Tag Archives: Investing

What is risk appetite?

By Robert Wright /May 28,2024/

Risk is about tolerating the potential for losses. Understanding your risk appetite allows you to make well informed decisions about your money.

For some people, risk means excitement and opportunity. For others, it invokes feelings of fear and discomfort. We all experience a degree of risk in our everyday lives – whether it’s simply walking down the street or having investments in the share market. Everyone has a risk profile that defines their willingness to accept risk. It’s usually shaped by age, lifestyle and goals and is likely to change over time.

Risk is about tolerating the potential for losses, the ability to withstand market movements and the inability to predict what’s ahead[1]. In financial terms, risk is the chance that an outcome will differ from the expected outcome or return. It includes the possibility of losing some or all of your original investment[2]. Often you may not be aware of your risk appetite until you’re facing a potential loss, so loss aversion becomes a significant factor when making decisions related to risk.

What is risk appetite and risk tolerance?

Risk appetite and risk tolerance are used interchangeably but are different.

Risk appetite is a broad description of the amount of risk an investor is willing to accept to achieve their objectives. It’s a statement or series of statements that describes their attitude towards risk taking[3].

Risk tolerance is the practical application of risk appetite3 and considers the degree of variability in returns an investor is willing to bear.

As an investor, you should have a good understanding of your attitude towards risk. If you take on too much risk, you might panic and sell at a bad time. But if you don’t expose yourself to enough risk, you may be disappointed with your returns and potentially unable achieve your objectives.

How do I work out my risk appetite?

Think about how you might answer these questions:

- How much money do I have to invest?

- How much money am I willing to lose?

- How worried would I be if share markets fell dramatically?

- Am I planning to track your investments daily?

- Would I consider investing in different types of investments?

Your age, income and investment objectives all help determine your risk appetite.

Age: generally younger investors with a longer time horizon to invest are more willing to take greater risk with their money to earn higher potential returns. Older investors with a shorter investment timeframe may be more cautious as they’ll need their money to be more readily available and have less time to recover from a loss.

Income: people who earn more money and have a higher disposable income can typically afford to take greater risks with their investments.

Investment objectives: be clear about why you’re investing and when you think you’ll need to withdraw your money, as well as how long you need the money to last. Saving for a holiday or a deposit on a home is quite different from investing for your retirement.

Risk and Return

The relationship between risk and return underpins all financial decisions. The more risk an investor is willing to take, the greater the potential return. However, investors expect to be compensated for taking on this additional risk and should realise that taking on more risk doesn’t guarantee higher returns.

What type of investor are you?

- High: willing to risk losing more money for the possibility of better returns.

- Moderate: willing to endure short-term loss for the prospect of better long-term growth opportunities.

- Conservative: willing to accept lower returns for a higher degree of liquidity or stability.

Whatever your risk appetite, you should always consider both risk and return before making decisions about what to do with your money. Although shares and property are generally considered to be higher-risk investments, even more conservative investments like bonds can experience short-term losses. No investment is completely risk free.

This explains why smart investors typically have a diversified portfolio that includes several different types of investments.

Risk and Diversification

Don’t think that just because your friends invest in shares you should too. If you don’t have a lot to invest or you’ll want to access your money in a few years, shares may not be the right type of investment for you.

By understanding your risk appetite and being honest about what you want to achieve, you’re more likely to be comfortable with your investment decisions. A financial adviser can help you understand your risk appetite, as well as create a portfolio that suits you.

The simplest way to minimise investment risk is through diversification. A well diversified portfolio will usually include different asset classes, like shares, property, bonds and cash, with exposure across different industries, markets and countries. The idea is to reduce the correlation between the different types of investment and have a good balance of assets which move in different directions and at different times. So, if some of your assets perform poorly, others may be performing well, offsetting the poor performers.

Although diversification doesn’t guarantee you won’t suffer a loss, it’s an effective way to minimise risk and help investors realise their financial goals.

Make informed decisions

You should monitor both your risk appetite and your investment portfolio over time.

Your risk appetite is likely to change as you get older, and as your income or family situation changes.

Similarly, you should review your portfolio to ensure the risk level is still suited to your overall investment objectives. Financial markets are constantly changing, which means the underlying assets you’re invested in could change too.

If you’re a confident investor, you should check that it’s still on track to generate the level of return you want and importantly, at a comfortable level of risk. If you prefer to speak with a financial adviser, they too can help you undertake regular reviews and rebalance your portfolio, as necessary.

By understanding your risk appetite, you’re in a better position to make well informed and transparent financial decisions. It will help you identify opportunities to take on more risk where appropriate or see where you’re exposed to unnecessary risk and adjust accordingly. You’ll also avoid being caught up in the emotion of market activity, where panic can lead to a poorly timed and costly decision.

[1] Charles Schwab: How to Determine Your Risk Tolerance Level https://intelligent.schwab.com/public/intelligent/insights/blog/determine-your-risk-tolerance-level.html.

[2] Investopedia https://www.investopedia.com/terms/r/risk.asp.

[3] Australian Government Department of Finance: Defining Risk Appetite and Tolerance https://www.finance.gov.au/government/comcover/education/risk-appetite-and-tolerance.

Source: BT

Will cash remain king?

By Robert Wright /May 28,2024/

Cash has been one of the best performing defensive assets over the past three years. When compared with global bonds (a riskier asset class), a typical portfolio of term deposits would have returned a cumulative 12.6% in comparison to -8.5% for global bonds over the three years to December 2023. With interest rates expected to stay higher for longer, cautious investors would be right to question whether other asset classes are worth the risk. But are the tides changing?

On paper cash still appears to be king; however, these healthy returns are attributed to accelerated inflation and rising interest rates, an environment we may be moving away from. Inflation has been trending downwards for months and rate cuts are predicted to begin before the end of 2024.

In this paper we explain why we believe now is a good time to revisit your asset allocation.

What is a bond?

A bond is a loan made by an investor to a borrower, generally a company or government. Typically, the borrower pays the investor interest (coupons) periodically over the term of the loan and then returns the initial value (principal) of the loan back to the investor at an agreed upon future date.

Bond values are linked to the borrowers perceived ability to pay back the loan as well as interest rates. For example, when interest rates rise, newly issued bonds offer higher coupons, making them more attractive and equivalent existing bonds with lower coupons less attractive, reducing their value.

How do bonds differ from term deposits?

Bonds are expected to provide higher returns over the long term because investors require compensation for assuming investment risk. Bonds also provide the opportunity for capital growth as well as higher income. This compares with term deposits where interest payments are lower but guaranteed by a bank – providing more security. Whilst income is guaranteed, the real value of a term deposit often diminishes over time due to inflation, which erodes your purchasing power (figure 1).

Figure 1 also shows that bonds are subject to greater risk over shorter time horizons which means they won’t be suitable for everyone. Your initial investment can go down in value and when you invest in funds this can be offset through the distributions, reducing your income. This primarily occurs when interest rates are rising and become unpredictable as they have in recent times.

Investors need to determine, with support from their adviser, whether trading term deposits capital guarantee for the potential increased return of a bond investment is suitable to their circumstances.

Why now?

In an environment where inflation is trending down and rates are expected to be cut, long term bonds should perform well as this is the environment when you typically experience the most capital growth (see figure 2). Term deposit rates are also forward looking. In other words, you don’t need to wait for central banks to reduce cash rates before you start to see term deposit returns fall. There are already signs of this happening. Whilst very recent, 1-year term deposit rates came down by 0.05% in January and we expect this trend to continue (although this won’t necessarily be a smooth journey). Whilst seemingly insignificant, this could be meaningful for larger investors. Particularly where capital growth has no role to play and investors don’t require the capital guarantee of cash.

What happens if the economy deteriorates?

If a recession were to occur, interest rates are more likely be cut quicker to encourage spending, resulting in bond prices rising. This would be supported by increased demand as investors move away from higher risk assets such as equities. If we don’t enter a recession and achieve a soft-landing scenario, rates will likely trend down more slowly to bring inflation in line with central banks’ targets; once again favouring bonds due to the inverse relationship between interest rates and bond values.

Conclusion

We believe it is critical to take a diversified approach to investing to help manage portfolio risks through different market conditions. The balance and mix of assets will depend on each investor’s ability and willingness to take on investment risk as well as how much of their capital they need guaranteed.

That said, we believe now is a great time to be reassessing your asset allocation. Investors looking for capital growth who don’t need capital guarantees should consider introducing bonds into, or back into, their investment portfolio and doing so before central banks begin to cut rates.

While cash rates may seem alluring, it is important to remember the distinct roles bonds and cash play in a portfolio. Cash is best reserved for short-term spending needs that require a guarantee as it will not provide the long-term capital growth and inflation protection of other assets.

It may seem daunting as we have been through a period of significant market volatility but over the long term, we have high conviction that bonds will provide better risk adjusted return outcomes for investors who are able to take on the increased risks offered by bonds.

As always, we recommend speaking to your financial adviser to get tailored advice based on your unique circumstances prior to making any investment changes.

Source: Perpetual

Australian household wealth

By Robert Wright /February 16,2024/

Is high Australian household wealth a source of support for consumers?

Key points

- Australia ranked as having one of the lowest rates of disposable income growth per capita amongst OECD countries in mid 2023.

- An increasing income tax burden and mortgage repayments have weighed on income growth, despite solid wages and salaries.

- But, household balance sheets in Australia look stronger compared to incomes. Household wealth increased in 2023, as home prices rose.

- However, growth in household wealth will decline in 2024 as home prices are expected to fall. Household incomes will also be under pressure as earnings growth slows from a softening labour market.

- As a result, high household wealth holdings will not be enough to offset a challenging environment for households in 2024, despite some easing in cost of living challenges.

Introduction

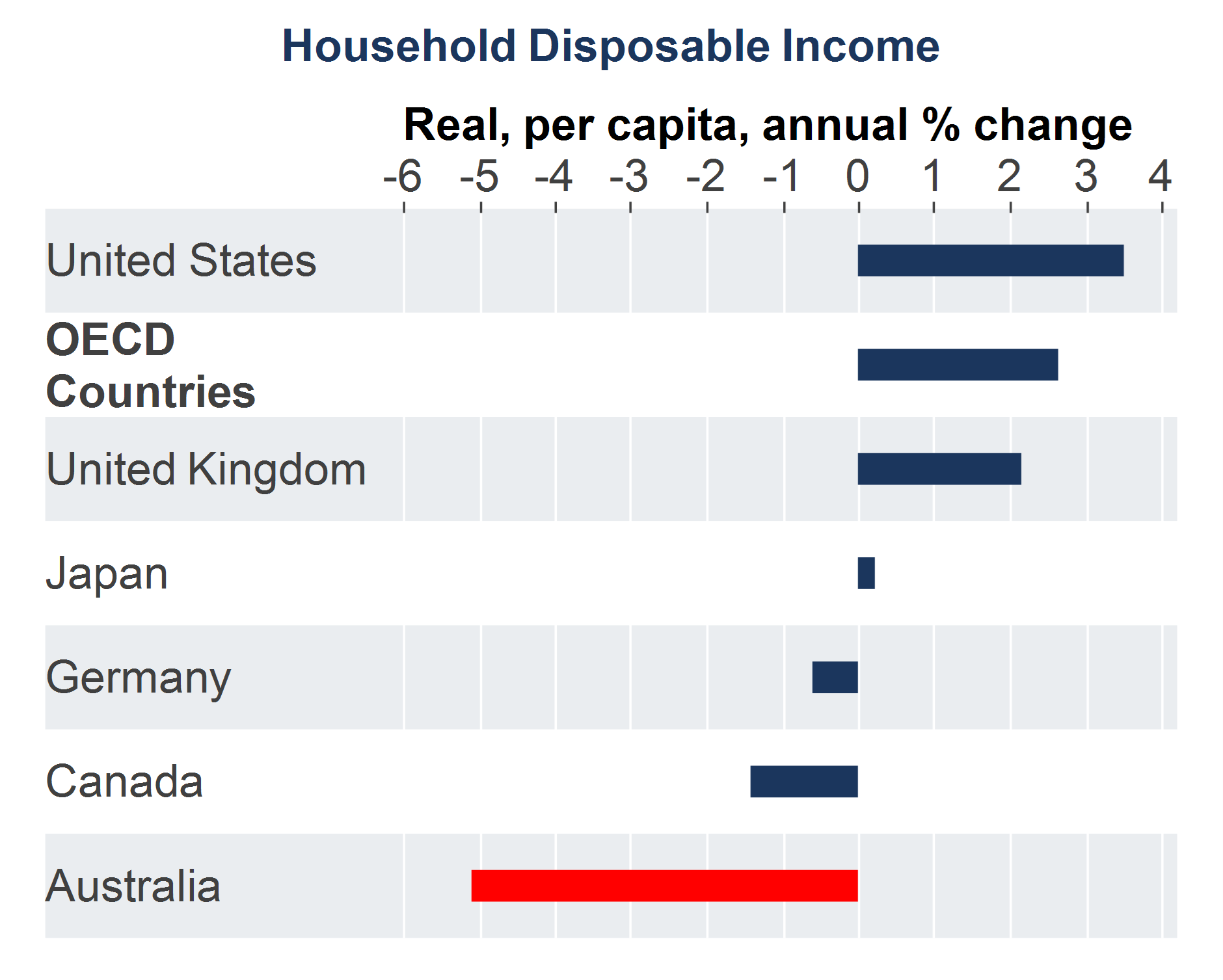

Household income data from the OECD showed that Australia had one of the lowest rates of annual real household disposable income per person compared to its OECD peers (see the chart below). Over the year to June 2023, Australia’s real per capita household disposable income was down by 5.1%, compared to a 2.6% rise across OECD countries.

Source: AMP, Macrobond

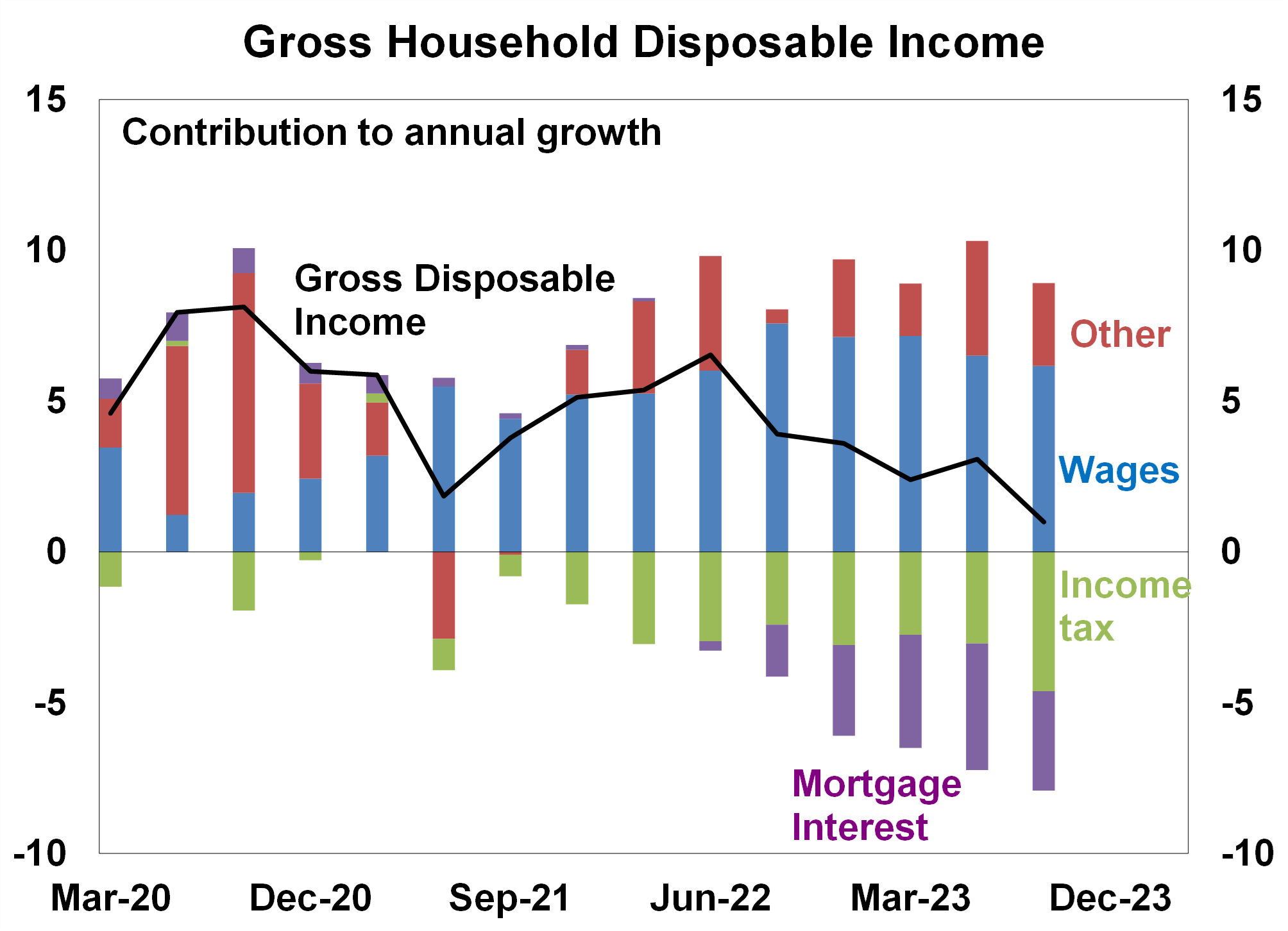

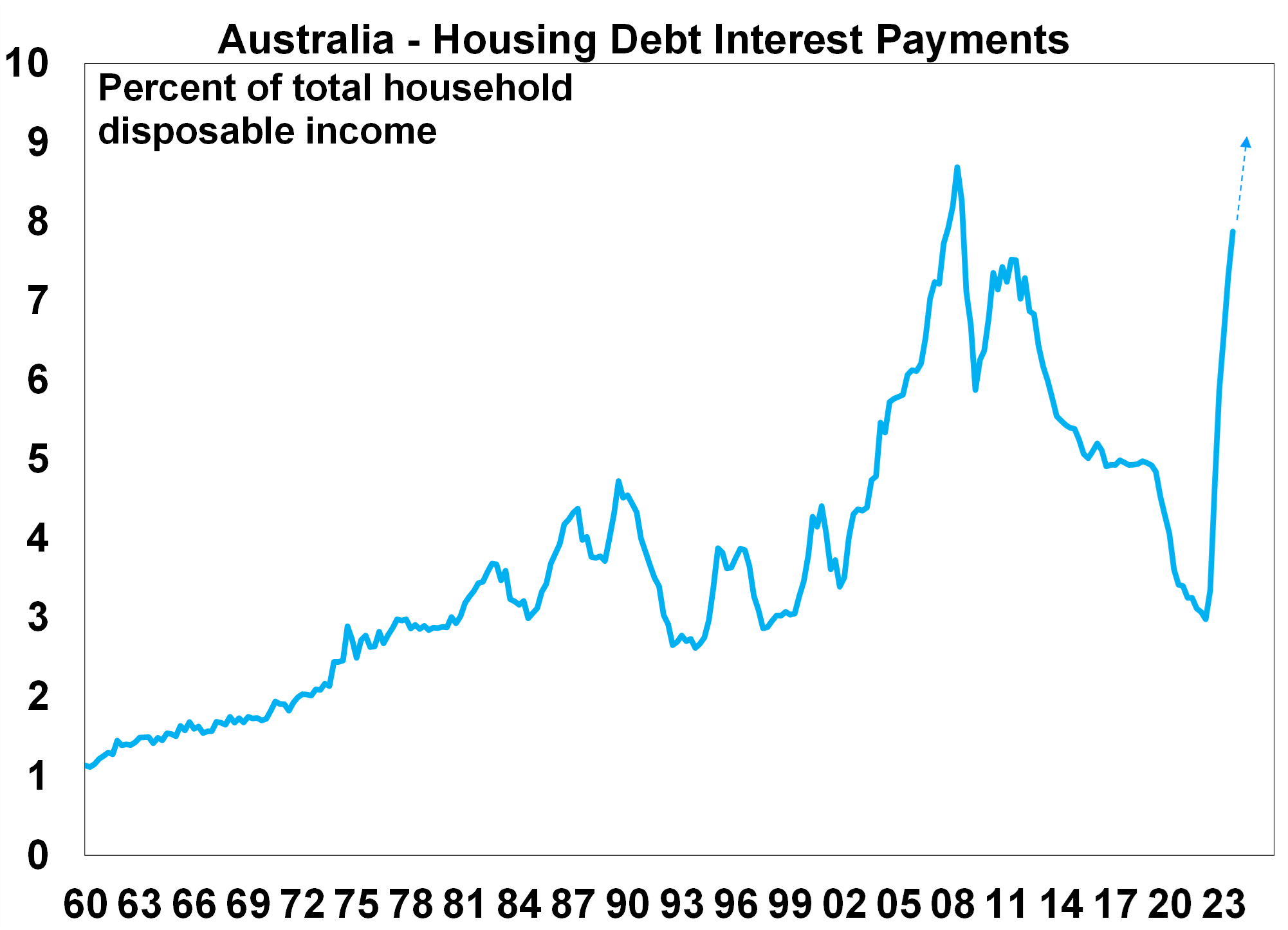

This occurred despite very healthy labour market conditions in Australia which saw employment growth running above 3.0% per annum all year, the unemployment rate remaining below 3.9% and underemployment continuing to be low, all of which boosted wages growth. Despite this positive earnings backdrop, the income tax burden increased in 2023 as households have been moving into higher income tax brackets (otherwise known as “bracket creep”), as well as the end of income tax concessions. Mortgage interest repayments are also an increasing drag on incomes (see the chart below) as the cash rate has been increased by 425 basis points since May 2022. Australia’s very high population growth in 2023 (running at 2.4% over the year to June 2023) also masked a fall in household disposable income growth per person, relative to other OECD countries.

Source: ABS, AMP

Just looking at household income accounts does not show everything about the position of households. In a country like Australia where home ownership rates are high (66% of Australian households own their home, with or without a mortgage), looking at household wealth is also important.

Household wealth in Australia

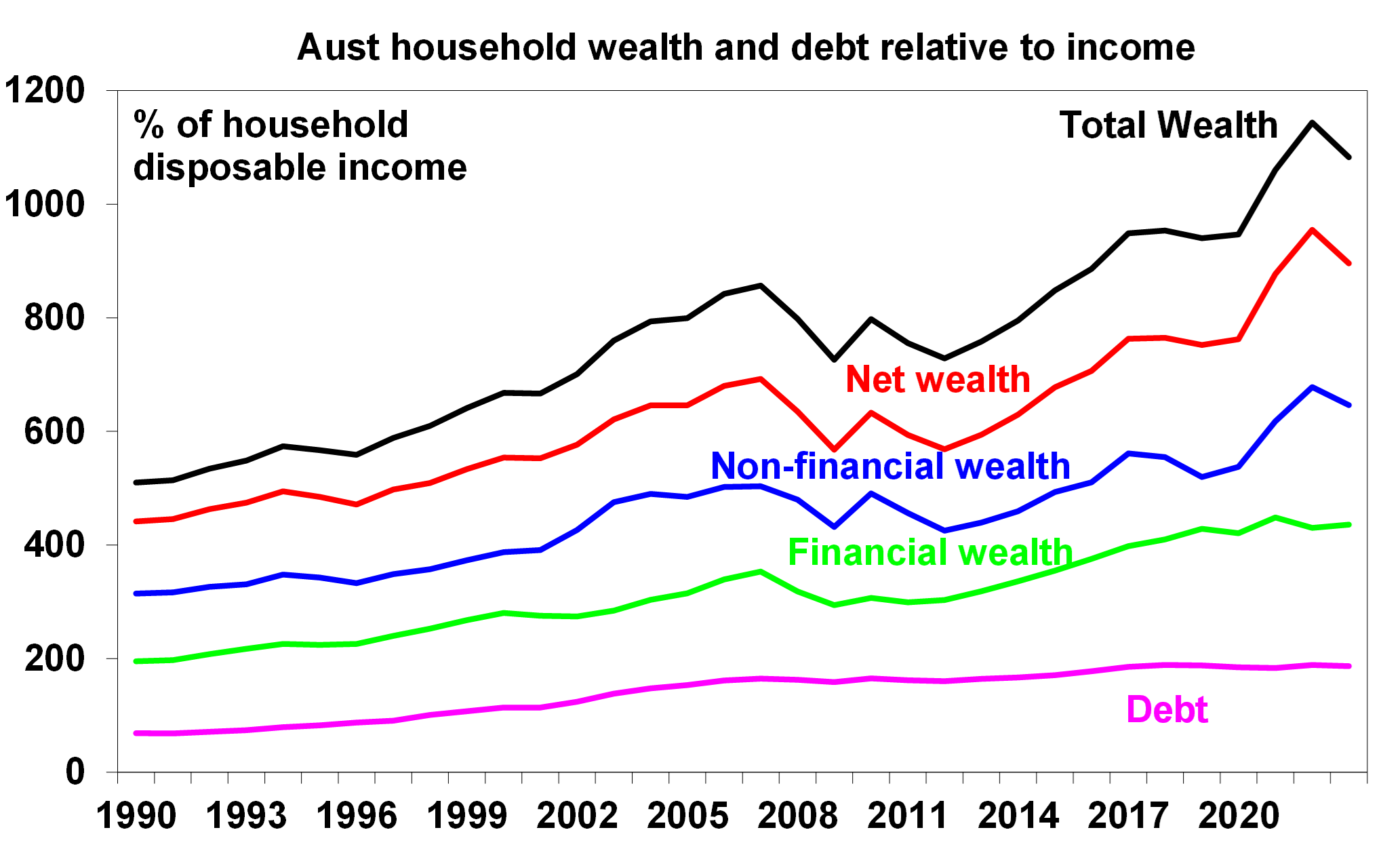

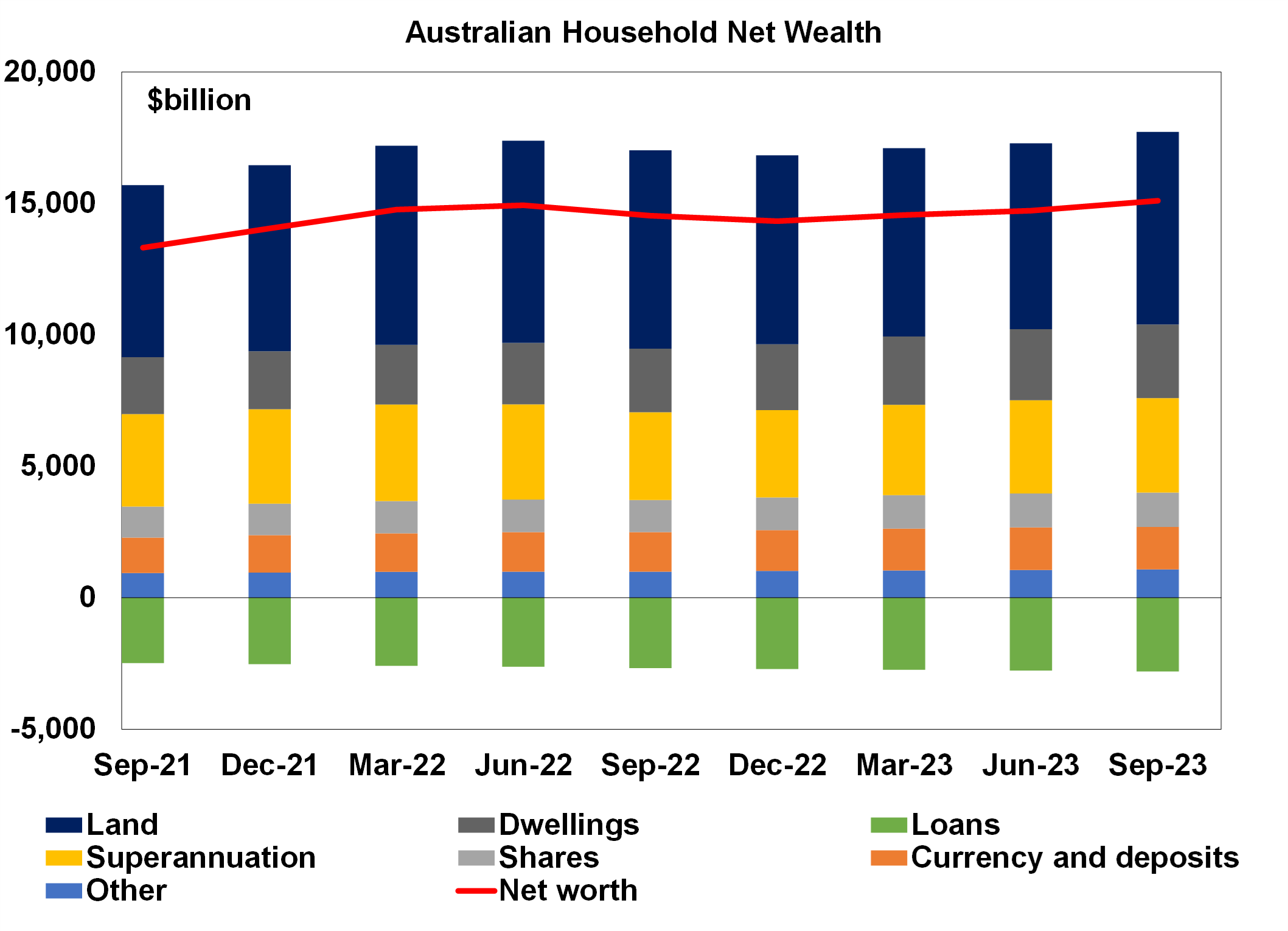

The Australian Bureau of Statistics estimates the value of a household’s assets, liabilities and therefore wealth. Net worth or wealth is calculated as a household’s total assets minus its liabilities. Total wealth is close to 11 times the size of household disposable income (or 1083%) and net wealth is 896% of income. The latest data for the year to June 2023 showed a slight fall in wealth as a share of income, after it reached a record high in 2022 – see the chart below. Non financial wealth is worth 647% of income, larger than financial wealth at 436% and well surpassing household debt, which is 187% of income.

Source: RBA, AMP

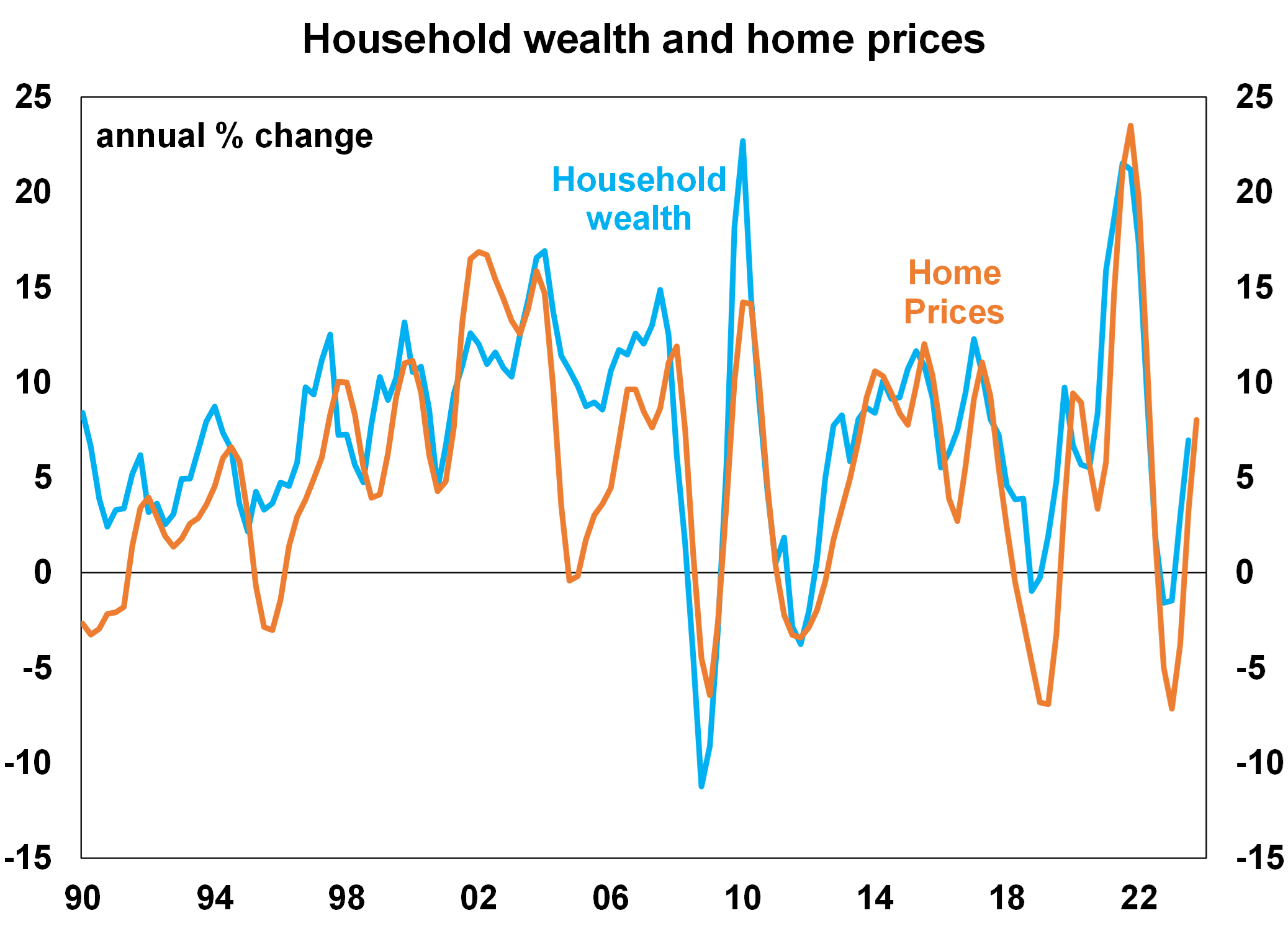

Around 70% of Australian household wealth is tied to the value of homes (which is made up of land and dwellings) and moves closely in line with home prices (see the chart below). Household wealth rose throughout 2023, in line with solid growth in home prices.

Source: ABS, AMP

Other components of household wealth are shown in the chart below. Assets include superannuation, shares and currency and deposits. Loans which are mostly for housing are the source of household liabilities.

Source: ABS, AMP

How does household wealth compare around the world?

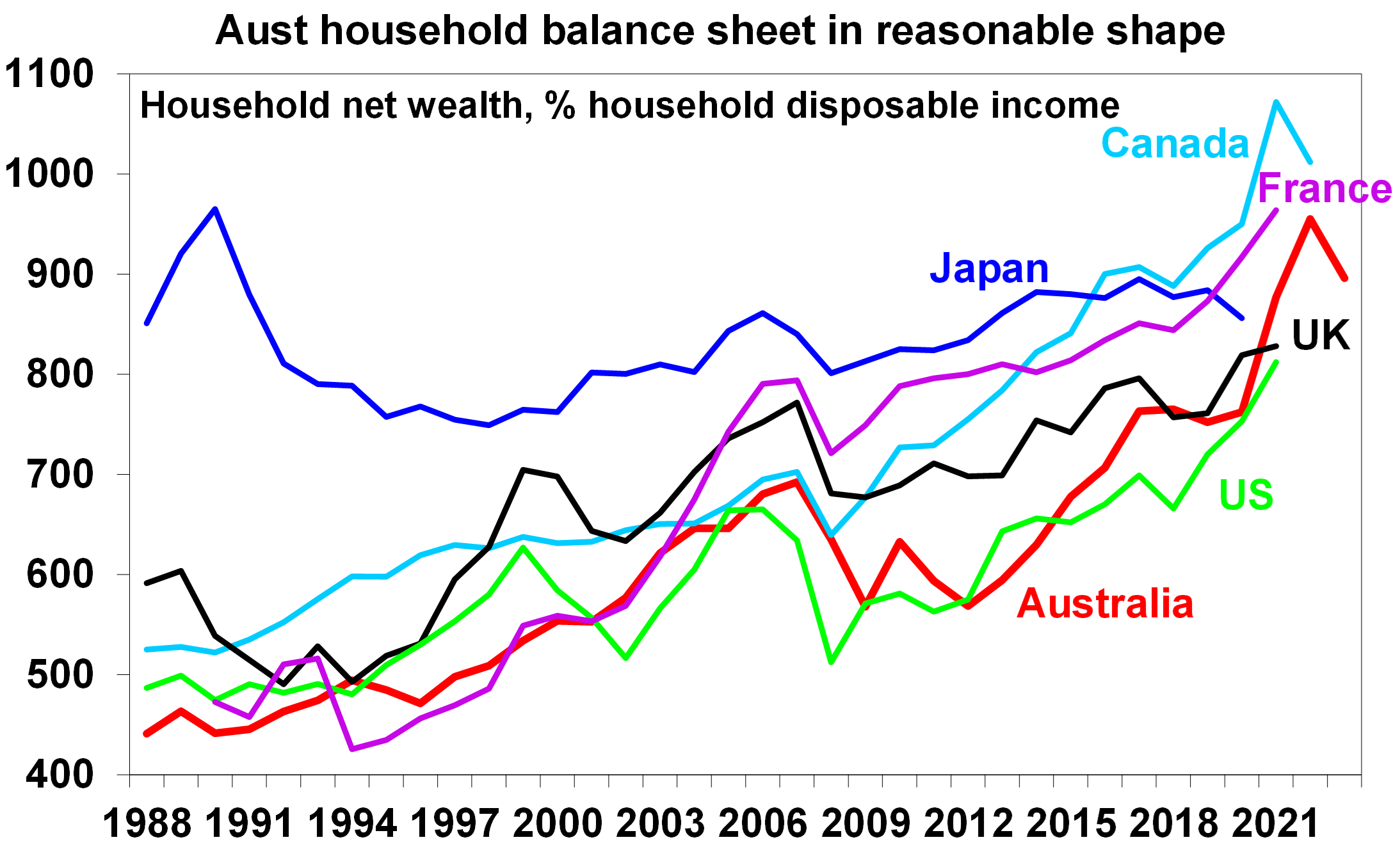

Australian household wealth, as a share of household disposable income, is at the top end of its OECD peers (see the chart below).

Source: OECD, AMP

High holdings of wealth could be considered a source of support for households, especially against record levels of household debt in Australia. This is a concept known as the “wealth effect”. When household wealth increases, households feel more secure with their financial position and household savings tend to decrease which lifts consumer spending. When wealth decreases, households feel less secure which leads to an increase in savings and decline in spending. However, this relationship does not always work. Most recently in the pandemic, household wealth rose in 2021/22 alongside the lift in home prices but the savings ratio also surged thanks to government driven stimulus cheques. Since then, the household savings ratio has been falling but growth in total consumer spending has been low. We expect that the household savings rate will continue to fall in 2024 as it normalises after the pandemic but growth in consumer spending will still be low.

Implications for investors

Households dealt with a cost of living challenge in 2023 because of high inflation and rising interest rates. Inflation is expected to slow in 2024 and we expect the RBA to start cutting interest rates by mid year which should ease the repayment burden for households with a mortgage, as mortgage interest repayments as a share of income are rising to a record high (see the chart below).

Source: ABS, AMP

So, while cost of living issues should improve for consumers, household wealth will come under pressure in 2024 as we expect home prices will decline by 3.0% to 5%. This is likely to occur alongside a slowing in household incomes as the labour market weakens and the unemployment rate increases. This environment is expected to be negative for consumer spending and GDP growth. We see GDP growth rising by 1.2% over the year to June 2024, below the RBA’s forecast of 1.8% and anticipate the unemployment rate to increase to 4.5% by mid year. This should see the RBA cutting interest rates by June and we expect a total of 3 rate cuts in 2024.

Wealth inequality between households is also an issue in Australia. The top 20% of households (by income quintile) owned 63% of total household wealth in 2019-20 but the bottom income quintile (the bottom 20%) owned less than 1.0% of all household wealth. In Australia, there is also increasing generational wealth gap, with wealth across older households increasing significantly over recent decades but this has not been the case for younger Australians. There are numerous government policies that could address these issues of wealth inequality, including improving the housing affordability issue (through lifting housing supply and/or looking at the favourable treatment of housing investment) and doing a tax review (looking at broadening the GST and examining the merits of a wealth or death tax), which could help the wealth inequality issue.

Source: AMP

As scams evolve, so can you

By Robert Wright /February 16,2024/

As scams continue to evolve, it’s important to stay on top of the latest information.

Here are some tips for staying protected against some of the most common scams impacting Australians today and red flags to watch out for.

What can you do to stay protected?

Anyone can fall victim to a scam. As well as learning more about the different types of scams and how to spot them, start a conversation with family members or friends. You might know the red flags to watch out for, but do your loved ones? Raising awareness and educating yourself and others are important steps to help combat scams and even prevent them from happening in the first place.

Three scams to watch out for

Impersonation scams

Have you ever received a call and it just didn’t feel right? It may have been part of an impersonation scam, which is when a scammer impersonates a bank or other service company by phone or SMS, asking you to authorise transactions, make a payment, or provide personal information.

According to the Australian Government’s Anti-Scam Centre, three in four reported scams include some form of impersonation of a legitimate entity1.

So how can you be sure next time that person calling you is really from where they say they’re from? Here’s a few things to remember:

- most financial institutions will never ask you to transfer funds to another account

- never share passwords with anyone

- avoid using phone numbers or links from text messages

- check contact information using a trusted source such as the company’s website.

Investment scams

As of 9 November 2023, Australians have lost $240 million to investment scams2. Investment scams are often sophisticated which means they can be hard to spot. Investment opportunities offering fast results and big returns can have the potential makings of a scam.

Common investment scams include:

- unsolicited investment offers such as cryptocurrency, fake corporate or treasury bonds, and fake share IPOs (Initial Public Offerings), claiming to be from reputable businesses

- fake endorsement of an investment or other business opportunities from celebrities

- early access to superannuation with a fee.

Buyer/seller scams

Buying or selling on an online selling platform is great when it’s quick and hassle-free. But scammers are popping up everywhere, so it’s harder to stay safe online. Here are five red flags to look out for:

- being approached by someone who has no profile photo

- the price seems too good to be true

- a request for personal information such as your phone number or email

- the buyer overpays for an item and wants you to refund the excess amount

- the buyer wants to pay using a gift card or wants to send a prepaid shipping label.

1scamwatch.gov.au

2scamwatch.gov.au as at 9 November 2023

Source: Macquarie