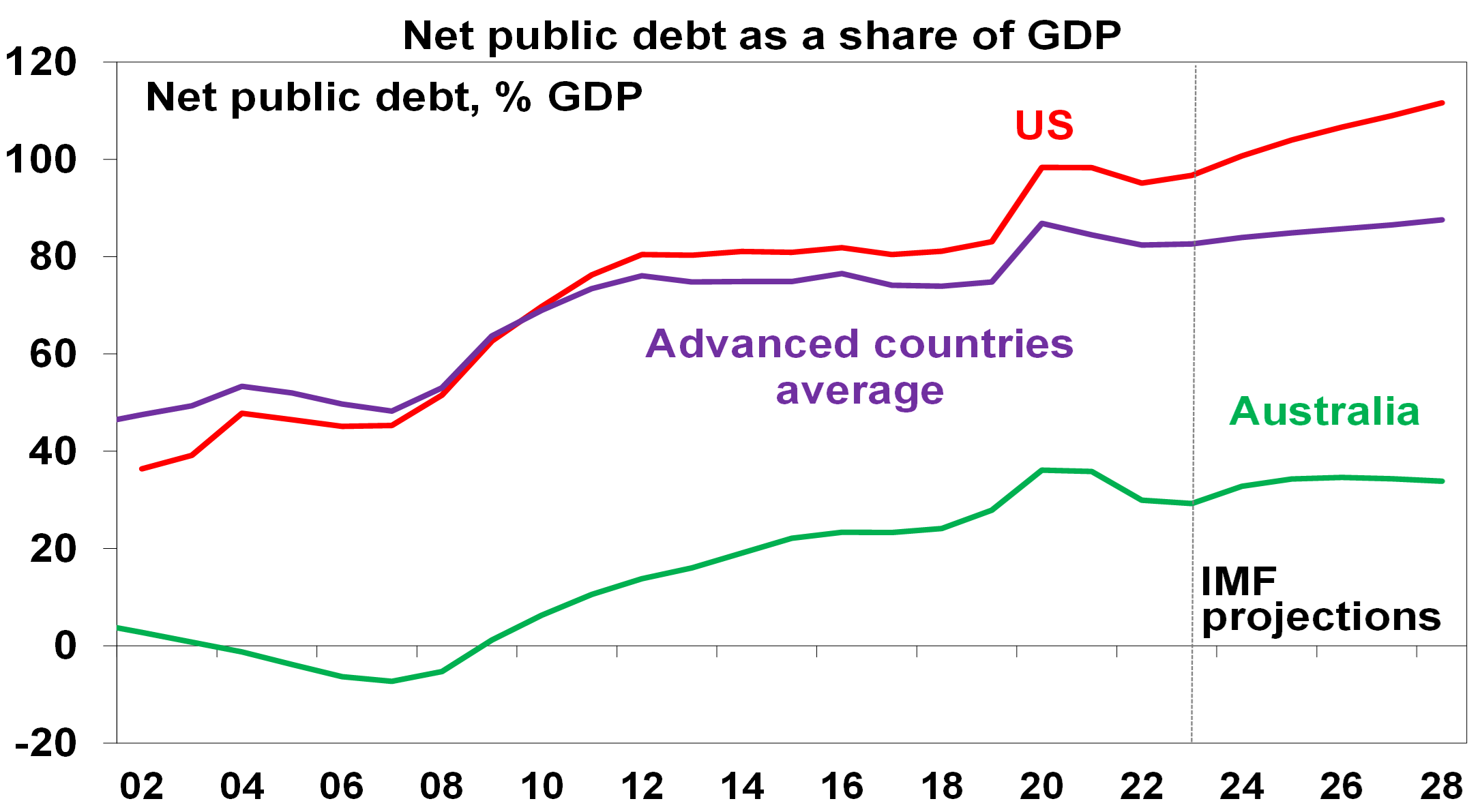

- Bigger government and more public debt

The malaise of the 1970s ushered in “smaller” government in the 1980s in the Thatcher, Reagan, Hawke and Keating era. But the political pendulum started to swing back to “bigger” government after the GFC and COVID has given it another push. Memories of the problems of high government intervention in the 1970s have faded and there is rising support for the view that government is the solution to most problems – via regulation, taxes, spending or education campaigns. The pandemic added to support for “bigger” government: by showcasing the power of government to protect households and businesses from shocks; enhancing perceptions of inequality; and adding support to the view that governments should ensure supply chains by bringing production back home. It’s combining with a desire for governments to pick and subsidise clean energy “winners”.

Source: IMF, Australian Government, AMP

IMF projections for government spending in advanced countries show it settling nearly 2% of GDP higher than pre-COVID levels. The success of governments in protecting households from the worst of the pandemic has also reinforced expectations they would do the same in the next crisis. The pandemic ushered in even bigger public debt just as the GFC did. While high inflation helped lower debt to GDP ratios in 2022 it’s settling at higher levels than pre-pandemic.

Source: IMF, AMP

Implications – While there may initially be a feel good factor, the long-term outcome of “bigger” government is likely to be less productive economies, lower than otherwise living standards and less personal freedom. It will take time before this becomes apparent though. Meanwhile, higher public debt means: less flexibility to respond with fiscal stimulus to a crisis; a greater incentive for politicians to inflate their way out; and interest payments being a high share of tax revenue.

- Tighter labour markets and faster wages growth

In the pre-pandemic years, wages growth was relatively low and a key driver was high levels of underemployment, particularly evident in Australia. After the pandemic, labour markets have tightened reflecting the rebound in demand post pandemic, lower participation rates in some countries and a degree of labour hoarding as labour shortages made companies reluctant to let workers go. As a result, wages growth increased, possibly breaking the pre-pandemic malaise of weak wages growth.

Source: ABS, AMP

Implications – Tighter labour markets run the risk that wages growth exceeds levels consistent with 2% to 3% inflation.

- Reduced globalisation/more geopolitical tensions

A backlash against globalisation became evident last decade in the rise of Trump, Brexit and populist leaders pushing a nationalist gender when the benefits of free trade were being questioned. Also, geopolitical tensions were on the rise with the relative decline of the US and faith in liberal democracies waning resulting in a shift from a unipolar world dominated by the US, to a multipolar world as regional powers (Russia, Iran, Saudi Arabia and notably China) flexed their muscles. The pandemic inflamed both – with supply side disruptions adding to pressure for the onshoring of production; conflict over the source of and management of coronavirus; it heightened tensions between the west and China; and it appears to have added to nationalism and populism. So, the days of global free trade agreements and falling defence spending seem long gone for now. Rather we are seeing more protectionism (e.g. with subsidies and regulation favouring local production) and increased defence spending.

Implications – Reduced globalisation risks leading to reduced potential economic growth for the emerging world and reduced productivity if supply chains are managed on other than economic grounds. And combined with increased geopolitical tensions resulting in more defence spending it could result in a more inflation prone world than was the case.

- Higher prices, inflation and interest rates

A big downside of the pandemic support programs was the surge in inflation. The combination of massive money printing along with a big increase in government payments to households (e.g. Job Keeper) resulted in a massive boost to spending once lockdowns were lifted which combined with supply chain disruptions, also flowing from the pandemic, to cause a surge in inflation. Inflation is now starting to come under control as the monetary easing and spending boost has been reversed and supply has improved again but the pandemic has likely ushered in a more inflation prone world by boosting “bigger” government; adding to a reversal in globalisation; and adding to geopolitical tensions. All of which combine with aging populations to potentially result in more inflation.

Implications – Higher inflation than seen pre-pandemic means higher than otherwise interest rates over the medium term which reduces the upside potential for growth assets like shares and property.

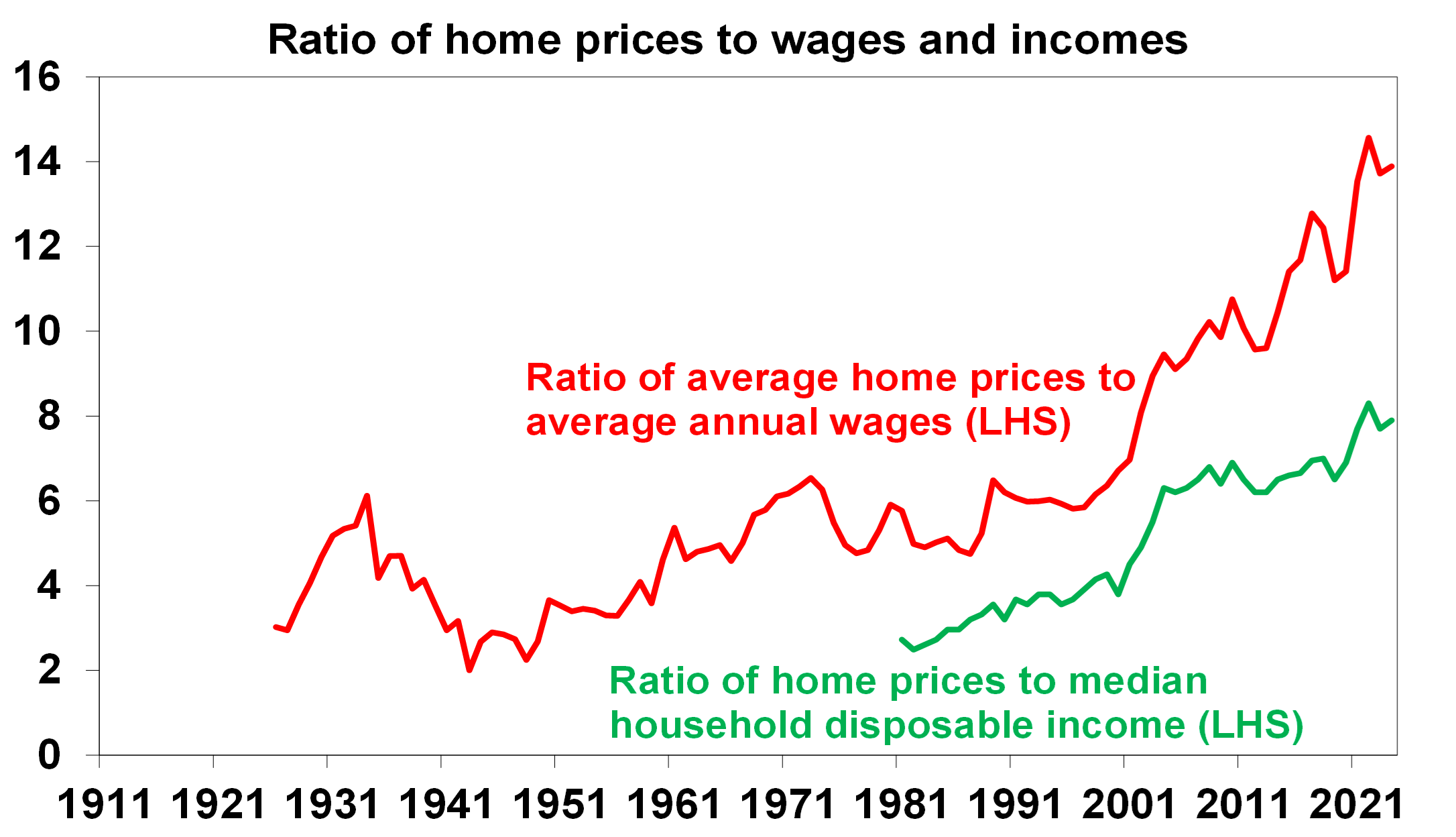

- Worse housing affordability

At the start of the pandemic, it was thought the economic downturn and higher unemployment and a freeze in immigration would cause a collapse in home prices and they did initially fall. But not by much as it was quickly turned around by policy measures to support household income, allow a pause in mortgage payments and slash interest rates and mortgage rates to record lows. What’s more the lockdowns and working from home drove increased demand for houses over units and interest in smaller cities and regional locations. As a result, Australian home prices surged to record levels. Meanwhile the impact of higher interest rates in the last two years on home prices was swamped by housing shortages as immigration surged in a catch up. The end result is now record low levels of housing affordability for buyers (who are hit by a double whammy of higher prices relative to incomes – see the next chart – and higher mortgages rates) and renters (who have seen surging rents).

Source: ABS, CoreLogic, AMP

Implications – Ever worse housing affordability means ongoing intergenerational inequality and even higher household debt.

- Working from home likely here to stay

While there has been a return to the office, for many its only two or three days a week. Basically, the lockdowns resulted in a step jump towards working from home (WFH). A UK study of over 2000 firms is indicative. It showed that while around 90.8% of employees were fully onsite in 2018, last year this had fallen to 62.3%, with 30.2% with hybrid (working in the office and at home) arrangements. Similarly, the ABS found 37% of employed people in Australia regularly worked from home. Of course, this masks a huge range with industries with a high proportion of computer-based workers having more hours working at home. And firms expect this to remain the case. There are huge benefits to physically working together around culture, collaboration, idea generation and learning but there are also benefits to working from home with no commute time, greater focus, less damage to the environment, better life balance and for companies – lower costs, more diverse workforces and happier staff. So the ideal is probably a hybrid model. The proportion of workers in a hybrid model may even rise as new firms are quicker to embrace WFH.

Working arrangements for UK employees

Source: K Shah, and others, Managers say working from home here to stay, CEPR

Implications – Less office space demand as leases expire resulting in higher vacancy rates/lower rents, more people living in cities as vacated office space is converted and reinvigorated life in suburbs and regions.

- Faster embrace of technology

Lockdowns dramatically accelerated the move to a digital world. Everyone was forced to embrace new online ways of doing things. Many have now embraced online retail, working from home and virtual meetings. It may be argued that this fuller embrace of technology will enable the full productivity enhancing potential of technology to be unleased. The rapid adoption of AI will likely help.

Implications – This has meant a faster embrace of online retailing (up from 7% of retailing pre-pandemic to around 11%) at the expense of traditional retailing, virtual meeting attendance becoming the norm for many (even in the office) and business travel settling at a lower level.

Concluding comments

Perhaps the biggest impact is that the pandemic related stimulus broke the back of the ultra-low inflation seen pre-pandemic. Together with bigger government and reduced globalisation, this means a more inflation-prone world. So, a return to pre-pandemic ultra-low inflation and interest rates looks unlikely. It’s not all negative though – apart from the faster technology uptake, the global and Australian economies have come through the last four years in far better shape than might have been imagined at the start of the lockdowns!

Source: AMP

Market volatility during COVID-19

By Robert Wright /November 17,2021/

Market volatility refers to extreme price movements over a given period. These movements may occur in a particular area, such as real estate or shares, and may be upward or downward.

Ever since COVID-19 started spreading across the world in late 2019, affecting every aspect of our lives, the term ‘market volatility’ has been hitting headlines.

But, what does market volatility mean? And what might it mean for your finances?

Market volatility can feel like a one-off crisis. However, it’s important to remember that volatility is in the very nature of markets. Fluctuations are bound to occur and, sometimes, they’re rather extreme.

For instance, in February and March 2019, markets dropped 37%, but fast-forward to the June quarter, and they picked up 16%. That’s quite a wild swing. Anyone who panicked and withdrew from the market at the end of March would have missed out on the subsequent gains.

In the scheme of things, three months isn’t long at all. In the 141 years since the ASX was established, there have been 28 negative years, and the rest have been positive. In other words, each year, the average investor has a 1 in 5 chance of a setback, but a 1 in 4 chance of making gains.

Further, in the 20 years leading up to 2018, the ten best days in the market were responsible for 50% of returns.

During downturns, it’s easy to be swayed by the news. Headlines often focus on the negatives. When the COVID-19 pandemic began, the emotional impact of worrying financial news was intensified by the fact that the virus itself was new and unknown. Plus, so many people were unable to go to their workplaces, or catch up with friends and relatives.

If you were reading the headlines and not speaking to anyone about them, you may have been susceptible to making big financial decisions based on your emotional reactions.

That’s why it’s important to speak to your financial adviser, who will remind you of your long term plan—and that a downturn is just a short term blip, when you think of the next 20 years.

Source: TAL

What you can claim when working from home

By Robert Wright /June 11,2021/

Setting up a home office? Here’s how to create a comfortable workspace, while offsetting the extra costs of working remotely. If you’re among those who’s decided to say ‘so-long’ to the office, you’ve probably also realised that having the right home-office set up is essential for your productivity – and sanity.

As many of us learnt during lockdown, trying to fit in a full day’s work at the dining room table isn’t always the most productive option.

You might also have noticed what many freelancers have known for years: Working from home comes with extra costs, as does setting up your home office.

So, what do you need to do to get your workspace set up for productivity – and comfort – and how can you offset the extra costs that come with working from home?

Getting ergonomic

For most computer work, there’s a few key areas you need to customise to suit you:

- The height of your desk and chair. You’ll know you’ve gotten this right when your forearms are parallel to the ground, with your wrists either straight, at or below shoulder level. Your knees should be level with your hips and feet flat on the ground, or on a footrest.

- Your monitor set up. Your monitor needs to be straight in front of you, an arm’s length away. The top of the screen should be at or slightly below eye level. Use a monitor riser if needed to get your monitor to the right height. Also consider the brightness of your display – it should be just a little brighter than surrounding ambient light.

- Location of key objects. Place your keyboard and mouse on the same level surface and keep other items you use often within easy reach. If you use the phone a lot, put it on speaker or use a headset to avoid neck and shoulder strain.

- Light sources. You’ll need sufficient ambient light to illuminate your workspace, so that you’re not straining your eyes. Beware of indirect lighting from windows that can cause glare on your monitor screen.

Getting (and expensing) equipment

Setting up an ergonomic workspace can involve a bit of gear, even if there are some inexpensive home solutions. At the very least you’ll need a computer, decent office chair, full size monitor, keyboard, and mouse. You may also need to add in a footrest, monitor riser, laptop dock or stand, headset, lighting, and any other office equipment you use regularly, like a printer.

This can add up to quite a hefty price tag! But don’t worry, it’s unlikely you’ll need to foot the entire bill yourself.

If you’re a company employee, start by speaking to your employer. Many companies will offer to either source equipment for you, lend it to you or reimburse you for purchase/s you make.

Under Workplace Health and Safety Laws, employers still have a duty to ensure the health and safety of workers, even if they’re working from home. In fact, some companies will already have occupational health and safety policies that mandate an ergonomic set up using a certain type of office equipment.

Tax deductions: What can I claim?

While you can save money by working from home (less transport costs, homemade lunches, no need for fancy clothes) it does come with other costs (and paperwork) you may not have thought about.

Fortunately, you’re allowed to offset many of these costs against your earnings by claiming a deduction in your annual tax return. According to the ATO, expenses you can claim a deduction for include:

- the cost of electricity for heating, cooling, and lighting the area you’re working in, and running items you’re using for work.

- cleaning costs for a dedicated work area.

- phone and internet expenses

- computer consumables (for example, printer paper and ink) and stationery

- home office equipment, including computers, printers, phones, furniture, and furnishings. You can claim either the

- full cost of items up to $300

- decline in value (depreciation) for items over $300.

To make a claim, you need to have spent the money and have a record to prove it. You can’t claim a deduction where you’ve been reimbursed by your employer for the expense.

Tax deductions: How do I claim?

Because it can be tricky to track and report on your expenses when working from home, the ATO has introduced a temporary ‘shortcut method’. This is now in place up until 30 June 2021 (and may be extended further).

The shortcut method allows you to claim a deduction of 80 cents for each hour you work from home. It covers all the deductible expenses listed above. You’ll need to keep a record of the hours you worked, in the form of a roster, diary, timesheet or similar.

With remote work now widely accepted, many people can’t wait to give hour-long commutes, open plan offices and office politics the flick for good. Just make sure you take the time to get your office set-up right and avoid those nasty repetitive strain injuries in years to come.

Source: FPA Money and Life

How to keep your super safe during COVID-19

By Robert Wright /October 16,2020/

If you’re feeling concerned about how the pandemic will affect your super balance, here are our tips to help protect and grow your super.

What can affect my super balance?

In Australia, your employer is required by law to pay a minimum percentage of your eligible income to a complying superannuation fund or retirement savings account. This is known as the Superannuation Guarantee and it’s currently set to 9.5%.

Your super contributions are then invested by your superannuation fund on your behalf, according to your chosen investment options. This means your super is subject to normal market fluctuations.

Your super is also exposed to a range of administrative fees, charges and premiums, which can eat away at your balance if you’re not vigilant.

Isn’t my super protected by law?

You might be surprised to learn that your superannuation savings are not protected by the government.

Last year, the federal government introduced a package of reforms to help stop low account balances from being eroded by unnecessary insurance premiums and fees. This was called the Protecting your Superannuation Package.

However, this protection only applies to accounts that meet certain criteria, such as having a balance below $6000, and not receiving any contributions for 16-months. These inactive or low-balance accounts are transferred to the ATO for administration. You can find out more about the reforms on the ATO website.

For everyone else, it’s up to you to keep an active eye on the health of your super.

So, here are five things you can do to help conserve and grow your superannuation, even during a global economic downturn.

1. Check your superannuation investment options

Because superannuation is a long-term investment, it’s important to check that your selected investment options are right for your age and stage of life.

Taking on the wrong level of risk at the wrong time in your life can erode your super balance. For example, when you’re starting out, there’s more time until retirement to ride out some of the ups and downs that come with higher levels of risk. But as you near retirement, you might want to focus on preserving your superannuation balance.

If you’re not sure how your super is invested, take the time to check your account either online or by contacting your super fund for advice. Be sure to find out whether they charge fees for advice, as these can be deducted from your super balance.

2. Switch to a low-cost superannuation provider

Fees and charges are deducted directly from your account, so they can quickly erode your super balance. Check your statements regularly and make sure you’ve compared your super fund with other providers.

3. Avoid withdrawing your super early

Most people can access their super once they reach the ‘preservation age’, which is between 55 and 65 years old, depending on when you were born.

There are also some special circumstances where you may be able to access your super early, such as severe financial hardship, including COVID-19.

While a cash injection of $10,000 or $20,000 might sound like a welcome relief when you’re struggling to pay your basic living costs, it’s important that you exhaust all other avenues first, because accessing your super early can have a significant impact on your retirement income.

How significant? Well, the FPA estimates, conservatively, every $1000 you have in super at age 30 is worth $4500 by the time you reach 60. Multiply that by $10,000 or $20,000 and you can see what you might be missing from your retirement nest egg.

For this reason, it’s really important to explore other options first and get expert advice from a financial planner before making a withdrawal.

4. Make regular contributions

One of the ways to protect and grow your super balance is to consider making regular contributions. You can do this by salary sacrificing a set amount every week. If that’s not possible, you could consider making extra contributions whenever possible, such as depositing your tax return, gifts or bonus.

5. Get professional advice

You can’t beat professional financial advice to help you reach your retirement goals. A financial planning professional can review your unique situation and goals and advise you on the right investment and contribution strategies for you. They can also advise you on the best forms of retirement income to conserve your super balance.

With the right superannuation investment strategies in place, you’ll be well prepared to weather the economic disruption brought about by COVID-19. It’s worth taking the time now to review and optimise each aspect of your super above to get the most from your investments.

Source: Money & Life