Tag Archives: Investment Property

Reserve Bank cuts interest rates by 0.25 percentage points in August in unanimous decision

By Robert Wright /August 22,2025/

In short:

The Reserve Bank cut interest rates by 0.25 percentage points in August to 3.6 per cent, after July’s shock ‘on hold’ decision.

The average owner-occupier with a $750,000 mortgage as of February will see their minimum monthly repayment fall $111 if their bank passes on the cut, taking the cumulative reduction this year to $340, according to Canstar.

What’s next?

The next RBA rates decision will be delivered on September 30. After that, there are two further meetings this year, in November and December.

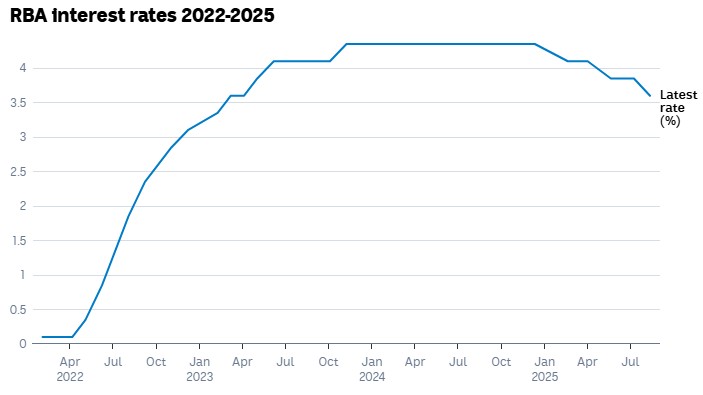

The Reserve Bank has delivered its third interest rate cut of 2025, with a 0.25 percentage point reduction at its August board meeting.

That takes the cash rate to 3.6 per cent for the first time since April 2023.

The move had been overwhelmingly anticipated by financial markets and economists after the surprise decision to hold rates steady in July.

It was a unanimous decision by board, which had been divided last month.

Tuesday’s cut follows a further easing of inflation in the June quarter, which RBA governor Michele Bullock last month highlighted as the crucial piece of data the monetary policy board was waiting for.

“Updated staff forecasts for the August meeting suggest that underlying inflation will continue to moderate to around the midpoint of the 2–3 per cent range, with the cash rate assumed to follow a gradual easing path”, the post-meeting statement read.

ABC News / Source: Reserve Bank of Australia

The inflation pull back, alongside “labour market conditions easing slightly, as expected”, led the board to deem “further easing of monetary policy was appropriate”.

“This takes the decline in the cash rate since the beginning of the year to 75 basis points”, the RBA board noted in its statement.

The central bank cut interest rates at its February and May board meetings.

Before that, the RBA’s cash rate had sat at 4.35 per cent since November 2023, after a series of 13 rate hikes, beginning in May 2022.

Treasurer Jim Chalmers described it as a “very welcome relief for millions of Australians”.

“It means the lowest interest rates for more than two years”, he said shortly after the decision.

“It reflects the substantial and sustained progress we’ve made on inflation in a volatile and uncertain global environment”, the treasurer noted in a statement.

Cash rate at 3.6pc, further rate cuts expected

The Australian dollar fell following the decision, dipping just below 65 US cents as Ms Bullock addressed a media conference in Sydney.

The RBA governor indicated the board was prepared to cut interest rates further if necessary.

“The forecasts imply that the cash rate might need to be a bit lower than it is today to keep inflation low and stable, and employment growing, but there is still a lot of uncertainty”, Ms Bullock told reporters.

“The board will continue to focus on the data to guide its policy response”.

Where are rates heading?

The Reserve Bank’s economic outlook suggests further room to cut interest rates, but it’s not all good news for most working-age Australians.

Betashares chief economist, David Bassanese has forecast further interest rate cuts, with the next easing more likely in November, rather than at the next meeting in September.

“Indeed, the [central] bank’s own forecasts of underlying inflation stabilising at 2.6 per cent over coming quarters incorporate further declines in the cash rate in line with current market expectations”, he wrote.

“That said, barring a major growth scare, the RBA does not seem in any rush to cut interest rates.

“All up, my base case remains that a rate cut on Melbourne Cup day is an odds on favourite –following release of the June quarter consumer price index report in late October”.

The governor would not be drawn on what specific cash rate the central bank considers to be “neutral” – that is, the level where the rate is not stimulating or putting a handbrake on the economy.

Instead, she gave a “very wide range” of between 1 and 4 per cent, and noted a neutral rate is for when there is an absence of economic shocks.

“We are very often not in the absence of shocks … we’ve got shocks, particularly at the moment”.

While the central bank’s forecasts put inflation around target over the period ahead, it has downgraded its growth forecasts.

It now expects gross domestic product (GDP) expanded 1.6 per cent over the year to June (compared to 1.8 per cent forecast in May); and GDP growth to only pick up to 1.7 per cent by the end of the year (it had previously forecast 2.1 per cent).

“Its forecasts assume that the cash rate will continue to ‘follow a gradual easing path’, implying that without further easing growth and inflation will be lower and unemployment higher”, AMP chief economist, Shane Oliver said.

AMP has forecast further rate cuts in November, February and May to take the cash rate to 2.85 per cent.

“We continue to see further rate cuts as growth remains sub par, the risks to unemployment are on the upside, underlying inflation is likely to remain around the 2.5 per cent target and monetary policy remains tight”, Dr Oliver wrote.

How much will home loan repayments fall?

Some lenders were quick off the mark to confirm they would be passing on the interest rate cut to home loan customers, with Macquarie, Commonwealth Bank, Westpac, ANZ, NAB and AMP among the first handful of announcements.

The cumulative effect of three rate cuts so far this year have added up to a substantial reduction in minimum mortgage repayments for many home loan borrowers.

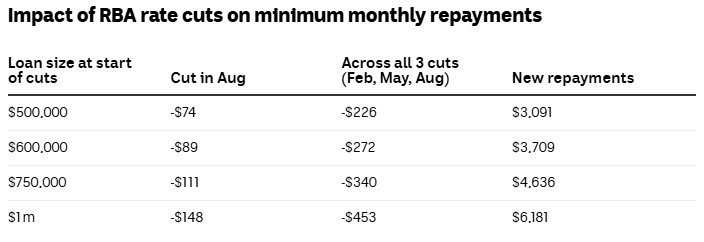

According to calculations by financial comparison site Canstar, the savings from this month’s cut range from $74 on a half a million dollar mortgage, to $148 on a $1 million home loan.

Based on an owner-occupier paying principal and interest with 25 years remaining in Feb 2025 at the RBA average existing customer variable rate. Calculations assume the banks pass on each cut in full to existing variable customers the month after.

Source: Canstar.com.au

The numbers are based on an owner-occupier repaying principal and interest, who had 25 years remaining on their loan in February.

The estimates assume borrowers were paying the average variable rate of 5.79 per cent, which would fall to 5.54 per cent after Tuesday’s 0.25 percentage point cut, and that lenders pass on cuts in full to existing variable customers the following month.

Home loan borrowers are not obliged to lower repayments, and, in fact, most do not – last month, Commonwealth Bank released data showing only one in 10 eligible home loan customers reduced their mortgage direct debits after the rate cut in May.

If borrowers continue to make repayments above the minimum required, they will pay down more of the principal as the interest reduces, and pay off their loan faster.

Source: ABC News

Your guide to gearing

By Robert Wright /August 21,2023/

There are a number of considerations when it comes to gearing, the investment assets you may choose to gear and the way you structure your debt.

A gearing strategy can be set at three levels:

- Positive gearing – where income from the investment exceeds the interest payable on the loan.

- Neutral gearing – where income from the investment is equal to the interest payable on the loan.

- Negative gearing – where the income from the investment is less than the interest payable on the loan. The excess interest expense is an allowable deduction against other assessable income, which for a taxpayer on the top marginal rate is currently worth 47% (inclusive of the Medicare levy).

Investing in growth assets such as shares or property using borrowed funds can be one of the most effective ways to accumulate wealth over the long term.

Investors are solely relying on a future capital gain when undertaking a negative or neutral gearing strategy. Negative gearing is tax effective in that the interest expense is fully deductible against the income generated by the geared investment and other assessable income. There are also other tax breaks such as the deductibility of depreciation (for property) and franking credits (for shares) to help subsidise the cost of the investment. In addition, for individuals, 50% of any capital gain is exempt from tax where the investment is held for at least 12 months.

Examples

Positive gearing strategy

If $100,000 were invested for a year in assets that produced a return on investment of 10% per annum, the total return on investment would be $10,000.

If the investor had also used a gearing strategy and borrowed $50,000 (at a cost of 7% per annum) and invested this in the same assets producing the same 10% per annum return, the return on investment would be 10%, less the cost of finance (7%) – that is, a net additional return of $1,500 using someone else’s money.

The net return can be greater than this when the tax deductibility of interest is taken into consideration.

The below examples of negative gearing illustrate how the negative cash flow from the investment can be offset by the deductibility of interest plus other tax breaks.

Negative gearing an investment property

Sarah earns a salary of $200,000 and borrows $400,000 to buy an investment property. The property generates rental income of $20,000 per annum while interest expense on the loan (interest only with no principal repayments) is 7% or $28,000 per annum. In addition to the deductible interest expense, there are the following ‘non-cash’ deductions:

- $2,500 depreciation

- $4,500 building amortisation (2.5% based on a construction cost of $180,000)

| Financial position | Without negative gearing strategy | With negative gearing strategy |

| Salary | $200,000 | $200,000 |

| Rental income | – | $20,000 |

| Non-cash property deductions | – | $7,000 |

| Interest expense | – | $28,000 |

| Taxable income | $200,000 | $185,000 |

| Tax payable (incl. Medicare levy) | $64,667 | $57,617 |

| Net cash | $135,333 | $134,383 |

The difference in cash flow of only $950 has been assisted by the $7,000 tax deduction for the non-cash depreciation and building amortisation expenses.

These examples demonstrate the worth of tax deductions to an individual on the top marginal tax rate in the first year of a negative gearing strategy. Over time, negatively geared investments can become positively geared – especially when rental income or dividends are reinvested.

Couples with one person on a higher marginal tax rate than the other, should carefully consider who should be the borrower and owner of investments over the long term. While initially it may be tax effective to have a negatively geared investment in the name of the person with the highest tax rate, if it’s expected to become positively geared in the future, it may be more effective to have the loan and investment in the name of the person with the lower marginal tax rate from the outset. Especially when you consider the potential capital gains tax, stamp duty and loans fees that might be incurred in transferring the investment and loan.

Trusts and companies can also negatively gear investments, however the following should be considered:

- Trusts and companies cannot distribute losses, they need to be carried forward and offset against future assessable income.

- While the company tax rate is 30% for companies that are not base-rate entities which have a tax rate of 25%, companies are fully assessed on capital gains as opposed to the 50% discount applied to assets held for 12 months or more by individuals and trusts.

Negative gearing a share portfolio

Sarah earns a salary of $200,000 and borrows $400,000 to invest in a share portfolio. The share portfolio generates a dividend yield of 4% fully franked, while the interest expense on the loan (interest only loan) is 7% per annum under a line of credit secured against her home.

The below table illustrates the impact the negative gearing strategy has on Sarah’s cash flow.

| Financial position | Without negative gearing strategy | With negative gearing strategy |

| Salary | $200,000 | $200,000 |

| Dividend | – | $16,000 |

| Imputation gross up | – | $6,857 |

| Interest expense | – | $28,000 |

| Taxable income | $200,000 | $194,857 |

| Tax payable (incl. Medicare levy) | $64,667 | $62,250 |

| Franking credit | – | $6,857 |

| Tax payable (incl. Medicare levy) and after franking credit | $64,667 | $55,393 |

| Net cash | $135,333 | $132,607 |

The difference in cash flow is $2,726 which is approximately 0.7% of the investment portfolio. Sarah hopes that her after-tax capital gain will be greater than this cash flow loss.

Source: BT

Property investment vs shares

By Robert Wright /February 18,2021/

An age-old question is whether it’s better to invest in property or shares. There is actually no right or wrong answer. It all comes down to your preferences and approach to risk.

Growth investments

Both asset classes – shares and property – are considered to be growth investments. In other words, over time, a quality investment in shares or a property could generate capital growth and also produce income from rent (property) and dividends (shares).

The case for shares

Ease of entry into the share market is a big plus for share or equity investors. You can buy into the share market with as little as a few hundred dollars. In comparison, home and apartment prices in our capital cities could easily cost upwards of $1 million. The transaction costs of investing in shares such as brokerage and transaction fees are also significantly lower than the stamp duty and legal fees you pay as a property investor.

Finally, with a share market investment, you could get almost instant access to your money when you decide to sell. Equally, you don’t have to sell the entire investment to get access to some cash. With an investment property, you can’t sell a bedroom to free up some cash – it’s the entire property that goes to market or nothing.

The case of property

A major appeal of owning a property is its perceived stability relative to the share market, where values can vary from day-to-day as a consequence of how easy it is to buy and sell shares. If you’re approaching retirement, this level of volatility may not be for you.

A property investment, on the other hand, gives you a tangible asset that can deliver a sense of investment security as well as some capital growth and income.

Property buyers have the ability to fix the interest rate of a loan, which is another valuable security measure. This means your mortgage repayments will be set for an amount of time, which could be a good option for someone who prefers stability.

Holding an investment property in a self-managed super fund (SMSF)

It is possible to set up an SMSF primarily to invest in property, but be aware, some rules apply to ensure your fund remains compliant. ASIC’s Money Smart website lists the following rules:

- The property must meet the ‘sole purpose test’ of solely providing retirement benefits to fund members.

- The investment property can’t be acquired from a member or related party of a member of the SMSF.

- The property can’t be occupied by a fund member or any fund members’ related parties.

- The property must not be rented by a fund member or any of the fund members’ related parties.

As this shows, there are many reasons to invest in shares and property. For further information about investing in property or shares, or to discuss whether it may be a suitable strategy for you, please get in touch.

Source: BT