Tag Archives: Financial Habits

Decoding cognitive biases: what every investor needs to be aware of

By Robert Wright /August 23,2024/

Common human biases that investors should understand when it comes to investing is extremely important. These biases are ingrained in human nature, leading to tendencies to oversimplify, rely on quick thinking or exhibit excessive confidence in judgments, which may lead to investment mistakes. By gaining insight into these biases, investors may be able to make better decisions to help reduce risk and improve their investment outcomes in the long-term.

Numerous cognitive biases can affect how decisions are made. The key to mitigating these biases lies in recognising their presence, identifying when they might arise and then either making appropriate adjustments or obtaining help to moderate their impact.

Seven cognitive biases that might arise at various stages of an investor’s investing journey.

- Herding: The tendency to follow and mimic the actions of a larger group.

- Confirmation bias: The preference for information that confirms one’s existing beliefs or hypotheses.

- Overconfidence effect: Excessive confidence in one’s own investment decisions and abilities.

- Loss aversion: When the fear of loss is felt more intensely than the elation of gains.

- Endowment effect: Overvaluing assets because they are owned.

- Neglect of probability: Disregarding the actual likelihood of events and often overemphasising rare occurrences at the expense of more probable outcomes.

- Anchoring bias: The tendency to rely too heavily on a past reference or a single piece of information when making decisions.

Herding

The herd mentality occurs when people find reassurance and comfort in a concept that is widely adopted or believed by many others. In recent times, we have seen the herd mentality with the events that surrounded the GameStop stock event. Where many people saw the rise in stock prices and without proper investment research followed the trend of many others and invested.

This impacted a lot of investors who bought the stock due to the fear of missing out and the hype it created. We believe, to be a successful investor, you must be able to analyse and think independently. Speculative bubbles are typically the result of herd mentality. Herd mentality in investing can overshadow rational decision making and could increase the risk of financial losses.

Investors need to recognise the feeling of pressure to conform to popular opinion or follow the crowd and instead consider conducting research and analysis before making decisions, as well as seeking alternative views to challenge the consensus.

Confirmation bias

Confirmation bias is the tendency to favour information that corroborates pre-existing beliefs or theories. In our view, confirmation bias can lead to significant errors in investing. Investors may develop an inflated sense of certainty when they encounter consistent evidence supporting their choices. This overconfidence can create an illusion of infallibility, with an expectation that nothing can go wrong.

Overconfidence bias

Overconfidence bias in investing is where investors overestimate their knowledge, intuition and predictive capabilities, often leading to poor financial decisions. This bias can present itself through various ways such as excessive trading, under-diversification and the general disregard for potential risks.

Investors with overconfidence bias tend to believe they can time the market or have the ability to pick the winning stocks better than most, which in turn may also result in overtrading and increased transaction costs. Overconfidence can also lead to a lack of proper risk assessment and analysis, as investors might underestimate the likelihood of negative events or industry dynamics affecting their investments.

An example of overconfidence bias occurred during the dot-com bubble of the late 1990s and early 2000s. Many investors were overly optimistic about the growth potential of internet related companies. This led to inflated stock prices as more and more people invested in these companies without proper evaluation of their actual worth.

Loss aversion

Loss aversion is where a real or potential loss is perceived as much more severe than an equivalent gain. The pain of losing is often far greater than the joy in gaining the same amount.

This overwhelming fear of loss can cause investors to behave irrationally and make bad decisions, such as holding onto a stock for too long or too little time. For example, an investor whose stock begins to tumble, despite clear signs that recovery is unlikely, may be unable to bring themselves to sell due to the fear of loss in the portfolio. On the flip side, when a stock in the portfolio surges, they may quickly cash out, not wanting to see the possibility of those profits disappearing.

When an investor clings onto failing stocks, departs with successful stocks too quicky and fear governs their investment decision, it’s known as the disposition effect. It’s a direct consequence of loss aversion, leading investors to make overly cautious choices that ultimately undermine their financial goals.

So, understanding this bias may help investors make rational decisions to grow their portfolios while managing risk effectively.

Endowment effect

Closely related to the concept of loss aversion is the endowment effect. This effect arises when individuals place a greater value to items because they own them, as opposed to identical items that they do not own. It’s a cognitive bias where ownership elevates the perceived value of an item beyond its objective market value.

For example, an investor may develop a strong attachment to a particular stock. It could be the very first stock they ever invested in, or they may favour the company for a particular personal reason such as aligning with their values. If this stock begins to fall and financial experts are advising to sell, because of the value bias this investor has they may be unwilling to sell. The investor perceives the stock’s value as greater than what the market dictates, purely because of ownership. It is a delicate balance that is needed to be able to determine between attachment and sound financial decision making and can be challenging for some investors.

To help mitigate the endowment effect, investors should regularly review their portfolios and consider the help of a financial adviser. Establish clear, predefined criteria for selling assets, aligned with financial goals. Develop a detailed investment plan with specific financial goals, a well defined investment strategy is crucial to prevent emotional decision making. Understanding and focusing on long-term investment goals can also help in maintaining objectivity.

Neglect of probability

Humans often overlook or misjudge probabilities when making decisions, including investment decisions. Instead of considering a range of possible outcomes, many people tend to simplify and focus on a single estimate. However, the reality is that any outcome an investor anticipates may just be their best guess or most likely scenario. Around this expected outcome, there’s a range of potential results, represented by a distribution curve.

This curve can vary widely depending on the specific characteristics of the business involved. For instance, companies which are well established and have strong competitive positions, tend to have a narrower range of potential outcomes compared to less mature or more volatile companies, which are more susceptible to economic cycles or competitive pressures.

Another error investors may make is to overestimate or misprice the risk of very low probability events. That does not mean that ‘black swan’ events cannot happen but that overcompensating for very low probability events can be costly for investors.

Anchoring bias

Anchoring bias is the inclination to excessively rely on a previous reference or a single piece of information when making decisions. Numerous academic studies have explored the impact of anchoring on decision making. Typically, these studies prompt individuals to fixate on a completely random number (such as their birth year or age) before asking them to assign a value to something. The findings consistently demonstrate that people’s responses are influenced by the random number they focused on prior to being asked the question.

Looking at a recent share price is a common way investors may anchor their decisions. Some people even use a method called technical analysis, which looks at past price movements to predict future ones. However, just because a stock’s price was high or low in the past doesn’t tell us if it’s a good deal now.

Source: Magellan

Australian household wealth

By Robert Wright /February 16,2024/

Is high Australian household wealth a source of support for consumers?

Key points

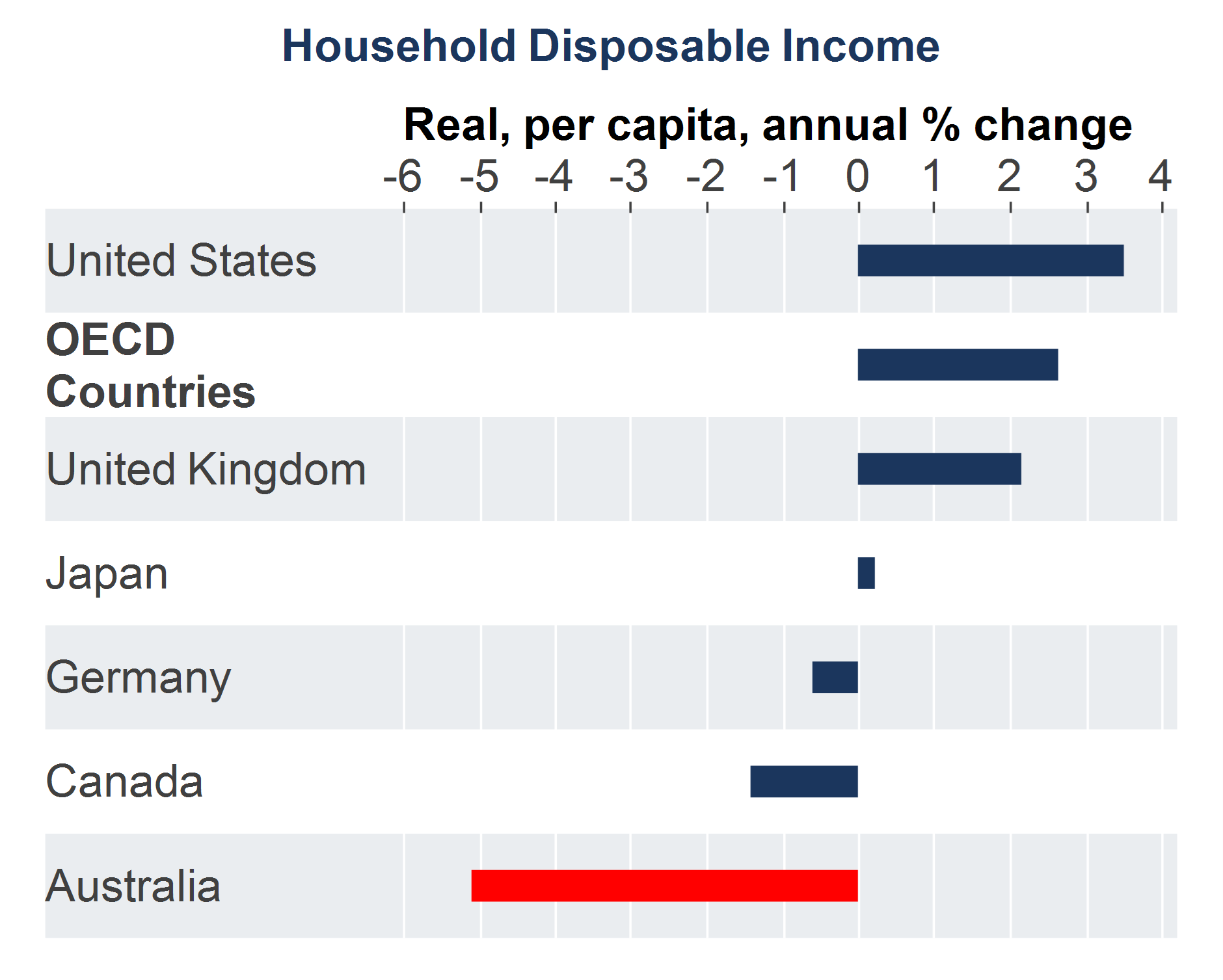

- Australia ranked as having one of the lowest rates of disposable income growth per capita amongst OECD countries in mid 2023.

- An increasing income tax burden and mortgage repayments have weighed on income growth, despite solid wages and salaries.

- But, household balance sheets in Australia look stronger compared to incomes. Household wealth increased in 2023, as home prices rose.

- However, growth in household wealth will decline in 2024 as home prices are expected to fall. Household incomes will also be under pressure as earnings growth slows from a softening labour market.

- As a result, high household wealth holdings will not be enough to offset a challenging environment for households in 2024, despite some easing in cost of living challenges.

Introduction

Household income data from the OECD showed that Australia had one of the lowest rates of annual real household disposable income per person compared to its OECD peers (see the chart below). Over the year to June 2023, Australia’s real per capita household disposable income was down by 5.1%, compared to a 2.6% rise across OECD countries.

Source: AMP, Macrobond

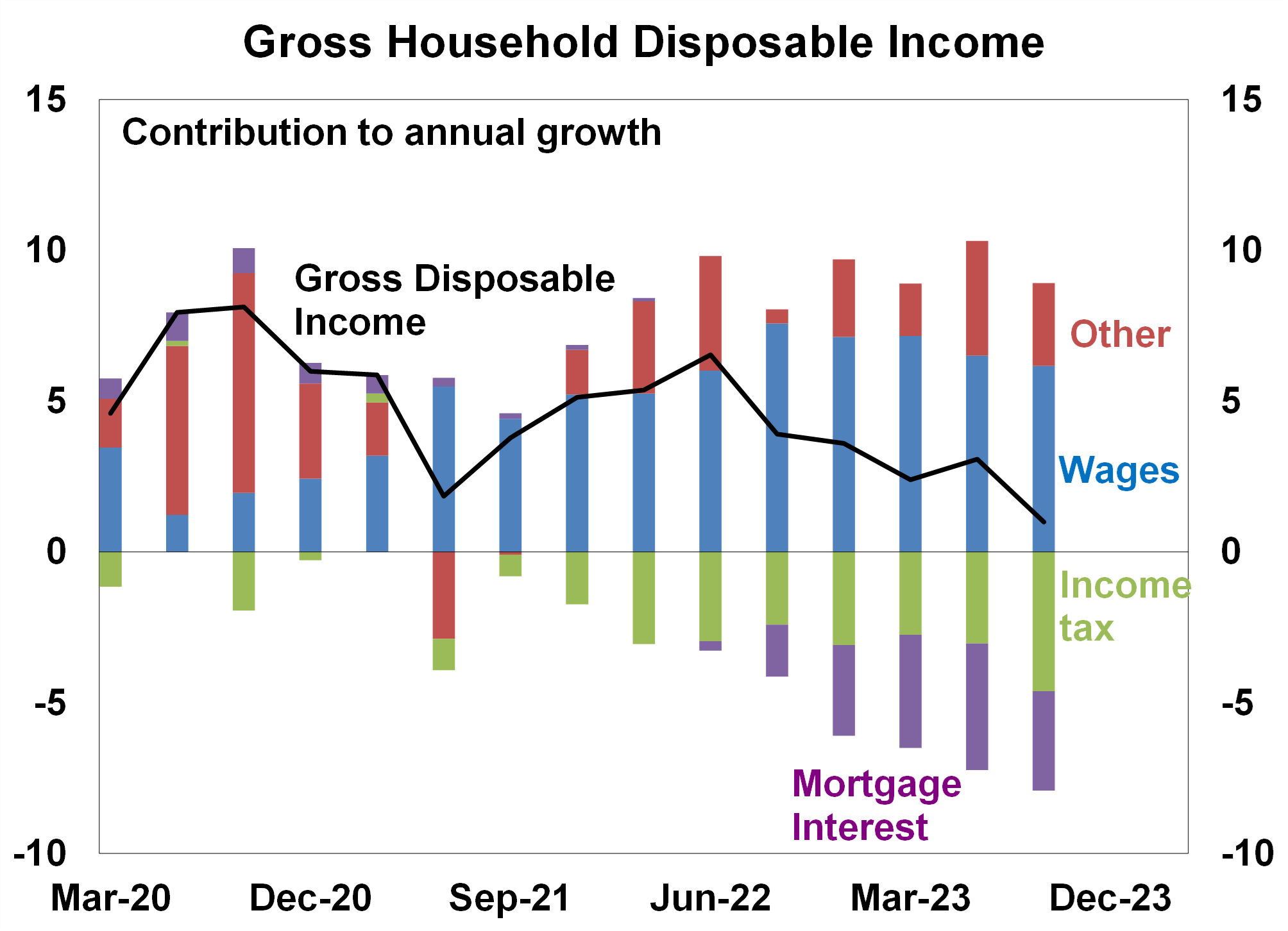

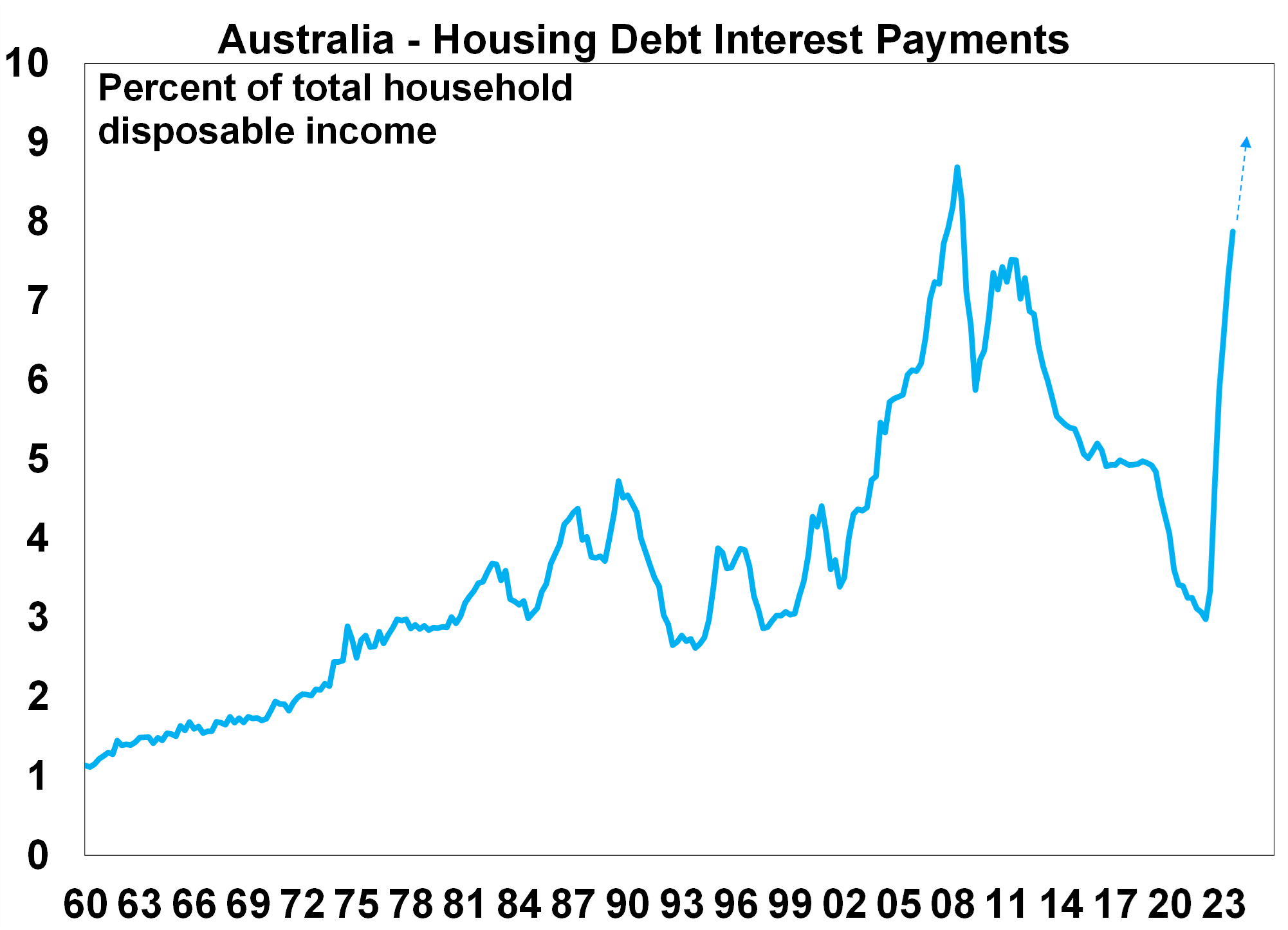

This occurred despite very healthy labour market conditions in Australia which saw employment growth running above 3.0% per annum all year, the unemployment rate remaining below 3.9% and underemployment continuing to be low, all of which boosted wages growth. Despite this positive earnings backdrop, the income tax burden increased in 2023 as households have been moving into higher income tax brackets (otherwise known as “bracket creep”), as well as the end of income tax concessions. Mortgage interest repayments are also an increasing drag on incomes (see the chart below) as the cash rate has been increased by 425 basis points since May 2022. Australia’s very high population growth in 2023 (running at 2.4% over the year to June 2023) also masked a fall in household disposable income growth per person, relative to other OECD countries.

Source: ABS, AMP

Just looking at household income accounts does not show everything about the position of households. In a country like Australia where home ownership rates are high (66% of Australian households own their home, with or without a mortgage), looking at household wealth is also important.

Household wealth in Australia

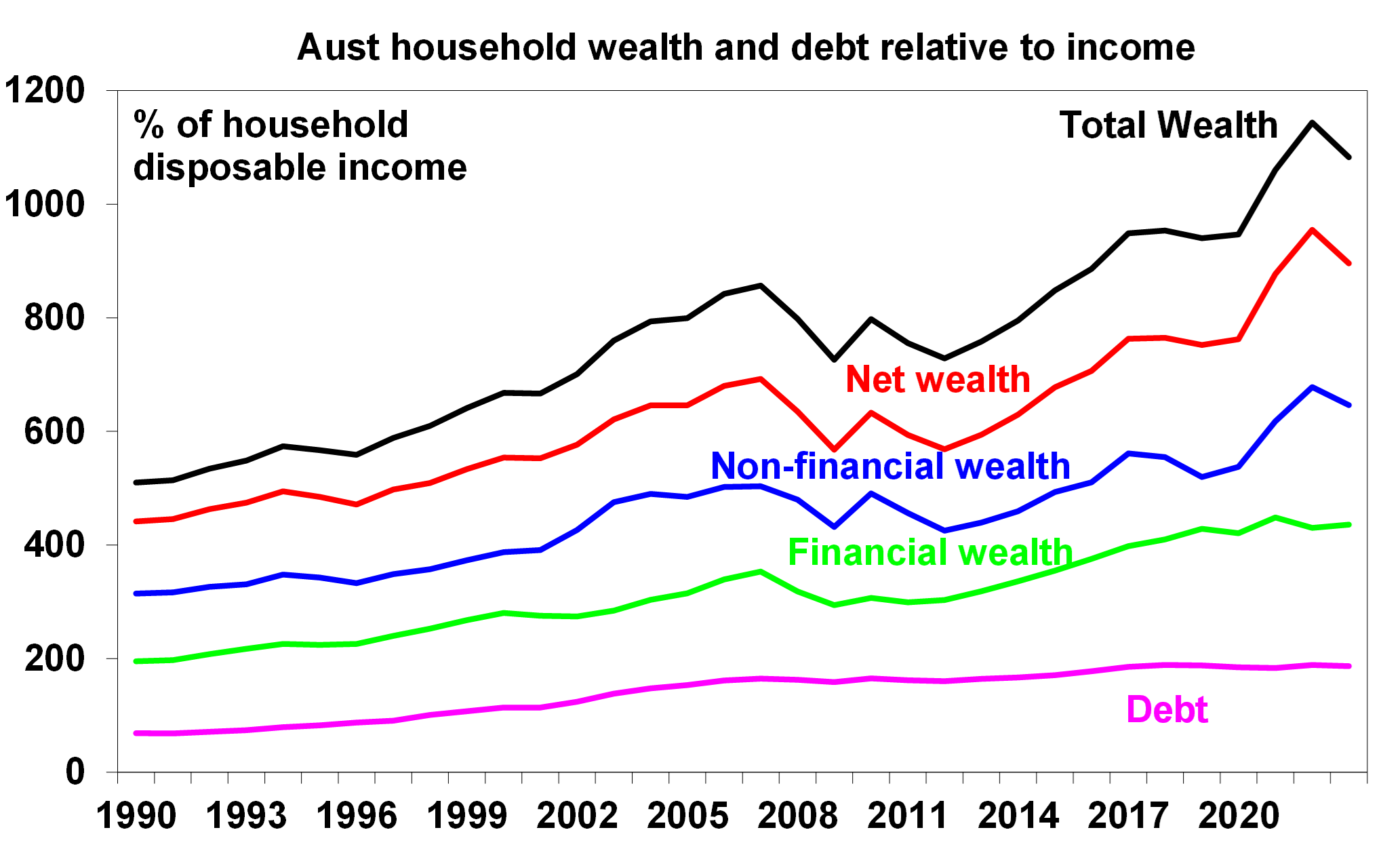

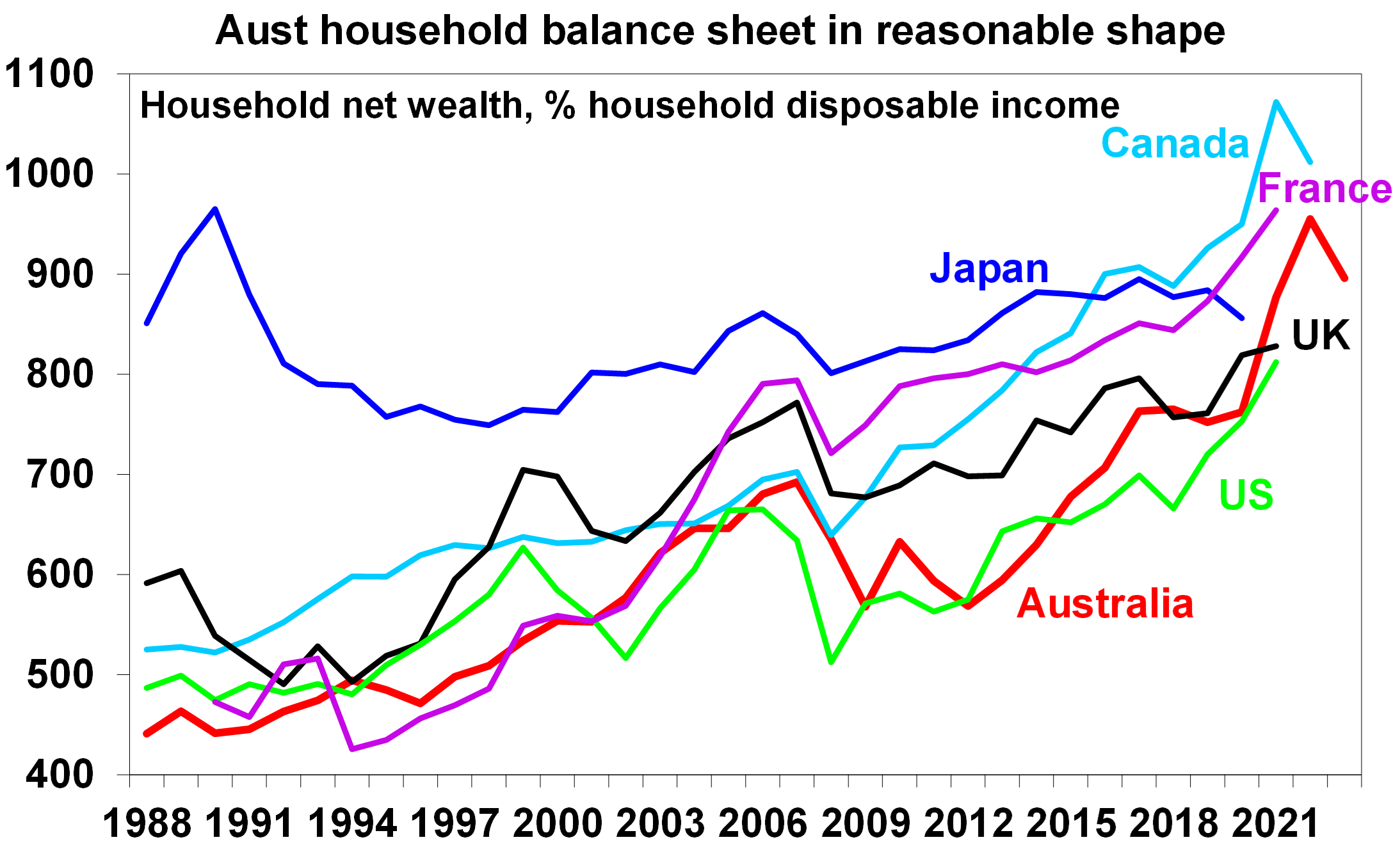

The Australian Bureau of Statistics estimates the value of a household’s assets, liabilities and therefore wealth. Net worth or wealth is calculated as a household’s total assets minus its liabilities. Total wealth is close to 11 times the size of household disposable income (or 1083%) and net wealth is 896% of income. The latest data for the year to June 2023 showed a slight fall in wealth as a share of income, after it reached a record high in 2022 – see the chart below. Non financial wealth is worth 647% of income, larger than financial wealth at 436% and well surpassing household debt, which is 187% of income.

Source: RBA, AMP

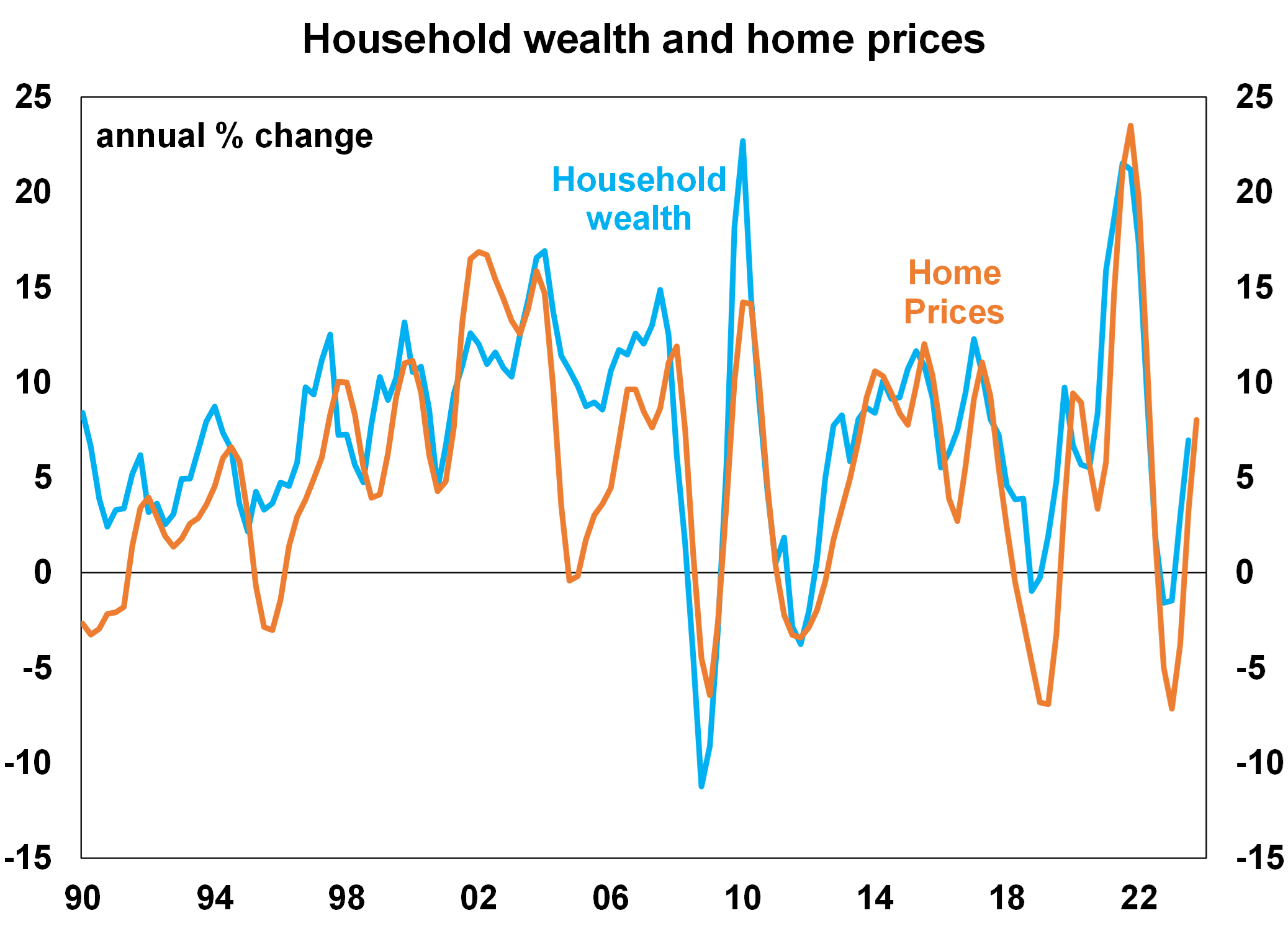

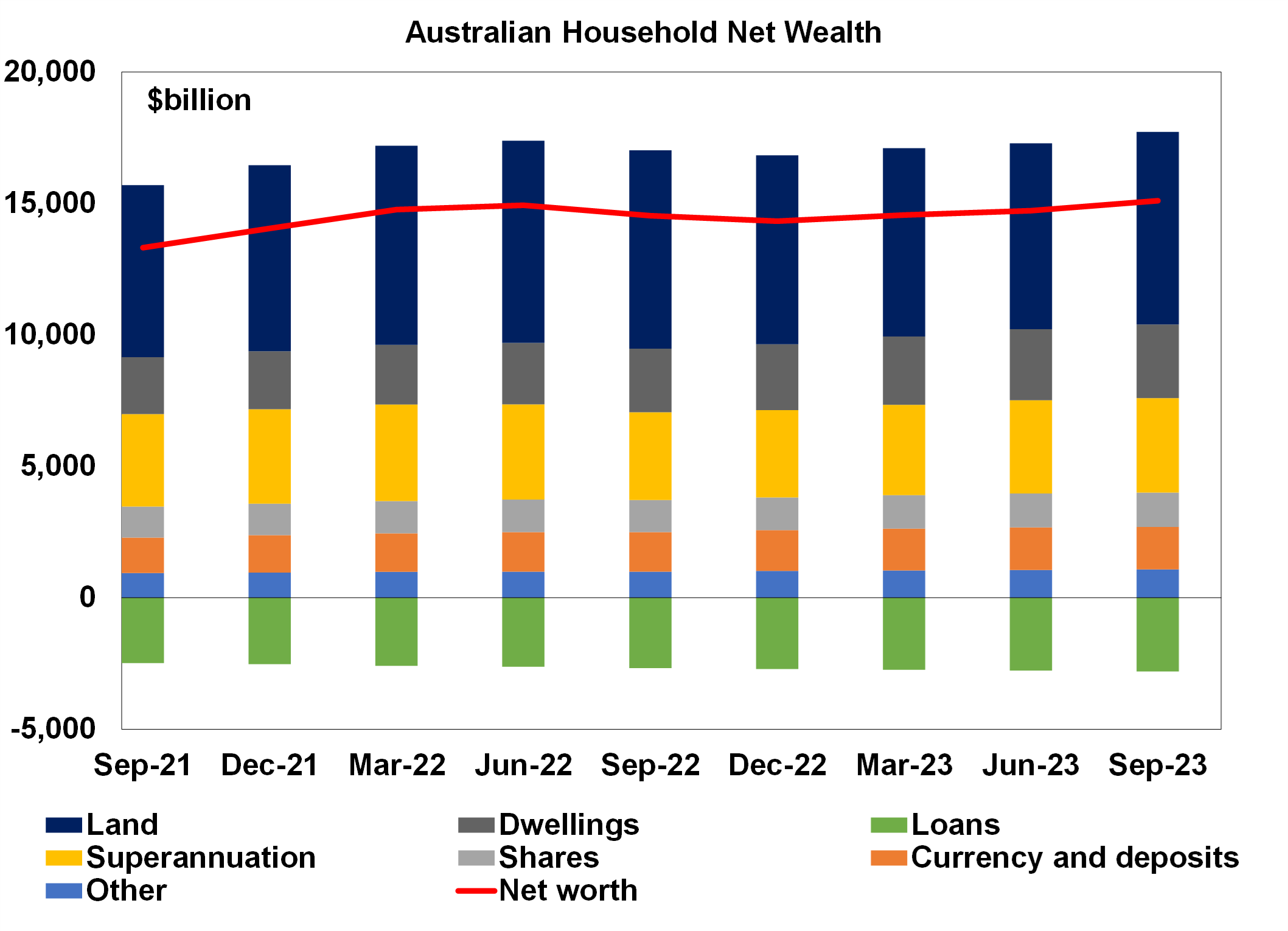

Around 70% of Australian household wealth is tied to the value of homes (which is made up of land and dwellings) and moves closely in line with home prices (see the chart below). Household wealth rose throughout 2023, in line with solid growth in home prices.

Source: ABS, AMP

Other components of household wealth are shown in the chart below. Assets include superannuation, shares and currency and deposits. Loans which are mostly for housing are the source of household liabilities.

Source: ABS, AMP

How does household wealth compare around the world?

Australian household wealth, as a share of household disposable income, is at the top end of its OECD peers (see the chart below).

Source: OECD, AMP

High holdings of wealth could be considered a source of support for households, especially against record levels of household debt in Australia. This is a concept known as the “wealth effect”. When household wealth increases, households feel more secure with their financial position and household savings tend to decrease which lifts consumer spending. When wealth decreases, households feel less secure which leads to an increase in savings and decline in spending. However, this relationship does not always work. Most recently in the pandemic, household wealth rose in 2021/22 alongside the lift in home prices but the savings ratio also surged thanks to government driven stimulus cheques. Since then, the household savings ratio has been falling but growth in total consumer spending has been low. We expect that the household savings rate will continue to fall in 2024 as it normalises after the pandemic but growth in consumer spending will still be low.

Implications for investors

Households dealt with a cost of living challenge in 2023 because of high inflation and rising interest rates. Inflation is expected to slow in 2024 and we expect the RBA to start cutting interest rates by mid year which should ease the repayment burden for households with a mortgage, as mortgage interest repayments as a share of income are rising to a record high (see the chart below).

Source: ABS, AMP

So, while cost of living issues should improve for consumers, household wealth will come under pressure in 2024 as we expect home prices will decline by 3.0% to 5%. This is likely to occur alongside a slowing in household incomes as the labour market weakens and the unemployment rate increases. This environment is expected to be negative for consumer spending and GDP growth. We see GDP growth rising by 1.2% over the year to June 2024, below the RBA’s forecast of 1.8% and anticipate the unemployment rate to increase to 4.5% by mid year. This should see the RBA cutting interest rates by June and we expect a total of 3 rate cuts in 2024.

Wealth inequality between households is also an issue in Australia. The top 20% of households (by income quintile) owned 63% of total household wealth in 2019-20 but the bottom income quintile (the bottom 20%) owned less than 1.0% of all household wealth. In Australia, there is also increasing generational wealth gap, with wealth across older households increasing significantly over recent decades but this has not been the case for younger Australians. There are numerous government policies that could address these issues of wealth inequality, including improving the housing affordability issue (through lifting housing supply and/or looking at the favourable treatment of housing investment) and doing a tax review (looking at broadening the GST and examining the merits of a wealth or death tax), which could help the wealth inequality issue.

Source: AMP

Money worries and your mental health

By Robert Wright /September 08,2021/

It’s been a trying time for many people, with our collective mental health taking a toll as the COVID-19 pandemic rolls on. The Melbourne Institute says one-in-three Australians are now reporting financial stress, while one-in-five are feeling ‘mental distress’.

It’s well known that our financial wellbeing and mental health go hand in hand. Severe or prolonged financial stress can trigger symptoms of anxiety and depression, relationship breakdowns, trouble sleeping and anti-social behaviour. This in turn can lead to further poor decision making when it comes to money.

Fortunately, there are things you can do to improve your financial security and wellbeing. If you’re experiencing financial stress, here are some practical steps you can take to get back on track.

Give yourself a financial health check

When you’re experiencing financial stress or hardship, it can be tempting to avoid the problem altogether; but this only makes things worse. Once you gain a clear understanding of your financial position, you’ll feel more in control and can take steps to improve your position.

Start by doing a financial health check to assess where your income is going. Use a spreadsheet or budget planner to list your income, debts, and expenses. Then look for opportunities to reduce your expenses, pay down debt and increase your savings.

Renegotiate your bills

Renegotiating what you owe is a smart way to free up some cash flow for daily living and ease the pressure you feel about meeting your obligations.

If you’re having a hard time meeting expenses, it’s important to speak to your service providers as soon as possible. Let them know you’re doing it tough and ask to negotiate lower repayment amounts and extended timeframes.

Don’t be shy to ask for a better deal on any services you use, including phone bills, internet, and utilities. Most organisations will try to work with you – it’s better for them to get paid (albeit slowly) than for you to default on what you owe them.

Pay down debt

With more cash flow available, you can concentrate on clearing your debts, a key step on the path to financial freedom. If you have lots of debt, it’s worth seeking the advice of a financial adviser. They can advise you on the most efficient and cost-effective way to repay what you owe. You might be able to refinance, take advantage of ‘no-interest’ periods or consolidate your debts into a single monthly repayment at a lower rate.

Make bank accounts your best friend

Keeping all your money in one bank account makes it hard to keep track of how much you have and how much you owe. One simple strategy to help you manage your money is to set up several bank accounts, each with a different purpose. For example, one to receive your income, another to pay household expenses, one for discretionary ‘spending’ and one for saving.

You can set up automatic payments to transfer the right amount of money into each account when you get paid. That way, you’ll always have the money put aside to pay your bills as they arise. Make sure to set up direct debits or automatic payments for each of your regular household bills from your expense account, so there’s no chance of falling behind in future.

Build your savings

Feeling financially secure goes hand in hand with having a good financial safety net in place. The more you have put aside for a rainy day, the less stressed you’ll feel when things don’t go to plan. Aim to build up your emergency fund to cover six-months’ worth of living expenses for yourself and your family. Again, creating an automatic transfer of funds to your ‘emergency’ savings account each month is an easy option. Then sit back and watch your savings grow.

Where to get help

If you’re experiencing financial hardship, struggling to make ends meet, or find yourself on the wrong end of one too many late payment notices, remember, there is help available.

Source: Money and Life

Five Financial habits to start

By Robert Wright /April 16,2021/

Like any habit, our financial behaviours are formed by doing the same actions repeatedly until they’re second nature. That’s great if you’ve got into the routine of saving regularly – but not so good if you’re one to whip out the credit card on impulse.

With the right approach, you can turn those less-than-helpful financial habits into healthy behaviours.

Research shows one way to avoid falling back into old ways is to replace them with healthier habits. Other useful strategies include:

- Making smaller changes rather than big, dramatic ones.

- Choosing specific actions like ‘I’m going to transfer $100 into a dedicated savings account every fortnight’ rather than vague goals, such as ‘I want to feel financially secure’.

- Triggering new behaviours with visual or sound cues – that’s why social media with its notifications can be so habit-forming.

Here’s how to use those strategies to set you up for a financially successful 2021.

1. It’s time to get organised

Knowing where you are financially gives you clarity around your money. This makes it easier to workout your financial goals – and what you need to meet them.

Start by having a place for everything. If you receive your bills electronically, save them in one place. Scan any other financial paperwork – or set up a folder if you prefer hard copies. Consider setting up direct debits or create calendar alerts to ensure you pay bills on time – and avoid late payment fees forever.

You can’t control your money if you have no idea where it’s going or how much is coming in. Using a budgeting app can help you easily track your expenses and get an accurate record of your monthly spend. You can use this information to create a realistic budget. You can also use your bank’s app to manage your day-to-day expenses and check your balance.

Don’t forget to record expenses as you go and photograph or scan receipts, so when tax time comes, you’ll have all the documents you need in one place.

2. Name your goals – And break them down into steps

What are your financial goals? Some common ones include:

- Buying a property or starting a business

- Going on a dream holiday

- Paying for the kids’ or grandkids’ education

- Leaving money for loved ones

- Retiring early

- Being free from debt/paying off the mortgage

Enjoying financial freedom. Once you know what your goals are, break them down into small, actionable steps. For example, say your goal is to buy a property. Work out first how much your ideal home will cost, how much you’ll need for a deposit and when you hope to purchase it. Next, decide how much you’ll need to set aside each fortnight for that goal. Don’t forget other sources of income that could add to your savings – like a tax return, bonus, or income from a second job.

3. Pay yourself first

One of the most important financial behaviours you can develop is the habit of saving regularly. You need some savings as a safety net – covering unexpected expenses like home or car repairs, or a trip to the dentist. You can then use additional savings to cover your financial goals, or to invest in assets like shares or property.

One of world’s most successful investors, Warren Buffett offers this advice on saving: “Don’t save what is left after spending; spend what is left after saving.” In other words, pay yourself first.

One way to do this is to automatically transfer a regular amount into a savings account each pay day. By taking the same amount out at the beginning of the pay cycle, you’ll get used to not having it. If money is tight, make the amount small.

Check the balance of your savings account regularly. This will give you the visual reward of seeing your savings account grow – helping motivate you to stay on track.

4. Set a debt repayment strategy

If you have credit card debt, try to pay off as much as you can each month. Make sure it’s more than the minimum, or you could end up paying a lot of money in interest.

If you have multiple debts, they may be easier to manage by consolidating them into one debt. Alternatively, pay off the debt with the highest interest rate first. Some people find paying off the smallest debt first, then moving onto the next smallest debt more motivating.

To avoid getting into more debt, try to avoid impulse buying. Consider having a credit card for emergencies only and relying on your everyday account to pay for groceries and other expenses. Even better, build up a rainy-day account and avoid credit cards altogether.

5. It’s never too late to learn

Do you find finances confusing, boring or stressful? Learning more about finances can take the hard work and mystery out of managing money.

Source: Colonial First State