Tag Archives: Family

Investing an inheritance from $10,000 to $100,000 whatever your life stage

By Robert Wright /November 21,2025/

Receiving an inheritance may be a once in a lifetime financial opportunity that also coincides with a very difficult, emotional time in your life. Whether you inherit $10,000 or $100,000, your age, life stage, risk appetite and financial preparedness are likely to play a key role in decisions about how and where to invest.

Many Australians are likely to be left some form of inheritance, most likely from a parent, at some point in their life, with 81% of retirees currently expecting to leave wealth behind.

The average amount Australians expect to inherit is $184,000, according to research commissioned by Colonial First State*.

And while one in two Australians consider up to $10,000 a sizeable amount with which to start investing, the research shows the average amount most Australians consider to be a sizeable investment to own is more than $600,000.

Investing an inheritance may help close that gap. Following are some general thought starters to consider by age, life stage and size of inheritance but please consult a financial adviser for advice relevant to your personal situation.

Also consider your risk appetite. Generally, the more risk you’re willing to undertake, the higher the potential reward may be. However, higher returns come with a higher risk that the value of your investment may fall.

In general, if you only have a short time frame to invest, lower risk investments could be a safer option as they’re less likely to fluctuate in value.

What to do when you first receive an inheritance

The first thing to do when you first receive an inheritance, particularly if it comes at an unexpected time, is to consider your options.

That may mean putting it in a high interest savings account or a mortgage offset account while you decide what to do.

Then consider your goals. Do you need to pay off debt? Are you looking to build long-term wealth? Pay off your home loan? Build a diversified investment portfolio? Or invest for the kids?

Most people with a six figure amount to invest will consult a financial adviser, although it can also be cost effective to obtain one off financial advice for smaller amounts.

Inheriting assets like shares or property, such as the family home, can also have different capital gains tax implications if you decide to sell, so getting tax advice may also be important.

In your 20s

In your twenties, it may be helpful to pay off any high interest debt or build an emergency fund to cover three to six months of living expenses. Otherwise, the earlier you invest, the more time your money has to grow and compound.

$10,000 to invest:

- A growth oriented exchange traded fund (ETF) or managed fund may allow money to grow while offering flexibility to access it later if needed.

- A voluntary contribution to super, allocated to growth or high growth, can be a tax effective investment that compounds over the long term if you’re within the super contribution caps, or limits, although you generally can’t access it until you reach age 60 and have retired.

$100,000 to invest:

- Low touch investors might consider a diversified range of shares via set and forget growth ETFs and managed funds, such as a US shares themed ETF or a long-term growth managed fund.

- It may be worth consulting a financial adviser to start building a diversified growth portfolio of managed investments.

In your 30s

For many, the thirties are about getting into the housing market.

$10,000 to invest:

- A high interest term deposit or savings account that offers some growth may be a good option over a short time frame.

- A voluntary contribution to super may allow you to save for your deposit faster using the First Home Super Saver scheme. The tax rate is generally 15% on earnings in super, while the amount of your contributions you can release to buy your first home increases in line with the shortfall interest charge rate (currently 6.78%).

$100,000 to invest:

Starting a family or looking to enjoy a little extra income?

- Dividend focused ETFs may help generate a passive income stream.

- If property investing is more your thing, you may have enough to invest in a growing regional market or a real estate investment trust (REIT).

In your 40s

At this point, many Australians who have a mortgage are looking to reduce it.

$10,000 to invest:

- Those with a mortgage that’s more than 50% of the value of their home might consider paying it down or putting their inheritance in a mortgage offset account.

- If a mortgage is less than 50% of the value of the home, it may be worth considering shares as average share market returns most years can be higher than average mortgage interest rates – again, there are many low cost ETFs and managed funds available.

- Or consider making a one off voluntary concessional (pre tax) or non-concessional (after tax) contribution to your super and investing it in a long-term, high growth shares investment option, a gold or silver themed ETF or the growth focused managed fund of your choice.

$100,000 to invest:

- Thinking about paying for the kids’ education? Investment bonds can be a good option to include in the mix as withdrawals are tax free after 10 years.

- Some investors may consider debt recycling by paying down the mortgage and then applying for a new loan to buy an investment property. Interest on the new loan is generally tax deductible so those interest payments can be offset against your income to reduce the amount of tax you pay.

- For those who can afford to invest the money outright, it may be worth building a diversified portfolio of ETFs or managed funds. Global and local shares have historically offered among the best returns. We can connect you with a financial adviser if you’d like help to invest.

In your 50s

After the age of 50, it’s often a good time to maximise pre tax and after tax super contributions to harness some of those tax advantages.

$10,000 to invest:

- Have you reached your annual super contribution cap limits? You can contribute up to $30,000 a year in concessional contributions, which are generally taxed at the concessional rate of 15%. These include compulsory employer contributions and salary sacrifice, as well as voluntary personal contributions (which could include a tax free inheritance) for which you claim a tax deduction.

- Alternatives might include investing in income producing shares that usually pay a dividend, income or dividend ETFs or REITs.

$100,000 to invest:

- If you haven’t fully used your concessional contributions cap in any of the previous five financial years (and your total super balance was less than $500,000 at 30 June of the most recent financial year), you may be able to use those unused cap amounts to make additional catch up contributions over the standard concessional cap amount (currently $30,000).

- Non-concessional super contributions (up to $120,000 a year to a maximum super balance of $2 million) are not taxed on the way in and are an effective means of growing your super quickly. While you can’t claim a deduction against these contributions, they compound relatively quickly in the super environment. Depending on how much you have contributed in prior years, you may be eligible to contribute up to $360,000.

- Investors who are likely to need to draw on their investments in the next few years, might consider including some fixed income securities or managed volatility funds alongside higher risk investments, such as shares.

In your 60s

Many people approaching retirement focus on preserving capital against sudden falls in value but there are also real costs in going too conservative too early.

From age 60, you can also access super if you meet a condition of release, such as retiring from a job. You can access your super regardless from age 65.

$10,000 to invest:

- It may be helpful to pay down any remaining debt or top up super.

$100,000 to invest:

- After 60, be cautious with gifting, as it may affect your eligibility to receive the government’s Age Pension from age 67. Gifts over $10,000 per year or $30,000 over five years will still be counted among your assets when it comes to Centrelink means-testing.

- For those who have reached their super contribution cap limits, it may be worth topping up your spouse’s super.

In your 70s and beyond

Enjoy your retirement. Most investors are focused on capital preservation and income generation and it may be worth using the bucket strategy with the goal of making your money last longer. At the same time, don’t forget to tick off the things on your bucket list.

$10,000 to invest:

- Keep some money in cash or term deposits for accessibility.

$100,000 to invest:

- A mix of fixed income investments, REITs and conservative managed funds may help reduce risk, alongside higher growth shares or managed funds that you don’t expect to access in the next five years.

Whether you inherit a modest sum or a substantial windfall, align your investment strategy with your life stage, goals and risk tolerance.

For smaller amounts, many Australians manage without advice but for larger inheritances, professional advice from a financial adviser and an accountant can help you navigate tax implications, diversify your investments and plan effectively for the future.

* Colonial First State research conducted with 2,250 Australians online between January and June 2025.

Source: Colonial First State

Australian household wealth

By Robert Wright /February 16,2024/

Is high Australian household wealth a source of support for consumers?

Key points

- Australia ranked as having one of the lowest rates of disposable income growth per capita amongst OECD countries in mid 2023.

- An increasing income tax burden and mortgage repayments have weighed on income growth, despite solid wages and salaries.

- But, household balance sheets in Australia look stronger compared to incomes. Household wealth increased in 2023, as home prices rose.

- However, growth in household wealth will decline in 2024 as home prices are expected to fall. Household incomes will also be under pressure as earnings growth slows from a softening labour market.

- As a result, high household wealth holdings will not be enough to offset a challenging environment for households in 2024, despite some easing in cost of living challenges.

Introduction

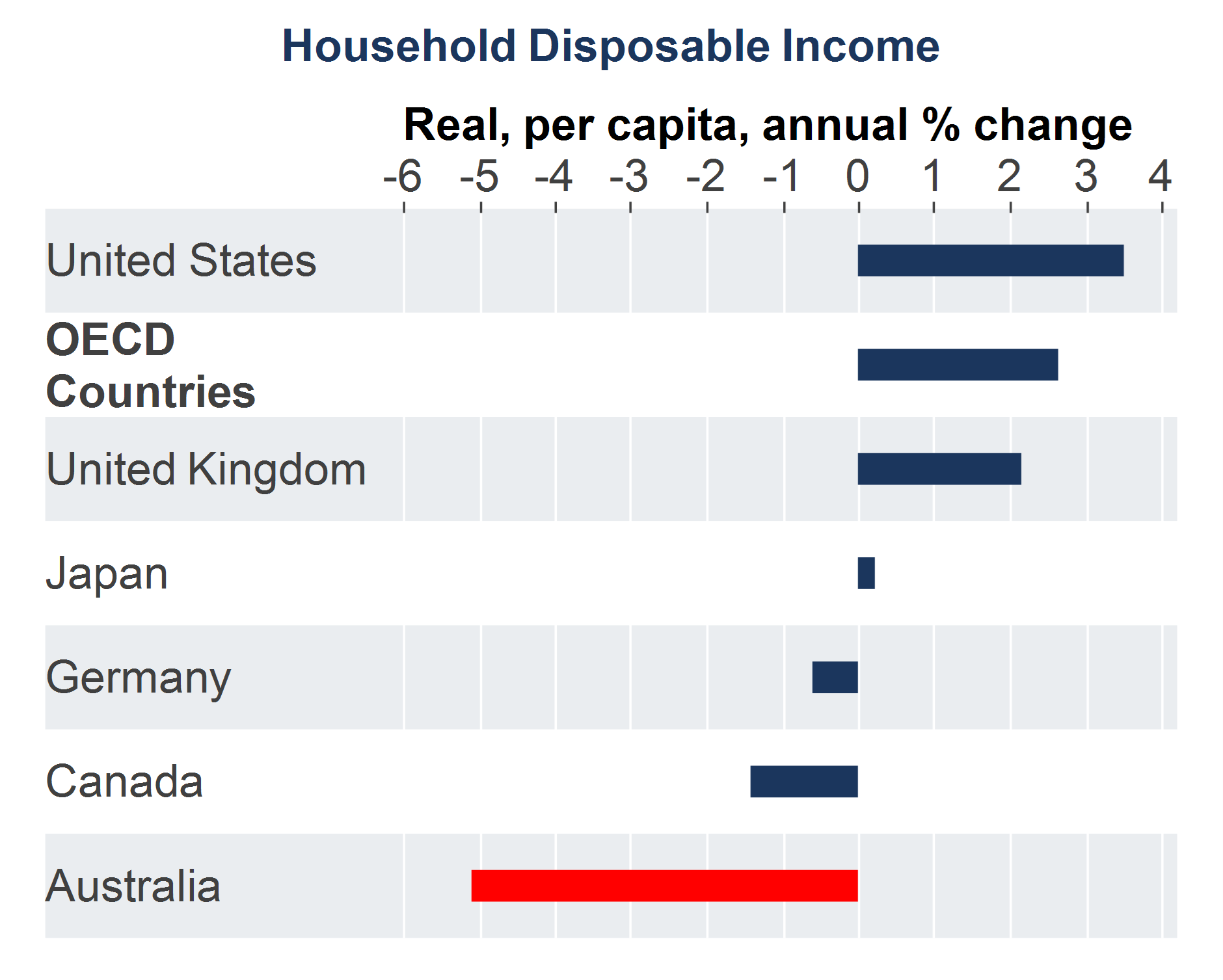

Household income data from the OECD showed that Australia had one of the lowest rates of annual real household disposable income per person compared to its OECD peers (see the chart below). Over the year to June 2023, Australia’s real per capita household disposable income was down by 5.1%, compared to a 2.6% rise across OECD countries.

Source: AMP, Macrobond

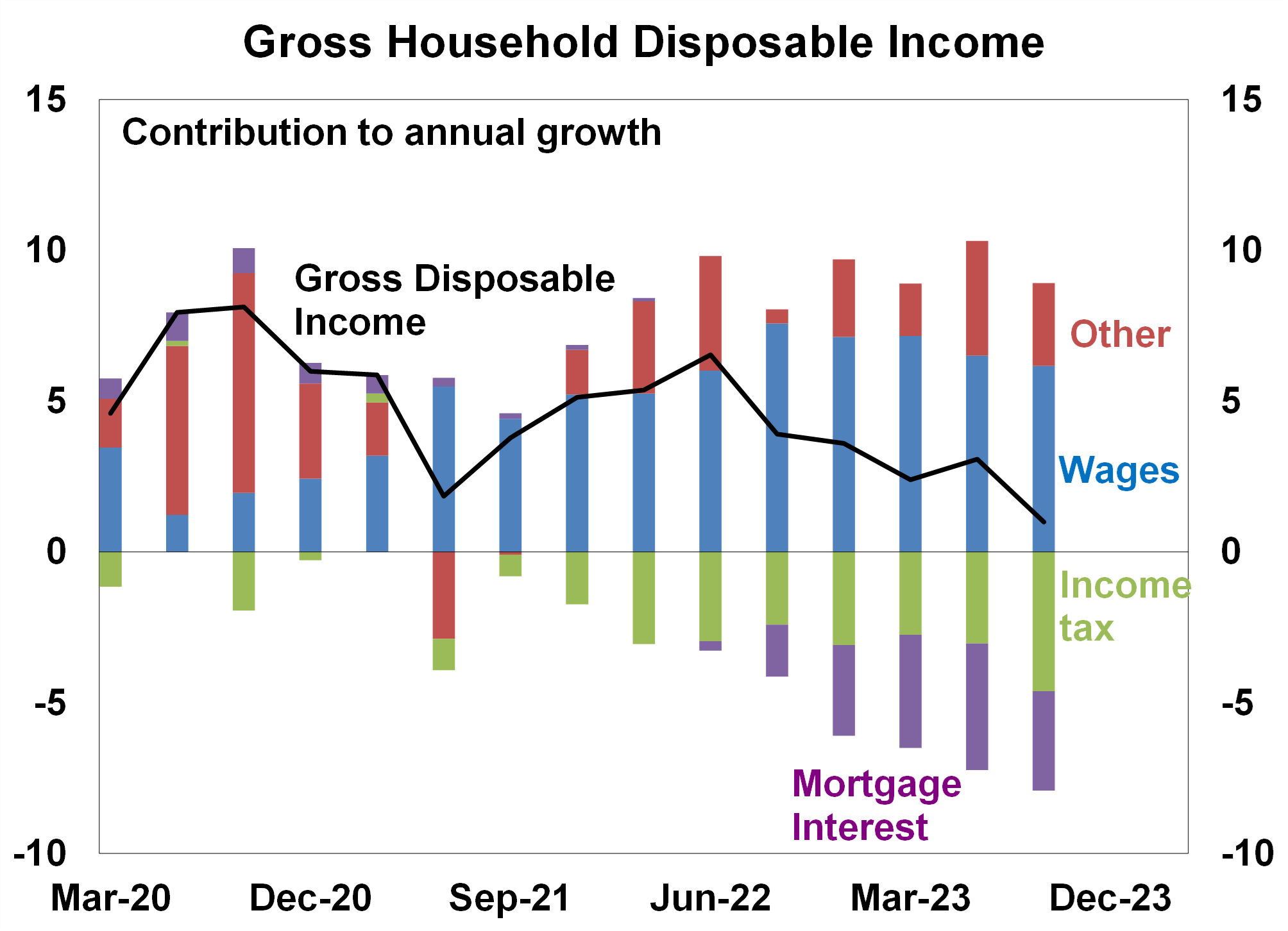

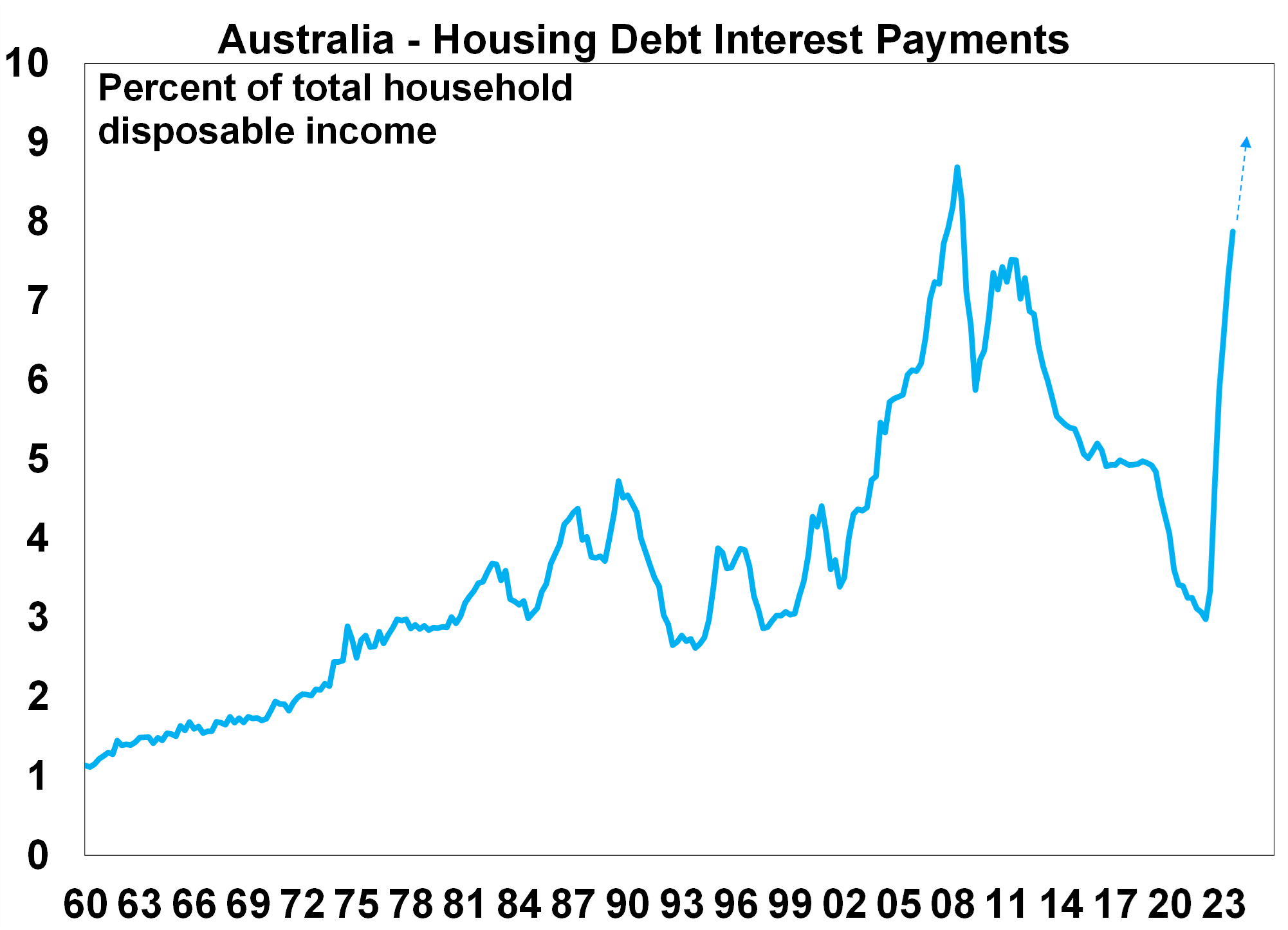

This occurred despite very healthy labour market conditions in Australia which saw employment growth running above 3.0% per annum all year, the unemployment rate remaining below 3.9% and underemployment continuing to be low, all of which boosted wages growth. Despite this positive earnings backdrop, the income tax burden increased in 2023 as households have been moving into higher income tax brackets (otherwise known as “bracket creep”), as well as the end of income tax concessions. Mortgage interest repayments are also an increasing drag on incomes (see the chart below) as the cash rate has been increased by 425 basis points since May 2022. Australia’s very high population growth in 2023 (running at 2.4% over the year to June 2023) also masked a fall in household disposable income growth per person, relative to other OECD countries.

Source: ABS, AMP

Just looking at household income accounts does not show everything about the position of households. In a country like Australia where home ownership rates are high (66% of Australian households own their home, with or without a mortgage), looking at household wealth is also important.

Household wealth in Australia

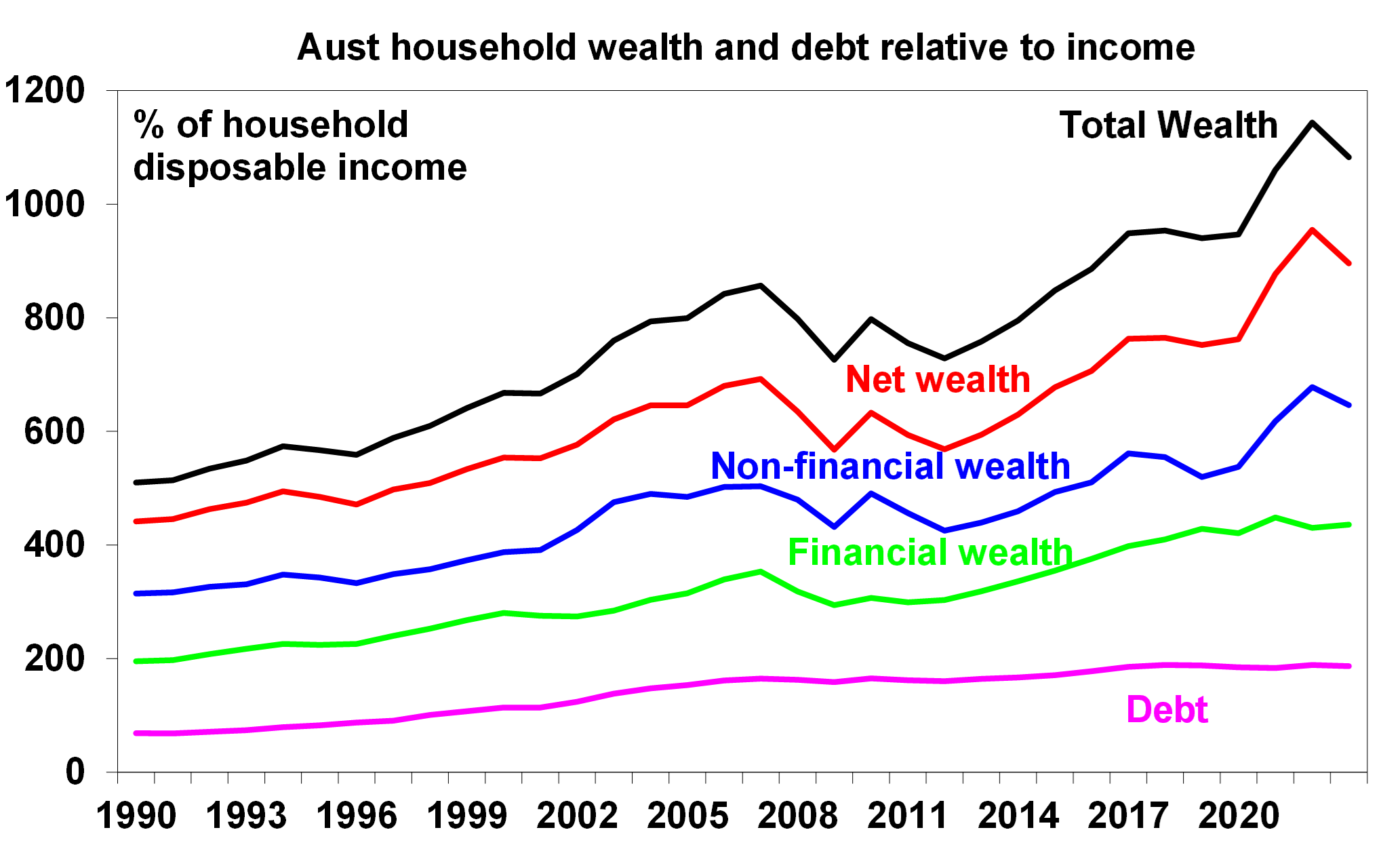

The Australian Bureau of Statistics estimates the value of a household’s assets, liabilities and therefore wealth. Net worth or wealth is calculated as a household’s total assets minus its liabilities. Total wealth is close to 11 times the size of household disposable income (or 1083%) and net wealth is 896% of income. The latest data for the year to June 2023 showed a slight fall in wealth as a share of income, after it reached a record high in 2022 – see the chart below. Non financial wealth is worth 647% of income, larger than financial wealth at 436% and well surpassing household debt, which is 187% of income.

Source: RBA, AMP

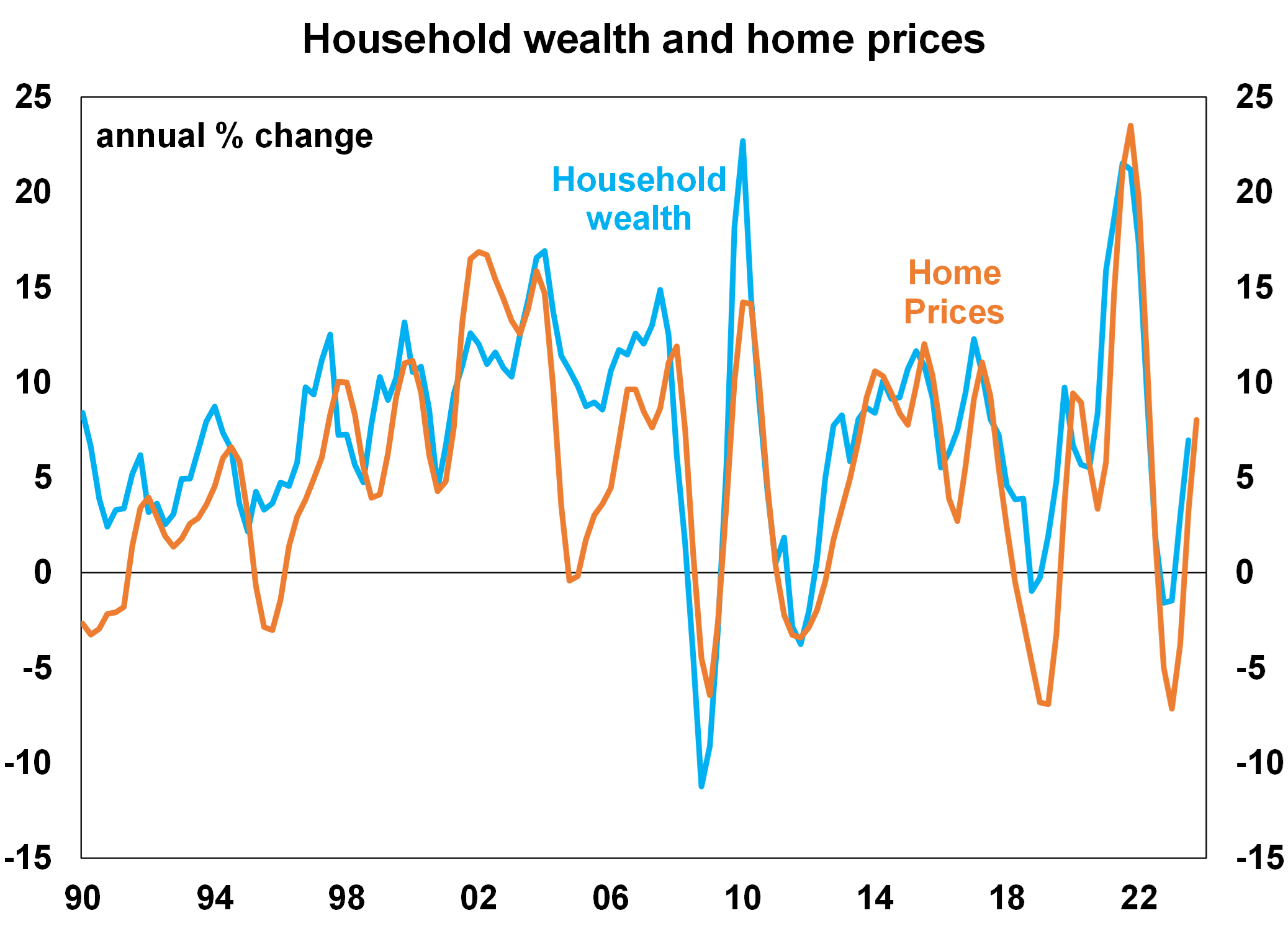

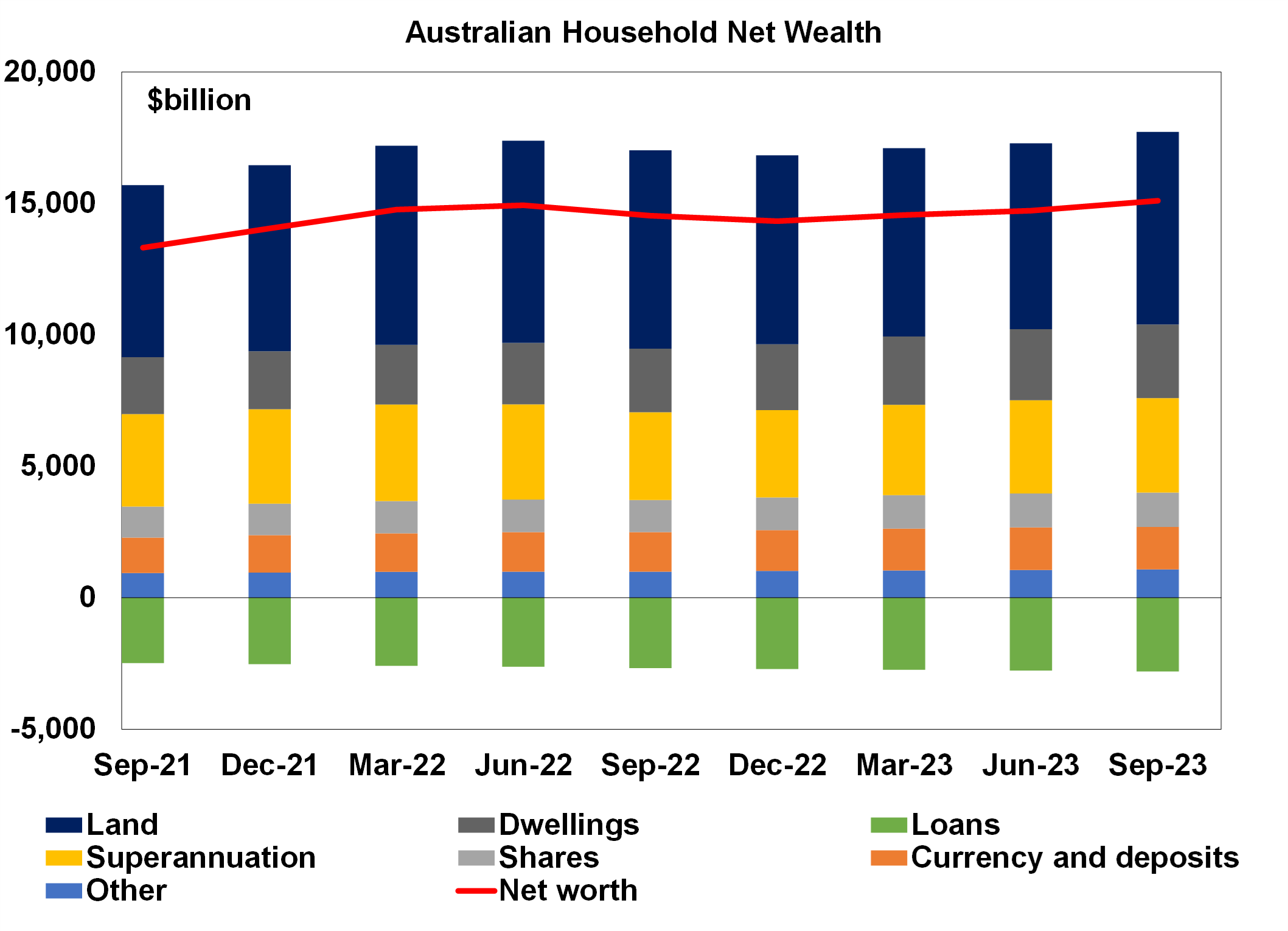

Around 70% of Australian household wealth is tied to the value of homes (which is made up of land and dwellings) and moves closely in line with home prices (see the chart below). Household wealth rose throughout 2023, in line with solid growth in home prices.

Source: ABS, AMP

Other components of household wealth are shown in the chart below. Assets include superannuation, shares and currency and deposits. Loans which are mostly for housing are the source of household liabilities.

Source: ABS, AMP

How does household wealth compare around the world?

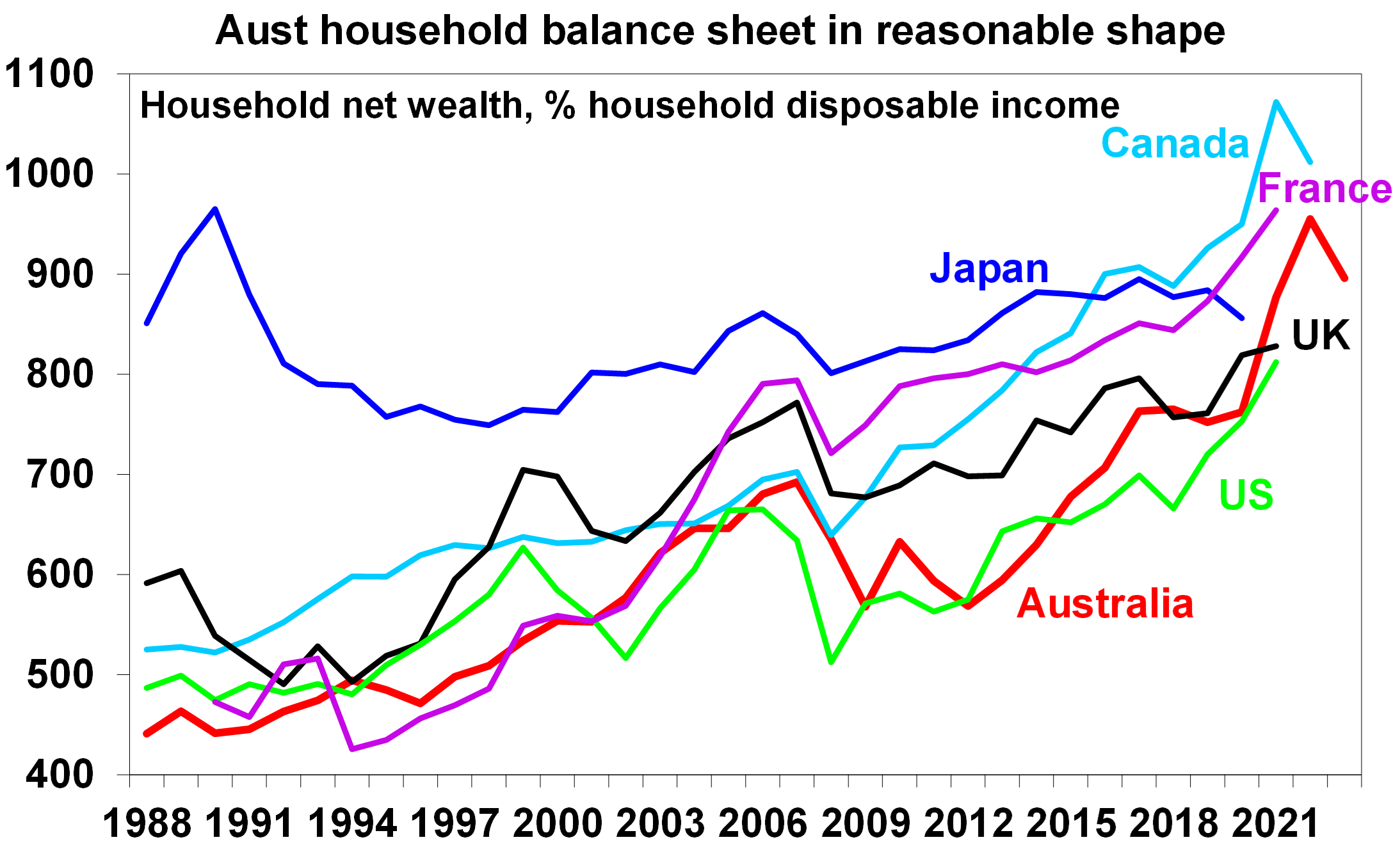

Australian household wealth, as a share of household disposable income, is at the top end of its OECD peers (see the chart below).

Source: OECD, AMP

High holdings of wealth could be considered a source of support for households, especially against record levels of household debt in Australia. This is a concept known as the “wealth effect”. When household wealth increases, households feel more secure with their financial position and household savings tend to decrease which lifts consumer spending. When wealth decreases, households feel less secure which leads to an increase in savings and decline in spending. However, this relationship does not always work. Most recently in the pandemic, household wealth rose in 2021/22 alongside the lift in home prices but the savings ratio also surged thanks to government driven stimulus cheques. Since then, the household savings ratio has been falling but growth in total consumer spending has been low. We expect that the household savings rate will continue to fall in 2024 as it normalises after the pandemic but growth in consumer spending will still be low.

Implications for investors

Households dealt with a cost of living challenge in 2023 because of high inflation and rising interest rates. Inflation is expected to slow in 2024 and we expect the RBA to start cutting interest rates by mid year which should ease the repayment burden for households with a mortgage, as mortgage interest repayments as a share of income are rising to a record high (see the chart below).

Source: ABS, AMP

So, while cost of living issues should improve for consumers, household wealth will come under pressure in 2024 as we expect home prices will decline by 3.0% to 5%. This is likely to occur alongside a slowing in household incomes as the labour market weakens and the unemployment rate increases. This environment is expected to be negative for consumer spending and GDP growth. We see GDP growth rising by 1.2% over the year to June 2024, below the RBA’s forecast of 1.8% and anticipate the unemployment rate to increase to 4.5% by mid year. This should see the RBA cutting interest rates by June and we expect a total of 3 rate cuts in 2024.

Wealth inequality between households is also an issue in Australia. The top 20% of households (by income quintile) owned 63% of total household wealth in 2019-20 but the bottom income quintile (the bottom 20%) owned less than 1.0% of all household wealth. In Australia, there is also increasing generational wealth gap, with wealth across older households increasing significantly over recent decades but this has not been the case for younger Australians. There are numerous government policies that could address these issues of wealth inequality, including improving the housing affordability issue (through lifting housing supply and/or looking at the favourable treatment of housing investment) and doing a tax review (looking at broadening the GST and examining the merits of a wealth or death tax), which could help the wealth inequality issue.

Source: AMP

Some recent questions on Australian inflation

By Robert Wright /August 21,2023/

Key points

- The Australian inflation rate peaked in the December quarter but has been slower to decline than some global peers. While interest rate rises are helping to reduce inflation (especially as discretionary consumer spending slows), rises in domestic energy prices, a tight rental market and a lagged pick up in wages have contributed to higher than expected inflation outcomes.

- The main policy available in the RBA’s toolkit to manage inflation is interest rates, which is a blunt tool because of its unequal impact on households with debt.

- The burden of interest rate increases falls on households with mortgage debt. Businesses and investors are also impacted but the deductibility of interest provides some offset.

- Some countries in Europe have opted to use price controls for essential items to reduce inflation, with mixed results. Price controls tend to add distortions to the market and rent controls are not helpful while housing supply is limited (like in Australia).

- But the government still has a role to play in helping the RBA achieve its 2-3% inflation target through keeping fiscal policy neutral/contractionary if inflation is high, ensuring a well functioning energy market, maintaining sustainable wage increases, regulating businesses to discourage price gouging and monopolistic behaviour and calibrating appropriate migration targets to match housing supply.

Introduction

Australian inflation is very high. Consumer prices were up by 7% over the year to March, around a 33-year high but this was a decline from a cyclical peak of 7.8% in December 2022. The Reserve Bank of Australia (RBA) has been focusing on reducing inflation through the main policy tool available in the central bank’s toolkit – interest rates. The cash rate has risen from 0.1% in April 2022 to 4.1% in June – a 4% lift in just over a year. But, the impact on inflation so far has been lower than expected. As a result, we are often asked whether interest rates are actually having an impact on inflation or whether there are better tools available to policymakers, especially as interest rate hikes are having an unequal impact across household groups. We go through some of these issues in this article.

Are interest rate hikes working to reduce inflation?

Interest rate hikes have led to a slowing in consumer demand which is helping to reduce inflation. Discretionary spending fell in the March quarter and the volumes of retail spending was negative over the December-March quarter. Without the lift in interest rates, inflation may have increased further and consumer and market-based medium-long term inflation expectations could have kept rising well above the RBA’s 2-3% inflation target.

Some might say that rate hikes should have worked faster or better by now to reduce inflation. The problem has been that there have been numerous supply driven elements of the inflation story that have been less sensitive to interest rate changes. COVID driven supply chain disruptions led to big increases in shipping costs, commodity prices like energy, metals and agriculture increased significantly in 2021-22 (mostly from supply disruptions), domestic energy supply issues led to an Australian energy crisis and multiple domestic floods led to higher food prices. While these issues may not be directly influenced by the level of change in interest rates, it is the responsibility of the RBA to ensure that supply driven price changes do not leak into consumer prices. A lot of these supply related issues are now resolved but it takes time for it to be reflected in the final inflation figures.

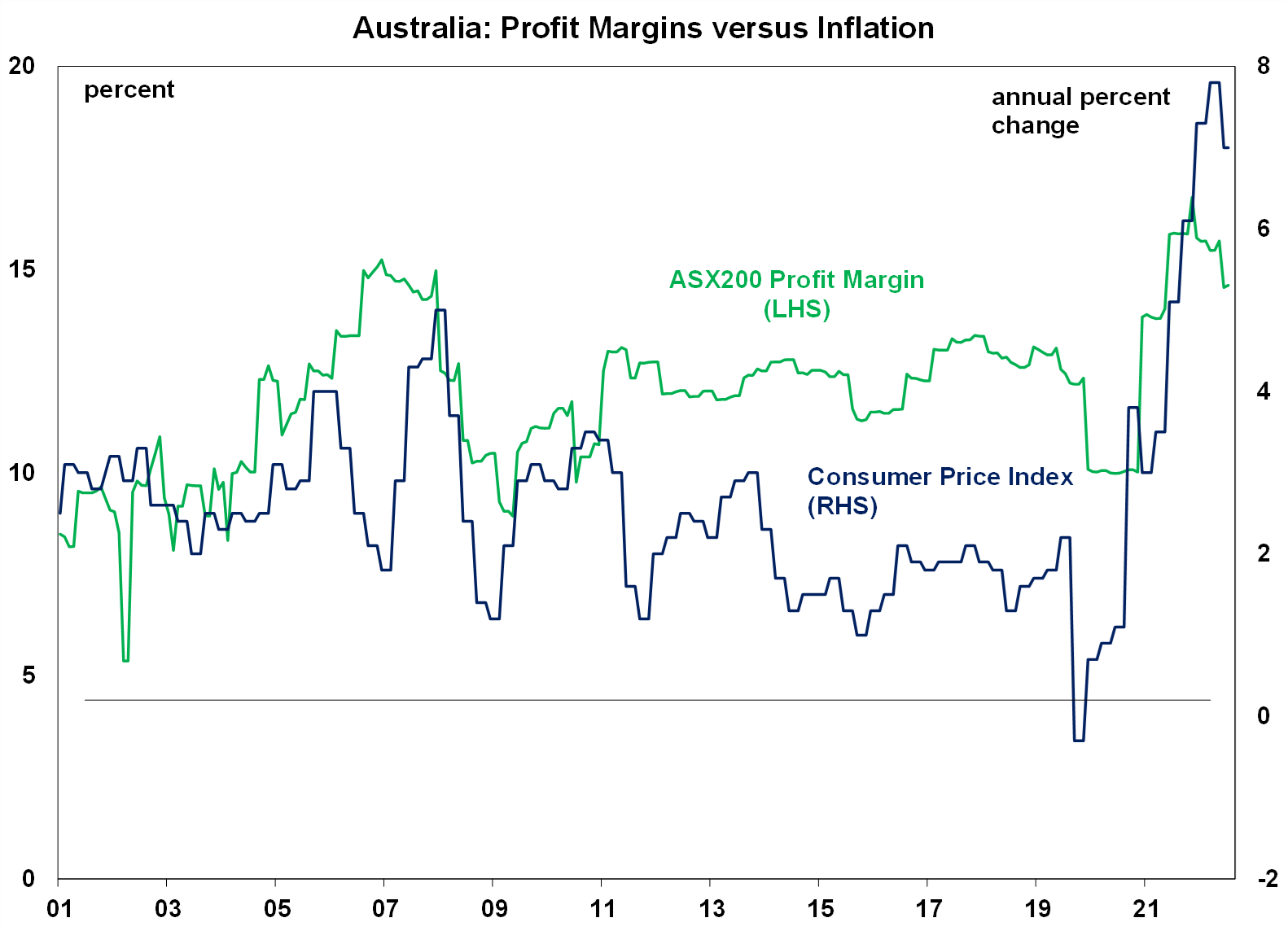

Evidence of excessive price gouging by businesses is not obvious. Profit margins have expanded (increasing from 10% in 2020 to a recent high of ~16%) but have generally moved in proportion to the rise in inflation (see the chart below) and are now declining. The profit share (ex mining) of GDP has also been fairly stable. And slowing consumer discretionary spending means that continued profit margin expansion will be unlikely.

Source: Bloomberg, AMP

The peak of Australian inflation (in December 2022) also occurred later compared to some global peers which means that the slowing in inflation appears like it’s taking longer. US inflation peaked at 9.1% in June 2022 and in the Eurozone at 10.6% in October 2022 (see the next chart).

Source: Macrobond, AMP

Australia’s energy crisis occurred later relative to the Northern hemisphere, because of a raft of our own domestic issues like supply challenges with coal, a poor national plan for the energy transition and higher global prices. This meant that both the US and Europe were more impacted by an energy price surge in early 2022 from the war in Ukraine and the winter weather. Australia’s rental market also tightened significantly over the past year as net migration rebounded to record highs after the pandemic, pushing vacancy rates to ultra low levels in the capital cities and lifted rents, although recent vacancy rates across the capital cities have ticked up and newly advertised rental growth is slowing. Australia’s wage setting system also seems to have more “inertia”, with the minimum wage decision occurring once a year and many other wages like awards also based off this annual decision or driven by changes to headline inflation, which only peaked in December 2022.

While these factors all suggest that inflation in Australia could remain higher for longer for now, the good news is that our Pipeline Inflation Indicator still suggests significant downside to Australian inflation over the next six months and we expect headline consumer prices to be at the top end of the RBA’s target band by early 2024 (on a 6-month annualised basis).

Source: Bloomberg, AMP

Are interest rate hikes increasing inequality?

The impact of monetary policy works primarily through the lending channel because borrowing rates are priced off the cash rate. Households with a mortgage are the most impacted by interest rate changes. Businesses and individual investors are arguably less impacted because they can deduct the debt interest expenses. There are also other financial market channels that monetary policy works through, mostly through the exchange rate.

The high level of household debt now means that mortgage holders will bear the brunt of monetary policy changes. Renters can also be affected from higher interest rates if landlords are able to pass on the higher cost of debt servicing through higher rents. This is only usually an option in a tight rental market (which the current situation is allowing for).

In Australia, 37% of households have a mortgage (using data from 2019-20), 29% rent and 30% own their own outright. Detailed ABS data on housing costs shows that households with a mortgage spend close to 16% of their gross household income on “housing costs” (mortgage or rent and rate payments) as at 2019-20, owners without a mortgage spend 3% of their income on housing costs and the average renter spends close to 20% of their income on housing. And there are divergences across income quintiles (see the chart below) with the lowest income quintiles spending a very large share of income on housing costs.

Source: Bloomberg, AMP

Are there other options to combat high inflation?

The high degree of supply related factors that have increased inflation, the slow reduction in prices despite aggressive interest rate hikes and the high burden placed on households with a mortgage has led to questions about whether there are other options available to reduce the level of inflation.

The RBA has been tasked with the responsibility for the 2-3% inflation target but the only tool at its disposal is monetary policy. While the range of options within the toolkit has expanded beyond interest rates (including yield targets and quantitative easing) all of these measures ultimately influence the money supply and therefore the cost of borrowing.

The government has more tools at its disposal compared to the RBA through its spending and taxation decisions as well as regulation. However, these tools are slow moving and do not have as much of a direct impact on inflation. Some have argued that price controls need to be considered in Australia. Food price caps have recently been tried in Europe for some essential items, including in France, Croatia and Hungary with mixed impacts as measured inflation went down but there were reports of some food shortages.

Usually, economists do not advocate for price controls or caps because it’s a distortion in the market and leads to problems like supply shortages. However, the Federal government did impose energy price caps domestically, so it is already being utilised in some capacity. Talk of rent controls would likely add to supply constraints across Australia at a time when housing supply needs to lift.

But, the government does have a role to play in many components that impact inflation, such as by ensuring a well regulated electricity market, sustainable outcomes for minimum award and public sector wages which set the tone for the rest of the market, ensuring that fiscal policy (both state and federal) is appropriate for the state of the economy (we think the impact of the May Federal budget is more or less neutral but with the addition of some state cost of living benefits it could be marginally inflationary and the government could consider raising taxes to help get inflation down), regulation of retailers to ensure adequate competition and ensuring adequate housing for the migration targets.

Implications for investors

For investors, the good news is that inflation is expected to decline through the rest of the year which should mean that central banks are close to the top of their tightening cycles. This is generally positive for sharemarkets however, the further interest rates increase, the higher the risk of recession which is a risk for sharemarkets. The RBA’s recent hawkish stance means that further increases to the cash rate are likely in Australia. We expect another two interest rate increases from here, taking the cash rate to 4.6% which risks a recession in the next 12 months because of the heightened sensitivity of households to interest rate hikes in Australia.

Source: AMP

Expanding SMSFs for the expanding family?

By Robert Wright /May 19,2023/

It has finally happened. Recommended by the Cooper Super System review in 2010, put forward in the Federal Budget four years ago by then Treasurer Scott Morrison and finally passed on 17 June 2021, the maximum amount of members allowed in a Self Managed Super Fund (SMSF) has expanded from four to six.

Despite the previous maximum of four members, the vast majority of SMSFs had only one or two members therefore this increase did not exactly stop the press. Yet the question remains, why would an SMSF want six members and what are the disadvantages?

The most logical reason for a fund to grow to six members is to gather a larger pool of assets to invest. A larger amount to invest could open up residential and commercial property investment, or other nonstandard assets that require a large capital outlay, such as fishing licenses or marina berths.

Greater diversification for what many would consider standard assets, such as shares and managed funds, could be better achieved with six members.

Additionally, if the SMSF is paying fixed accounting and administration costs, having six members would also result in a lower cost per member.

If a large family is running two funds currently due to the previous four member limit, the funds can now be consolidated. However, it would be a capital gains tax event for the fund that is being closed down. Therefore consideration should be given to the unrealised tax position for each fund when deciding which to keep and which to close.

The main disadvantage of a six member fund is just that, the six members. The larger the fund, the greater number of people who are involved in the decision making process and the greater number of people who have to agree. With a greater number of members there is also the greater likelihood that there will be a falling out or there will be a marriage breakdown that could result in the division of superannuation. This would be particularly detrimental if the six member fund was established to invest in one large illiquid asset.

The chances of one of these unfortunate events occurring magnifies with each additional member, so it goes without saying that six member funds and the accountants and advisers that assist them will see their fair share of grief and the financial consequences that result.

For current SMSF trustees who are considering taking advantage of this legislation change, a review of the trust deed should be completed and a corporate trustee should be appointed if one is not already in place.

The SMSF member limit increase to six is good. It provides more choice in a superannuation environment which is known for restrictions and adverse government legislation changes. Opening up self managed superannuation funds to six members does increase additional investment opportunities, however serious consideration should be given to potential ramifications prior to proceeding down this path.

If you would like to discuss establishing an SMSF with six members, or adding members to an existing SMSF, please contact your financial adviser.

Source: Bell Potter