Tag Archives: Financial Planning

How much super do I need to retire in Australia?

By Robert Wright /August 22,2025/

The amount of super you need to support your retirement will depend on what kind of lifestyle you’re hoping to enjoy and how much income you’ll be earning in addition to your super savings. Income from the Age Pension, part-time work and other financial investments will affect the amount of super you need to retire comfortably.

The Association of Superannuation Funds of Australia (ASFA) provides yearly total income recommendations based on the type of retirement you’re aiming for. Depending on how much income you expect to receive from other sources, you can then estimate how much super you’ll need to reach the “comfortable” or “modest” benchmarks.

The table below gives you an idea of how much retirement income you might need to enjoy a comfortable, or modest retirement, and compares these benchmarks against how much you can receive on the Age Pension.

| Comfortable lifestyle | Modest lifestyle | Maximum rate of Age Pension | |

| Single | $52,383 | $33,386 | $29,874.00 |

| Couple | $73,875 | $48,184 | $22,518.60 (each) a year |

Budgets for various households and living standards for those aged 65-84 (March quarter 2025)

Source: ASFA Retirement Standard

The amount of super you need will also depend on what you’re earning from full or part-time work, the Age Pension and other investments.

To enjoy a comfortable retirement, AFSA suggests that single people will need $595,000 in super savings at age 67, and couples will need $690,000. But your own individual goal will depend on your other income streams and personal situation.

In addition to the total amount of super you have, the way you access it once you retire can also impact your retirement wealth. For example, your super earnings might be subject to more tax if you plan to withdraw lump sums, compared to setting up a super income stream like an account-based pension.

What’s the difference between a comfortable and modest retirement in Australia?

A comfortable retirement means you can look forward to a broad range of leisure and recreational activities, with a good standard of living. ASFA guidelines suggest you’ll be able to purchase things like private health insurance, a reasonable car, good clothes and a range of electronic equipment. You’ll enjoy domestic and occasionally international, holiday travel.

According to ASFA, you can expect a modest retirement to be better than living on the government Age Pension. However, you’ll only be able to enjoy a fairly basic lifestyle.

See the charts below to get a more detailed understanding of what sort of services and luxuries you might be able to enjoy, based on your retirement savings.

| Comfortable lifestyle | Modest lifestyle | Age Pension | |

| Medical | Top level private health insurance, doctor/specialist visits, pharmacy needs | Basic private health insurance, limited gap payments | No private health insurance. |

| Technology | Fast reliable internet/telco subscription, computer/android mobile/streaming services | Basic mobile, modest internet data allowance | Very basic mobile and limited internet connectivity |

| Transport | Own a reasonable car, car insurance and maintenance/upkeep | Owning a cheaper, older, more basic car | Limited budget to own, maintain or repair a car |

| Lifestyle | Regular leisure activities including club membership, cinema visits, exhibitions, dance/yoga classes | Infrequent leisure activities, occasional trip to the cinema | Rare trips to the cinema |

| Home | Home repairs, updates and maintenance to kitchen and bathroom appliances over 20 years | Limited budget for home repairs, household appliances | Struggle to pay for repairs, such as leaky roofs or major plumbing problem |

| Haircuts | Regular professional haircuts | Budget haircuts | Less frequent haircuts, or self haircuts |

| Home cooling and heating | Confidence to use air conditioning in the home, afford all utilities | Need to keep a close watch on all utility costs and make sacrifices | Limited budget for home heating in winter |

| Eating out | Occasional restaurant meals, home delivery meals, take away coffee | Limited meals out at inexpensive restaurants, infrequent home delivery or take away | Only local club special meals or inexpensive take away |

| Clothing | Replace worn out clothing and footwear items, modest wardrobe updates | Limited budget to replace or update worn items

|

Very basic clothing and footwear budget

|

| Travel | Annual domestic trip to visit family, one overseas trip every seven years | Annual domestic trip or a few short breaks

|

Occasional short break or day trip in your own city |

Annual budgets for households and living standards for those aged 65-84 (March quarter 2025)

Source: ASFA Retirement Standard

Do I need a second income stream in retirement?

This will come down to your personal circumstances, and what kind of lifestyle you’re hoping to enjoy when you retire.

Planning ahead is a great idea if you want to supplement your super with additional streams of income. For example, you could:

- build up your financial investments

- top up your super with salary sacrifice or a personal super contribution

- find part-time employment

- apply for the Age Pension.

What government benefits could I receive?

When you retire, you might be eligible for government benefits like the Age Pension or a concession card. This will depend on your age, your residency status, and your financial situation.

As of 20 March 2025, the maximum Age Pension is:

- $1,149 per fortnight for singles ($29,874 a year).

- $866 each per fortnight for couples ($22,516 a year).

If you’re eligible for the Age Pension, you may also be able to access additional government payments, such as:

- Carer allowance: If you provide daily care to an elderly person or someone with a disability or a serious illness.

- Rent assistance: To help cover your rent if you’re renting privately.

If you’re receiving the Age Pension, the government will automatically send you a Pensioner Concession Card. Even if you’re not eligible for the Pensioner Concession Card, you might still be able to get a Commonwealth Seniors Health Card, subject to being eligible.

Either of these cards will allow you to access:

- cheaper medicines on the Pharmaceutical Benefits Scheme (PBS)

- bulk billing for doctor’s appointments

- reduced out of hospital expenses through Medicare.

Note that there may be additional concessions from state or territory governments, or from local councils and businesses.

How can I set myself up for the retirement I want?

Your first step will be to create a clear vision for the retirement you want. Ask yourself: What type of lifestyle do you want to enjoy in retirement? Modest, comfortable, or would you like even more freedom? Use the table above to figure out what you’d like your retirement to look like.

Secondly, are you currently on track to achieve this goal?

If you’re not quite on track to reach your goal, you can start thinking about strategies to boost your retirement wealth. This might include topping up your current super savings, working part-time, or building up your other financial investments.

If you’re unsure about the best way to set yourself up for a retirement which supports your personal goals, a financial adviser can help steer you in the right direction.

Calculating how much super is needed for retirement

A retirement calculator helps you estimate how much money you’ll need for the retirement lifestyle you want – and how much money you might have when you retire, based on your super savings and other assets.

The calculator will also show you the impact of potential investments, fees and voluntary contributions to your super and your retirement wealth.

Consider the ASFA benchmarks for a modest and comfortable retirement, other income streams like part-time work or investments and your own financial goals when determining how much super you’ll need when you retire.

How can I grow my super?

Topping up your super is a good way to boost your retirement wealth and may provide tax-concessions in the short term.

Currently, your employer must pay 12% of your ordinary time earnings into your nominated super fund. These contributions are called Superannuation Guarantee (SG) contributions. However, there are a few different ways you can contribute more of your own money towards your super.

As super compounds each year, even a small contribution can go a long way towards building up your retirement wealth so you can enjoy the type of retirement you want.

If you’re still not sure about the best way to set yourself up for retirement, consider speaking with a financial adviser. They’ll review your personal situation and help you find the solution which best suits your life stage, financial goals and risk tolerance.

Source: Colonial First State

Carry forward concessional contributions

By Robert Wright /August 22,2025/

If you’re looking for ways to potentially increase your retirement savings while reducing tax, carry forward concessional contributions could be a good option.

Carry forward concessional contributions

If you’ve had time out of work raising kids or for other lifestyle reasons, or you haven’t had the money to boost your super until now, you could take advantage of carry forward concessional contributions (also known as catch up contributions).

If you’re eligible, the Australian government allows you to catch up on your super contributions by adding in more than the annual limit, so you can enjoy life at retirement without worrying about money.

What are carry forward concessional contributions?

Carry forward concessional contributions, also known as catch up contributions, fall under concessional (before-tax) contributions. Concessional contributions include:

- employer contributions (such as super guarantee and salary sacrifice).

- personal contributions that you claim as a tax deduction.

There is an annual cap for concessional contributions which is currently $30,000.

If eligible, you can contribute more than $30,000 this financial year by using any unused concessional contributions caps from the previous five financial years.

Benefits of carry forward super contributions

Making additional before-tax contributions can be a tax-effective way to boost your retirement savings.

Super contributions are taxed at 15% (up to an additional 15% tax may apply to higher income earners) which is often a lot lower than most peoples’ marginal tax rate (rate of tax you pay on your personal income) which can be up to a maximum of 47% including the Medicare levy.

Any earnings you receive on your contributions once they are in your super account are also only taxed at up to 15%.

Case study examples

Here’s a few examples of how carry forward concessional contributions could benefit you.

Example 1: Tax savings

John, a 50 year old with a total super balance under $500,000. He receives a bonus at work and decides to use the bonus to make additional concessional contributions to super including unused amounts from the previous five financial years.

This not only helps him save more for retirement but also reduces his taxable income and tax liability for the year.

Example 2: Boosting retirement savings after a career break

Mark took a career break in his early 30s to care for his children. When he returned to work, he wanted to catch up on his super contributions. His total super balance was $400,000. The carry-forward rule allowed him to use the unused cap from up to five previous financial years when he wasn’t working. He did this by making regular salary sacrifice contributions through his employer which helped him rebuild his super balance more quickly as well as providing additional personal income tax savings.

Example 3: Accelerating retirement savings close to retirement

Lisa, who is in her late 50s, is planning to retire in a few years. She realises her super balance is not as high as she’d like it to be at $300,000. Carry forward concessional contributions enable her to decrease her tax and increase her super savings in the final years before retirement, giving her a better lifestyle in retirement. She does this by making salary sacrifice contributions through her employer.

Eligibility rules for carry forward concessional contributions

To make a carry forward concessional contribution, there are specific conditions you need to meet:

- You need to be under the age of 75 – your contribution must be received by your super fund on or before 28 days following the end of the month you turn 75.

- Your total super balance needs to be less than $500,000 on 30 June of the previous financial year.

- You can only carry forward unused concessional contributions from 1 July 2020.

- Unused concessional cap amounts can only be carried forward for five financial years until they expire.

Eligibility criteria for super contributions, including carry forward concessional contributions, can change over time. It’s essential to check with the Australian Taxation Office or consult a financial adviser for the most up to date information.

Calculating your carry forward concessional contribution amount

Check your previous 30 June total super balance with the ATO. This is available via the MyGov website. You want to ensure your total super balance is under $500,000 as at the previous 30 June.

Once you login to your account, you can also use MyGov to work out the amount of unused concessional contributions cap that is available.

Important things to consider for carry forward concessional contributions

Keep in mind that carry forward concessional contributions are part of the concessional contributions cap, which includes employer contributions (such as super guarantee and salary sacrifice contributions) and personal contributions that you claim as a tax deduction. When determining the amount of unused concessional contributions cap that is available for the current financial year, consider any future concessional contributions you intend to make.

It’s also important to remember that you can’t access your super until you meet a condition of release, such as reaching age 65 or age 60 and either retiring or ceasing work.

To use up carried forward concessional cap amounts, you may want to make salary sacrifice or personal deductible contributions to super.

How do super bring forward rules differ to carry forward concessional contributions?

Super bring forward rules

Super bring forward rules relate to after-tax contributions, allowing you to contribute more into super in a shorter period. Under these rules, you can bring forward up to two years’ worth of non-concessional (after-tax) contributions.

The annual non concessional contributions cap is $120,000 for the 2025-26 financial year. However, using the bring forward rule, you could contribute up to $360,000 if eligible.

If your total super balance is less than the general transfer balance cap of $2.0 million, you may be eligible to make non-concessional (after-tax) contributions. Depending on your total super balance you may be able to use the bring forward rule.

Carry forward concessional contributions

Carry forward concessional contributions are for before-tax contributions, enabling you to make up for past years where you may not have utilised all your concessional contribution caps. Generally, concessional contributions reduce your personal taxable income and tax payable.

Ready to make a carry forward concessional contribution?

Adding a little extra to your super can be a great way to boost your super savings for retirement.

Frequently Asked Questions

How do I determine my carry forward contributions for the current financial year?

Carry forward concessional contributions are in addition to the current financial year’s concessional contributions cap ($30,000 for 2025-26). Your carry forward concessional contributions or unused concessional contributions cap for the previous five years, can be obtained from the ATO using MyGov. Check that the information in MyGov is consistent with what you believe has occurred.

Do I need to notify my super fund to make carry forward concessional contributions?

If you intend to claim a tax deduction for personal contributions, you must lodge a valid notice of intent to claim a tax deduction with your super fund. Strict timing requirements apply. However, you don’t have to notify your super fund that you intend to use carry forward concessional contributions.

Can I make carry forward concessional contributions at any time during the financial year?

Generally, you can make carry forward concessional contributions at any time during the financial year, however:

- where personal contributions are made on or after age 67, a work test or work test exemption must be satisfied in the financial year to be eligible to claim a tax deduction.

- if you’re turning 75, a personal tax-deductible super contribution cannot be made after 28 days following the end of the month you turn 75.

- there are strict timing requirements for lodging a notice of intent to claim a tax deduction with your super fund. See the ATO website for more information.

What are the tax benefits of carry forward concessional contributions?

Carry forward concessional contributions can help to reduce your taxable income for the year in which you make them. This can result in potential tax savings, especially if you’re in a higher tax bracket.

Source: MLC

The absurdity and calamity of US tariff policies

By Robert Wright /May 23,2025/

US tariffs are poorly designed, badly implemented and are already damaging both the US and global economies. The economic damage will only get worse as uncertainty further undermines business and consumer confidence and results in dislocation of global supply chains.

Determining the extent of economic damage, and financial market implications, is difficult because we don’t know what tariffs will actually be implemented or how many backflips there are before then. There’s no clear, defining strategy. The justification for tariffs oscillates between reinvigorating US manufacturing, raising revenue to fund tax cuts, the cost of the US providing global security, the provision of the US dollar to support global trade and financial markets, and broadly addressing an ‘unfair’ trading system. Different justifications would lead to different structures of the tariff regime. Adding to uncertainty, key individuals in the administration have different goals for tariffs.

- The obsession with bilateral trade deficits is baseless

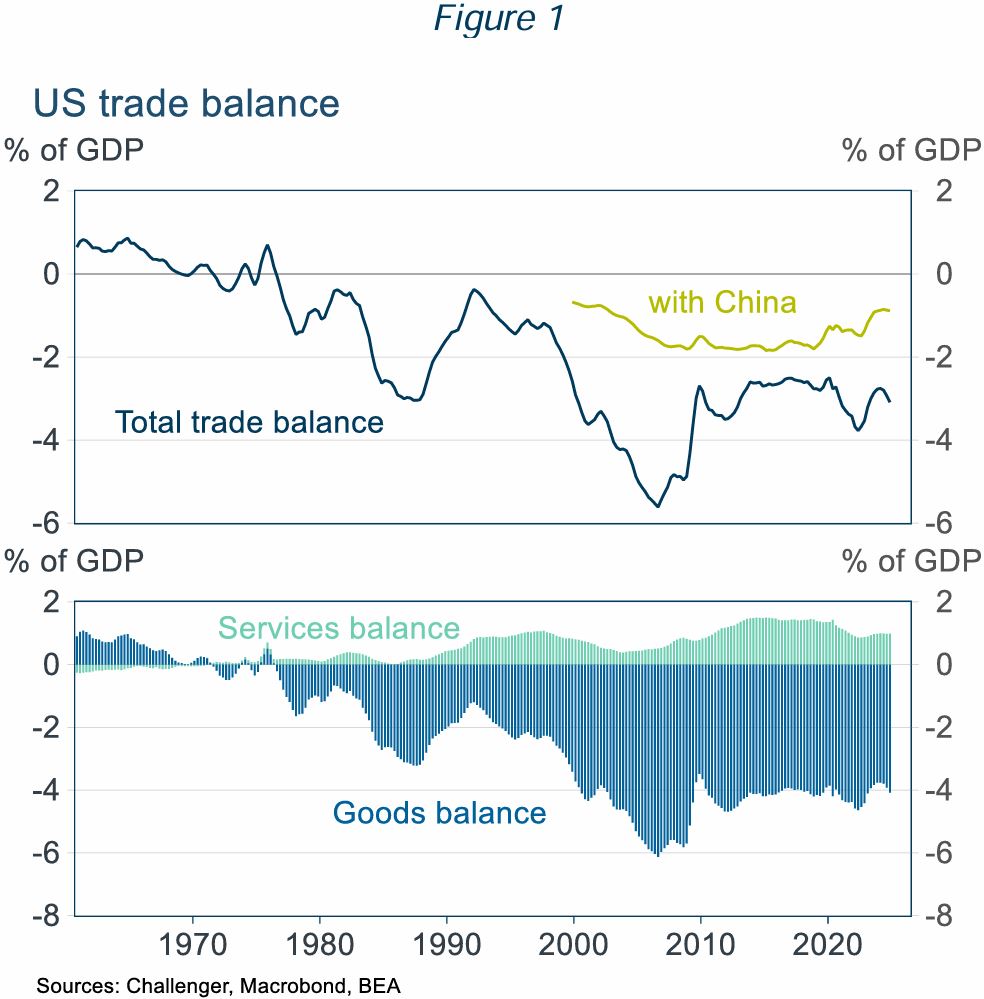

President Trump’s tariff obsession is rooted in a dislike of trade deficits. The United States has run a trade deficit since the mid-1970s (Figure 1). He attributes this deficit to unfair trade policies in other countries and an overvalued US dollar, resulting from US dollar demand given its role in international trade and finance. But the trade deficit also depends on US domestic conditions, notably the US Government’s huge fiscal deficit, currently 5% of GDP.

Balanced national trade doesn’t need bilateral balanced trade

Even if balanced trade at the country level was desirable, there is no reason for this to apply country by country. Even countries with balanced aggregate trade run large trade deficits or surpluses with almost all of their trading partners: Belgium had balanced trade with just two countries; and Canada, Finland, South Korea and South Africa each had balanced trade with just one of their trading partners. Each of these five countries had significant bilateral trade surpluses or deficits with over 150 of their trading partners. The US goal of balanced bilateral trade with every country is, frankly, bonkers.

- The calculation of tariff rates is absurd

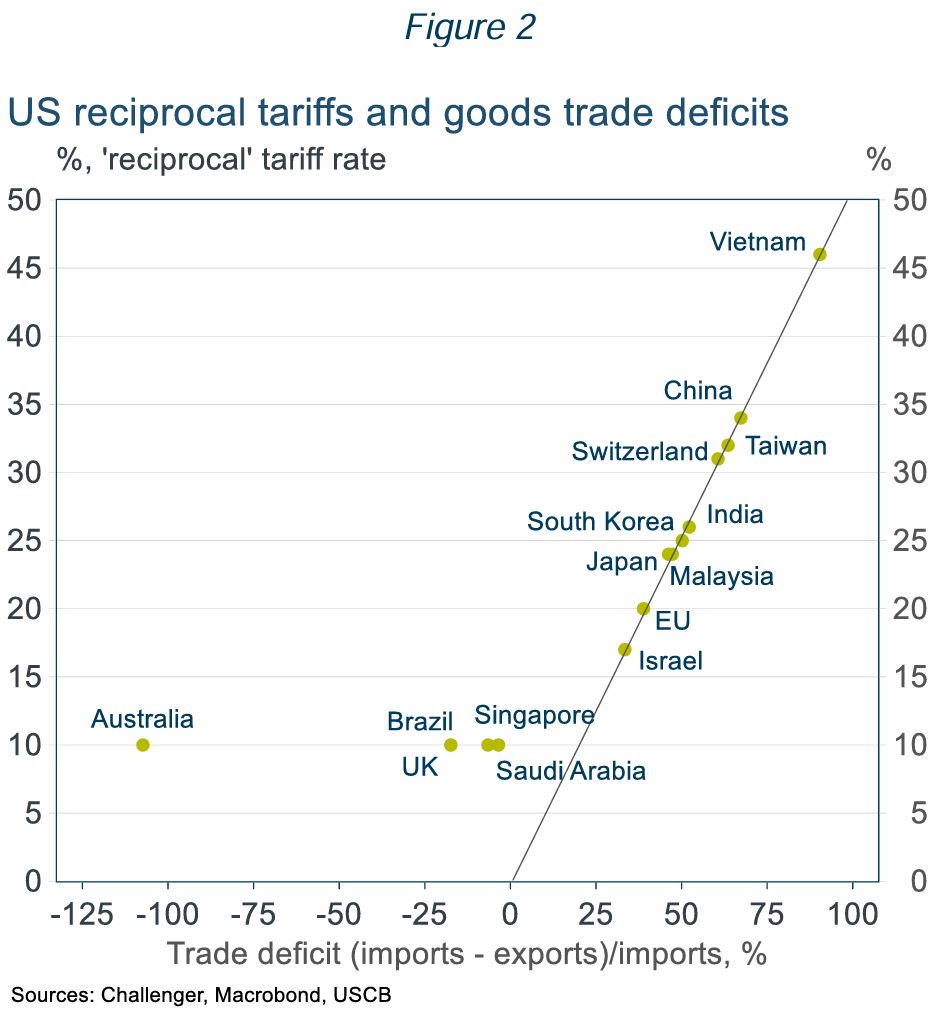

- Bilateral trade balances are meaningless but determine the US ‘reciprocal tariffs’ (Figure 2).

- Even countries the US has a trade surplus with, including Australia get a 10% tariff. If Australia applied the same logic as the US, we’d impose a tariff on the US of around 50%.

- The US has a surplus in services trade of 0.25% of GDP (partly offsetting the goods trade deficit of 1% of GDP; Figure 1) but ignores services trade in its calculation of tariffs.

- The tariffs are badly designed reflecting unclear and inconsistent goals

The US tariff regime has a mix of tariffs on specific goods (steel, aluminium, vehicles) and on specific countries (Canada, Mexico, China and the reciprocal tariffs) reflecting the varied goals of the tariffs. But many of these goals are in conflict. If, as Trump claims, tariffs raise revenue without increasing US prices by forcing foreign suppliers to absorb the tariff, then US manufacturers won’t be more competitive as US prices won’t be higher. And if tariffs are successful in boosting US production, then there would be fewer imports, and so less tariff revenue.

Several bad design elements of the tariffs mean there will be further changes:

- Different tariff rates distort trade for little benefit – for example, Apple intends to ship iPhones to the US from India rather than China as US produced iPhones would be prohibitively expensive.

- High tariffs are being applied to goods the US can’t, or won’t, ever produce – for example, some minerals and shoes (most come from China and Vietnam with 145% and 46% tariffs).

- Tariffs are being applied to inputs used by US manufacturers, increasing exporters’ costs.

- The effective trade embargo with China will be disruptive to the US economy

The 145% punitive tariff applied to China makes most imports from China prohibitively expensive. But the US economy is not ready to disengage from China, which has supplied 13% of US imports. Factories don’t pop up overnight.

Using a fine disaggregation, breaking down goods into their constituent parts, over half of US imports are from China. Alternative suppliers just don’t exist.

For finished consumer goods with very high import shares from China, large price increases and stock shortages will be disruptive to consumers and impact consumer sentiment and support for tariffs. The economic impact will be even greater for those imports predominantly sourced from China that are used as inputs in US production, such as explosives, machinery and various chemicals. For example, China is also a key source for base ingredients used in manufacturing medicines and finished medicines.

- The tariff regime won’t survive its poor design, but tariffs won’t go away completely

The US tariff regime is already unravelling with holes poked in the tariff wall.

- Reciprocal tariffs were paused until 9 July (the baseline 10% tariff still applies to all countries).

- Consumer frustration will mount facing higher prices and product shortages. For example, phones, computers and some other electronics have been exempted from the China tariffs.

- Businesses are getting traction lobbying on the cost to production from tariffs, for example there will be a partial rebate on the 25% tariffs on car parts used as inputs in US manufacturing.

- The US has said some 70 countries want to negotiate tariff reductions. Yet negotiating a detailed trade agreement takes time. The renegotiation of the US-Canada-Mexico trade agreement in President Trump’s first term took 18 months. A rushed negotiation will contain flaws.

However, President Trump strongly believes in the benefits of tariffs for promoting US manufacturing and he needs the revenue. He has committed to using tariffs to reduce income taxes, even musing that income taxes could be eradicated. But a 10% uniform tariff has been estimated to raise just $1.7 trillion over 10 years, a 20% tariff $2.6 trillion. This is substantially less than the estimated cost of $5 to 11 trillion of the tax cuts already promised by President Trump.

- What does the future hold?

There will be many more turns in the road with backflips, reduced tariffs for goods the US won’t produce or needs and new tariffs. There will be ‘deals’ reducing (but not eliminating) individual tariffs with countries committing to reduce trade barriers and import US goods (much of which will never happen).

The pause in reciprocal tariffs, after just one week, was reportedly triggered by the turmoil in bond markets which could have precipitated a financial crisis. Trump has displayed greater resolve in the face of the large fall in equity prices than in his first term. But the risk of a financial crisis, or severe recession, and sharp falls in approval ratings are likely to remain red lines that would result in some pullback.

Challenger expects ongoing tariff uncertainty and hence further volatility in markets. Aggregate tariffs will never get to the levels initially announced, but they will also be much higher than before, reducing US and global growth. Tariffs will add to US inflation, reducing the ability of the Fed to ease. Market pricing is for almost 100 basis points of cuts this year, but there’s a good chance the Fed does not even cut this year.

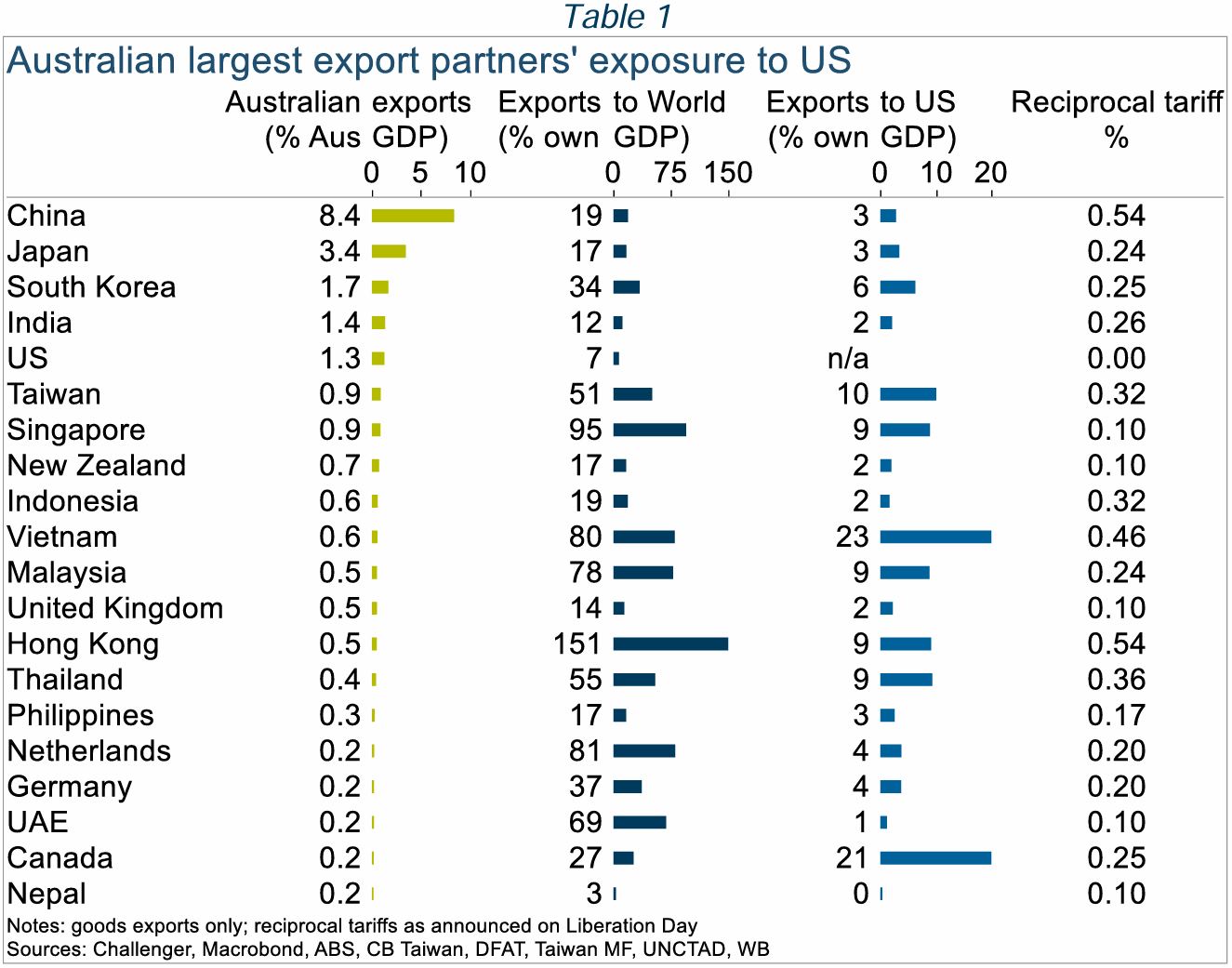

Australia will also see slower growth. We have limited direct exposure to the US economy, but our largest trading partners are more exposed (Table 1). The IMF downgraded its GDP growth forecasts for 2025 by 0.5%. Slower growth, and China’s surplus manufacturing capacity reducing Australian import prices, will lower inflation opening the path to RBA rate cuts. However, market pricing for a cash rate below 3% by December is overdone. With the worst case for US tariffs unlikely to play out, three cuts bringing the cash rate to 3.35%, around its neutral level, seems more likely.

Source: Challenger

Navigating market volatility

By Robert Wright /May 23,2025/

Financial markets have been erratic lately, understandably causing some concern for those of us with super and investments. While dips and major market events are a common feature of investing, markets generally trend upwards over time.

Most super funds invest in sharemarkets to help your money grow over in the long term. So when markets see-saw, so do super and investment balances and returns.

While this can be worrying, it’s important to remember that although the value of investments may go up and down at different times, markets tend to recover and grow over the long term. So it’s important to keep your long-term investment goals in mind.

What’s happened recently?

On 3 April, President Donald Trump announced the US would place tariffs on goods imported into the US from countries around the world. This included a 10% tariff on goods from Australia, which was the minimum rate announced on the day.

Major global economies and markets had been preparing for the announcements, but the tariffs imposed on some countries were bigger than expected. Other countries have also responded by putting similar tariffs on US goods coming into their markets.

As a result, share markets in the US and elsewhere fell sharply in the days afterwards, including the Australian Stock Exchange.

What is a tariff?

A tariff is a tax added to the cost of goods imported from a particular country or countries. It is paid to the government where the goods are being imported.

Tariffs are often used to protect domestic industries by increasing the price of foreign-made competitor products, or to raise revenue.

The cost of those items to the public will generally increase by a similar amount to the tariff.

What does this mean for markets and investments?

The US tariffs are expected to slow global trade and push up the price of some things, which could cause inflation to rise.

This could result in the Reserve Bank of Australia cutting the interest rate several times this year to prevent the economy from slowing down too much.

In the short term, you may see a negative effect on the performance of investments.

Short term volatility in response to political announcements and other geopolitical events is a common feature of investment markets.

While difficult to forecast, history shows us that markets do recover from disruptive influences – for example, from the Global Financial Crisis and the COVID-19 pandemic.

What led to this?

Since Trump’s second presidency began, uncertainty has emerged about US policy in the areas of tariffs, defence and other critical areas of government spending.

In recent months, shares have been quite weak, particularly US technology stocks. This group of stocks was optimistically priced after two years of strong growth, and therefore most at risk of uncertainty in the US market.

This has unsettled businesses amid concerns the US economy could slow. It has also fed into uncertainty in global investment markets, including the Australian sharemarket.

What does this mean for me?

As global financial markets move up and down, the value and returns of your super and investments may also change in the short term.

While this can be concerning, history shows that markets rise over time. So it’s important to keep your long-term savings and investment goals in mind and carefully consider before making any changes to your investment strategy.

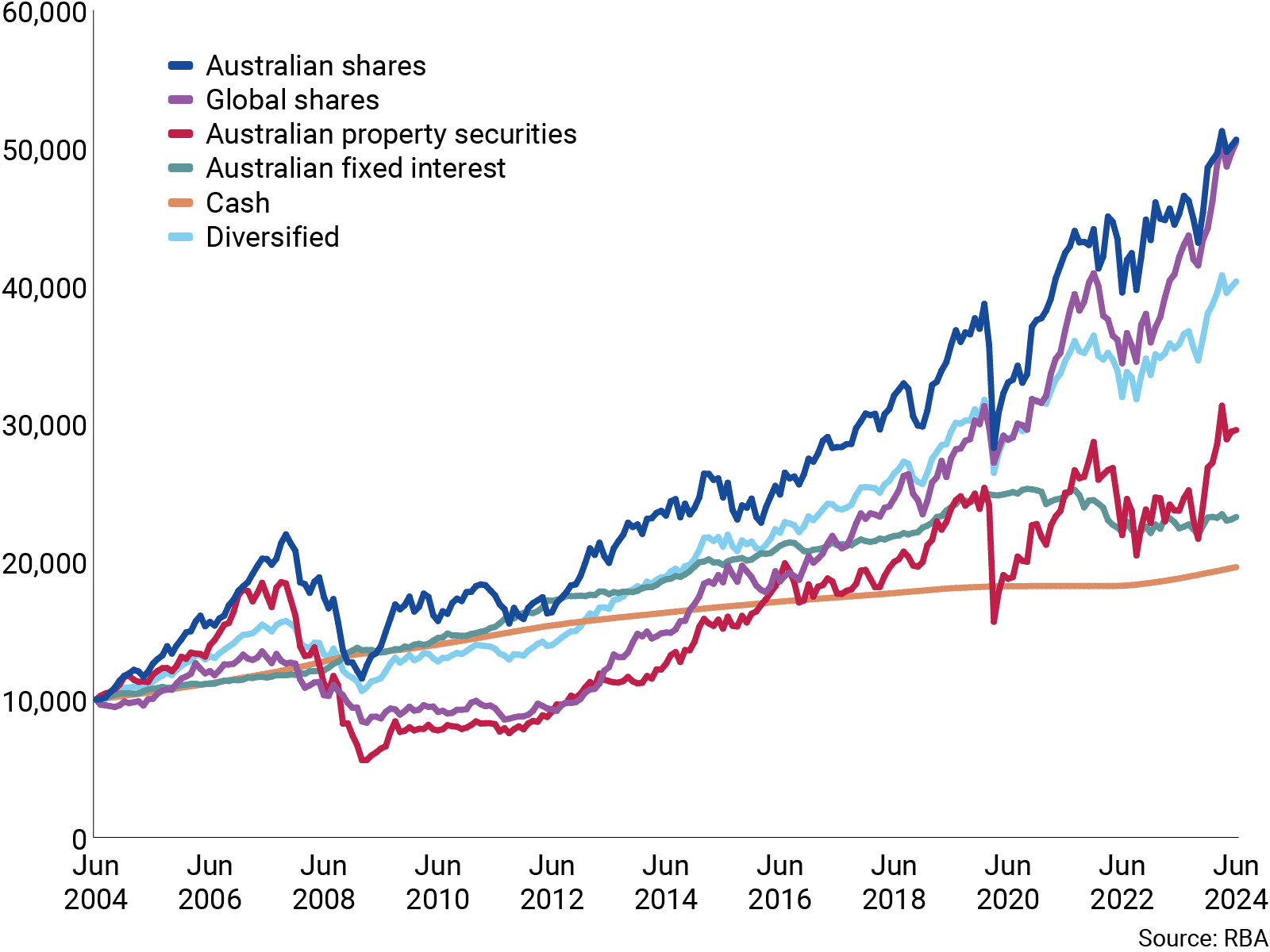

It’s understandable at times like these that some members think about changing how their money is invested. As this chart shows, the long-term trend across major investment types is positive, with shares experiencing more volatility but generating higher returns than more conservative options such as cash.

While past performance is not a guarantee of future performance, historically more time invested in the sharemarket has meant a higher return on investment.

How different investment types have performed over 20 years

It’s also worth noting that investment performance has generally been strong over the past two years, meaning the value of your investments or super may have been relatively high.

Do I need to do anything?

As with any significant market event, it’s best to avoid impulse reactions, but to take a long-term view.

Source: CFS