Tag Archives: Investments

Protecting your money – Cybersecurity and scam awareness

By Robert Wright /November 21,2025/

Your super and investment savings represent years of hard work for a secure future. Unfortunately, they can be a prime target for scammers, causing significant financial loss and emotional distress.

Financial scams are on the rise and becoming more sophisticated, making them harder to detect. This article will help you recognise common types of super and investment scams, how to identify them and how to protect yourself and your loved ones.

Super scams

These scams usually involve individuals or companies pretending to be from a super fund or regulatory body seeking your personal information. They may claim they need it to update your super account or verify your identity. Or they could offer to help you access your super before you’re eligible to under law. They may claim that doing this can, for example, help you pay off debts or purchase a house. But accessing your super early can result in significant penalties. In addition, these scams may involve high fees or charges which can eat into your super savings.

We recommend that:

- You never give out your personal information unless you’re sure it’s safe.

- You’re aware of the conditions of release to withdraw your super.

Given the variety of scams out there, following these four steps can help prevent you falling victim.

Stop

If you receive a suspicious call, email or text, pause and assess. Genuine organisations never pressure you to act immediately or ask for your password via email.

Reflect

Be careful about sharing personal information online. Scammers piece together details from various sources to exploit or create accounts in your name. Always reflect.

Protect

Whether it’s personal or work, staying vigilant is crucial. When in doubt, reject contact, delete suspicious messages and avoid opening unknown links.

Report

If you receive a suspicious email, do not click on any links or attachments or provide any information. If you receive a suspicious email, you can report it to the Australian Cyber Security Centre (ACSC).

Amy’s story: a crypto cautionary tale

Amy, intrigued by a cryptocurrency investment promising high returns using her super, fell victim to a scam that led to the loss of her savings and her involvement in criminal activity.

Her story highlights the dangers of crypto scams. It will help you to recognise and avoid such fraudulent schemes and the potential consequences, including financial loss and legal repercussions that victims may face.

Amy was contacted by a man named Michael via Facebook. He was promoting a cryptocurrency investment business promising amazing returns that didn’t require an initial deposit from her bank account but rather from her superannuation.

A complex scheme

Intrigued by this, Amy engaged in further conversation with Michael. He walked her through the steps of setting up a legitimate Self Managed Super Fund (SMSF), allowing Amy to take the funds she had invested with her existing super fund and place them into a bank account, which was then invested into a fake crypto wallet/fake investment website.

As time went on, Amy would check her balance on what she believed was a genuine trading platform – it showed significant growth, her initial $30,000 deposit soaring to over $170,000. However, after hearing about instability in the crypto markets, Amy decided that it might be time to withdraw some of her profits. Amy contacted the crypto business, which advised that she would need to pay an upfront sum of $4,500 to cover taxes – funds that Amy didn’t have readily available.

Amy reached out to Michael and explained that she wanted to withdraw some of her money from her crypto investment but couldn’t afford to pay the upfront lump sum tax. Michael explained if Amy agreed to open a number of bank accounts and handle some fund transfers on his behalf that would “help to grow the Australian business”, she would be able to earn a 5% commission on each amount transferred and accumulate enough money to pay the lump sum tax.

Amy agreed to the arrangement and funds began being transferred into the bank accounts Amy had opened. Michael would call Amy and request her to “transfer $x into the crypto wallet, then purchase this specific crypto coin”. The crypto wallet would then be emptied by Michael/Crypto Investments.

How did the scam work?

Amy unknowingly fell for a crypto investment scam. Michael convinced her to open an SMSF, allowing her to access funds that were meant to be preserved until retirement. The fake crypto platform showed huge growth, giving Amy confidence in the investment and making her feel good about the nest egg she believed was growing. By quoting her high upfront costs to access the funds, Michael manipulated her into becoming an unwitting money mule, engaging in money laundering and helping the scammers deceive other unsuspecting people out of their funds.

Unfortunately, Amy has not only lost her super but has also become involved in criminal activity. The matter is now with the police and Amy faces possible prosecution for money laundering offences.

Source: MLC

The absurdity and calamity of US tariff policies

By Robert Wright /May 23,2025/

US tariffs are poorly designed, badly implemented and are already damaging both the US and global economies. The economic damage will only get worse as uncertainty further undermines business and consumer confidence and results in dislocation of global supply chains.

Determining the extent of economic damage, and financial market implications, is difficult because we don’t know what tariffs will actually be implemented or how many backflips there are before then. There’s no clear, defining strategy. The justification for tariffs oscillates between reinvigorating US manufacturing, raising revenue to fund tax cuts, the cost of the US providing global security, the provision of the US dollar to support global trade and financial markets, and broadly addressing an ‘unfair’ trading system. Different justifications would lead to different structures of the tariff regime. Adding to uncertainty, key individuals in the administration have different goals for tariffs.

- The obsession with bilateral trade deficits is baseless

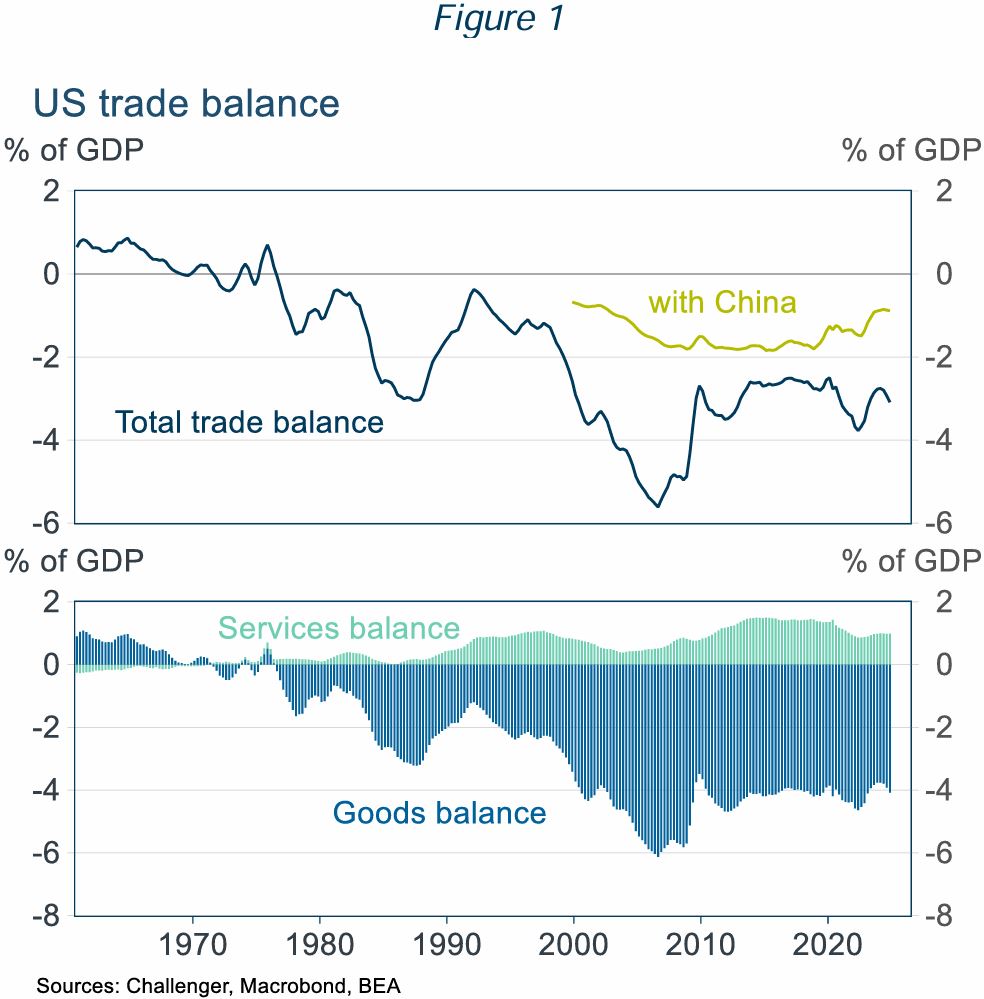

President Trump’s tariff obsession is rooted in a dislike of trade deficits. The United States has run a trade deficit since the mid-1970s (Figure 1). He attributes this deficit to unfair trade policies in other countries and an overvalued US dollar, resulting from US dollar demand given its role in international trade and finance. But the trade deficit also depends on US domestic conditions, notably the US Government’s huge fiscal deficit, currently 5% of GDP.

Balanced national trade doesn’t need bilateral balanced trade

Even if balanced trade at the country level was desirable, there is no reason for this to apply country by country. Even countries with balanced aggregate trade run large trade deficits or surpluses with almost all of their trading partners: Belgium had balanced trade with just two countries; and Canada, Finland, South Korea and South Africa each had balanced trade with just one of their trading partners. Each of these five countries had significant bilateral trade surpluses or deficits with over 150 of their trading partners. The US goal of balanced bilateral trade with every country is, frankly, bonkers.

- The calculation of tariff rates is absurd

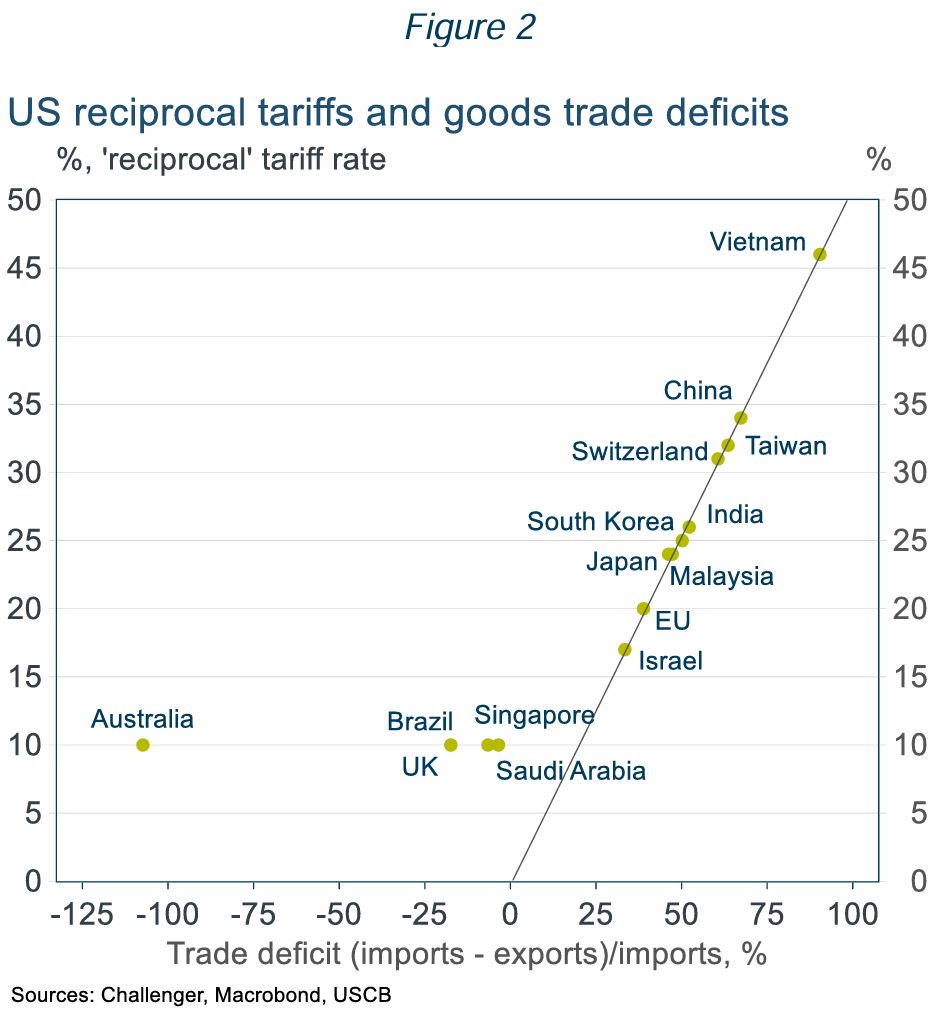

- Bilateral trade balances are meaningless but determine the US ‘reciprocal tariffs’ (Figure 2).

- Even countries the US has a trade surplus with, including Australia get a 10% tariff. If Australia applied the same logic as the US, we’d impose a tariff on the US of around 50%.

- The US has a surplus in services trade of 0.25% of GDP (partly offsetting the goods trade deficit of 1% of GDP; Figure 1) but ignores services trade in its calculation of tariffs.

- The tariffs are badly designed reflecting unclear and inconsistent goals

The US tariff regime has a mix of tariffs on specific goods (steel, aluminium, vehicles) and on specific countries (Canada, Mexico, China and the reciprocal tariffs) reflecting the varied goals of the tariffs. But many of these goals are in conflict. If, as Trump claims, tariffs raise revenue without increasing US prices by forcing foreign suppliers to absorb the tariff, then US manufacturers won’t be more competitive as US prices won’t be higher. And if tariffs are successful in boosting US production, then there would be fewer imports, and so less tariff revenue.

Several bad design elements of the tariffs mean there will be further changes:

- Different tariff rates distort trade for little benefit – for example, Apple intends to ship iPhones to the US from India rather than China as US produced iPhones would be prohibitively expensive.

- High tariffs are being applied to goods the US can’t, or won’t, ever produce – for example, some minerals and shoes (most come from China and Vietnam with 145% and 46% tariffs).

- Tariffs are being applied to inputs used by US manufacturers, increasing exporters’ costs.

- The effective trade embargo with China will be disruptive to the US economy

The 145% punitive tariff applied to China makes most imports from China prohibitively expensive. But the US economy is not ready to disengage from China, which has supplied 13% of US imports. Factories don’t pop up overnight.

Using a fine disaggregation, breaking down goods into their constituent parts, over half of US imports are from China. Alternative suppliers just don’t exist.

For finished consumer goods with very high import shares from China, large price increases and stock shortages will be disruptive to consumers and impact consumer sentiment and support for tariffs. The economic impact will be even greater for those imports predominantly sourced from China that are used as inputs in US production, such as explosives, machinery and various chemicals. For example, China is also a key source for base ingredients used in manufacturing medicines and finished medicines.

- The tariff regime won’t survive its poor design, but tariffs won’t go away completely

The US tariff regime is already unravelling with holes poked in the tariff wall.

- Reciprocal tariffs were paused until 9 July (the baseline 10% tariff still applies to all countries).

- Consumer frustration will mount facing higher prices and product shortages. For example, phones, computers and some other electronics have been exempted from the China tariffs.

- Businesses are getting traction lobbying on the cost to production from tariffs, for example there will be a partial rebate on the 25% tariffs on car parts used as inputs in US manufacturing.

- The US has said some 70 countries want to negotiate tariff reductions. Yet negotiating a detailed trade agreement takes time. The renegotiation of the US-Canada-Mexico trade agreement in President Trump’s first term took 18 months. A rushed negotiation will contain flaws.

However, President Trump strongly believes in the benefits of tariffs for promoting US manufacturing and he needs the revenue. He has committed to using tariffs to reduce income taxes, even musing that income taxes could be eradicated. But a 10% uniform tariff has been estimated to raise just $1.7 trillion over 10 years, a 20% tariff $2.6 trillion. This is substantially less than the estimated cost of $5 to 11 trillion of the tax cuts already promised by President Trump.

- What does the future hold?

There will be many more turns in the road with backflips, reduced tariffs for goods the US won’t produce or needs and new tariffs. There will be ‘deals’ reducing (but not eliminating) individual tariffs with countries committing to reduce trade barriers and import US goods (much of which will never happen).

The pause in reciprocal tariffs, after just one week, was reportedly triggered by the turmoil in bond markets which could have precipitated a financial crisis. Trump has displayed greater resolve in the face of the large fall in equity prices than in his first term. But the risk of a financial crisis, or severe recession, and sharp falls in approval ratings are likely to remain red lines that would result in some pullback.

Challenger expects ongoing tariff uncertainty and hence further volatility in markets. Aggregate tariffs will never get to the levels initially announced, but they will also be much higher than before, reducing US and global growth. Tariffs will add to US inflation, reducing the ability of the Fed to ease. Market pricing is for almost 100 basis points of cuts this year, but there’s a good chance the Fed does not even cut this year.

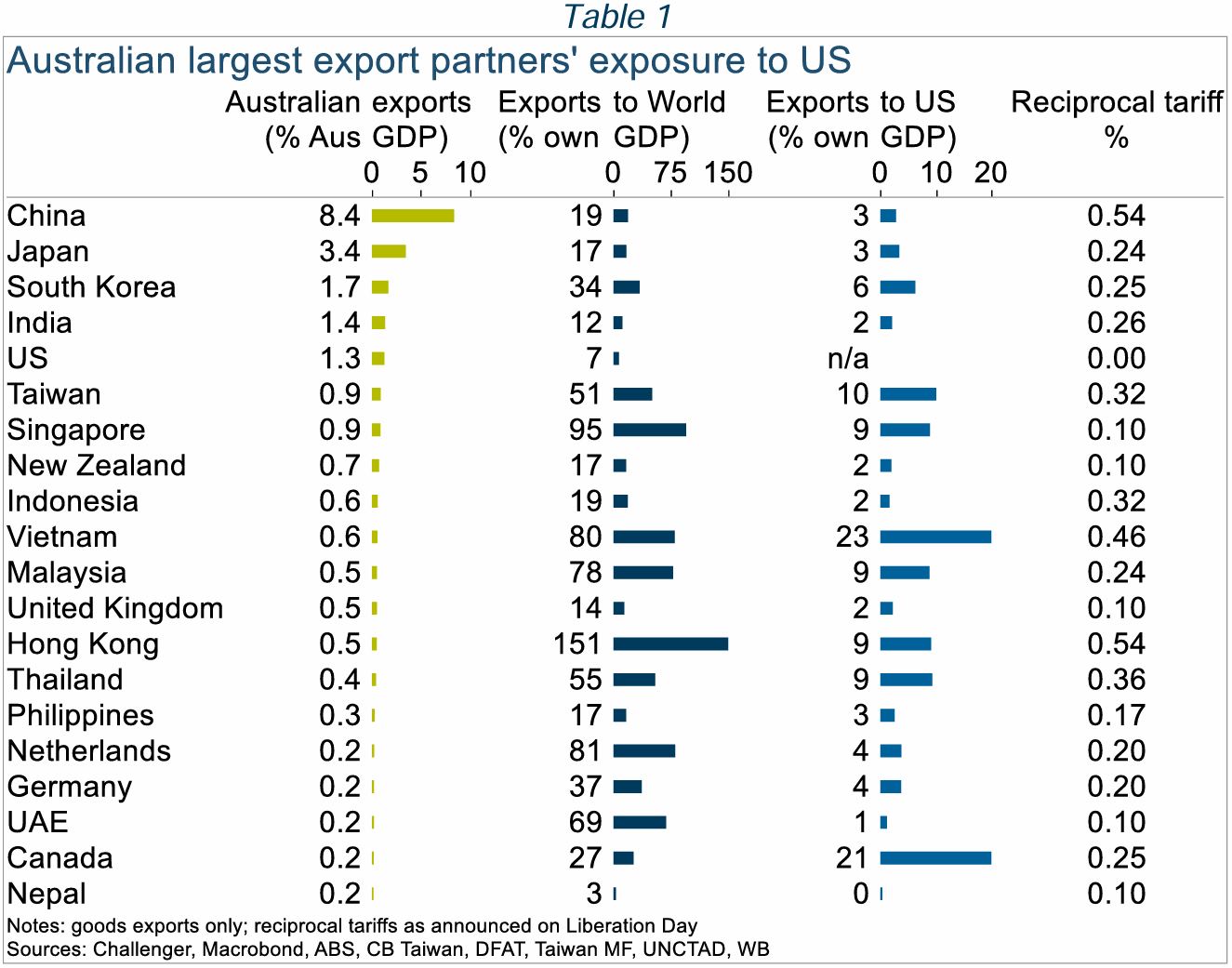

Australia will also see slower growth. We have limited direct exposure to the US economy, but our largest trading partners are more exposed (Table 1). The IMF downgraded its GDP growth forecasts for 2025 by 0.5%. Slower growth, and China’s surplus manufacturing capacity reducing Australian import prices, will lower inflation opening the path to RBA rate cuts. However, market pricing for a cash rate below 3% by December is overdone. With the worst case for US tariffs unlikely to play out, three cuts bringing the cash rate to 3.35%, around its neutral level, seems more likely.

Source: Challenger

Megatrends for 2025 and beyond…

By Robert Wright /February 28,2025/

Megatrends are long-term structural changes that affect the world we live in. Importantly, they shape communities but they also create investment opportunities and risks. Learnings from historical megatrends include: 1) they often solve a problem through innovation; 2) the scope of the megatrend can initially be underestimated; and 3) the duration of a megatrend is typically longer than anticipated. There are numerous megatrends likely to influence markets that investors should consider: the shift to the cloud and generative AI, the ageing population, rising geopolitical tensions and so on. Today we highlight just some of the current megatrends.

The continued growth in “winners take all” dynamics

A megatrend that continues to play out is growth in “winner take all” or at least “winner takes most” dynamics in the global economy. Reduced cross-border frictions, the growth in digital goods and distribution channels, and the increasing importance of scale and network effects have allowed companies to scale to a size almost unimaginable in the past.

The rise of the so called “magnificent seven”, the group of leading US technology companies, is a good example of these forces playing out. This group now accounts for a higher share of global markets than the leading companies of the tech bubble era of the early 2000s. However, unlike that time, their size today has predominantly been fuelled by enormous growth in revenues and profitability, albeit some speculative elements may have played a part more recently.

A key risk for some of these businesses is antitrust. Microsoft, Apple and Alphabet have recently attracted the attention of the antitrust authorities, with increased competition the primary motive. We view that it is a low probability that regulators break up these businesses, meaning the underlying economic forces will continue to allow successful businesses to scale far more quickly and to far larger sizes than historically was the case. This presents a significant opportunity for global investors, as these companies can deliver outsized returns. On the other hand, these trends also increase disruption risks to legacy businesses and industries.

To benefit from the former and guard against the latter, investors should focus on quality companies that have strong and enduring competitive advantages. These advantages typically include scale, pricing power, brand strength, network effects and intellectual property.

Glucagon-like peptide-1s (GLP-1s) and solving obesity

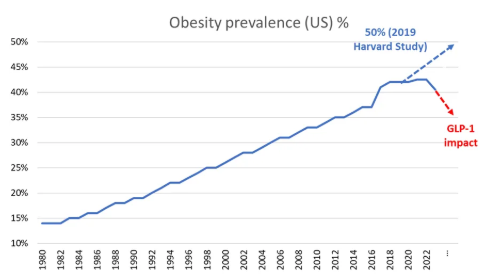

One of the biggest health issues facing developed countries is obesity. The development of the GLP-1 class of weight loss drugs such as Ozempic promises to transform the treatment of obesity and significantly improve health outcomes for societies. GLP-1s stimulate the brain to reduce hunger and act on the stomach to delay emptying, so you feel fuller for longer, have a lower calorie intake and lose weight.

Take up is likely to be strong over coming years as supply constraints ease and continued innovation delivers a more convenient oral pill and mitigates potential side effects such as nausea. Growing clinical evidence of health benefits, such as lower risk of heart problems, will also encourage governments and insurers to cover the cost of the drugs. These developments have dramatically changed the outlook for obesity, with the US recording its first fall in obesity rates since at least the 1970s, a dramatic turnaround from predictions of just a few years ago.

Source: CDC, OECD, WHO, IHME, Harvard

The development also has some significant investment implications. Most obvious are the potential investment opportunities in the drug manufacturers, although given high expectations we need to carefully monitor scientific developments and the pricing environment. There are also several investment risks to consider, with the potential for lower demand for certain medical device companies, food manufacturers and quick service restaurants.

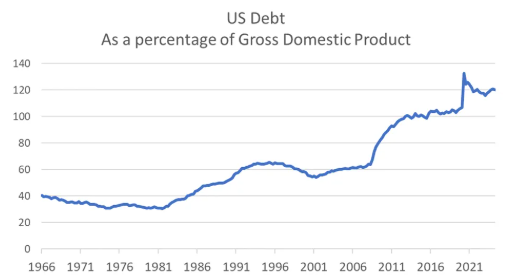

The unrelenting rise in sovereign debt

Not all megatrends are positive for investors; one megatrend to be wary of is rising sovereign debt. In many parts of the world fiscal responsibility is no longer a priority as governments focus on more immediate issues and winning elections. In the US the national debt has been rising since the 1980s. In 2010, following the government’s response to the Global Financial Crisis, it first exceeded 90% as a percentage of GDP – the level identified by academics Reinhart and Rogoff as associated with a worsening in growth outcomes. A further spending binge during the 2020 COVID pandemic has resulted in the US national debt rising to more than 120% of GDP.

Source: Federal Reserve Economic Data

With the US Federal budget deficit expected to hit $1.8 trillion in 2024 and both parties promising billions more in spending, debt is likely to continue to build. US national debt has not been a major issue for markets to date, but the risk of a debt crisis, accompanied by rising bond yields and volatile markets, increases as debt levels continue to rise. Many other countries are in a similar position, with debt to GDP exceeding 100% in the UK, France, Spain, Italy and Japan. Australia is relatively well placed with the national debt at 38% of GDP.

What does this mean for investors? Governments have three ways to “solve” excessive national debt: (1) austerity – cutting spending and raising taxes; (2) default; or (3) financial repression – printing money to inflate the problem away. The first is politically unpalatable and appears unlikely, the second would be an outright disaster and can be avoided by countries that issue debt in their own currency such as the US. Thus, the most likely outcome is money printing, or central bank financing of budget deficits in more technical terms, resulting in a period of structurally higher inflation.

While it’s impossible to be precise in terms of the timing of a potential debt crisis, investors can seek to protect themselves by investing in real assets, such as property and equities, with a focus on high quality companies with pricing power that can protect investors in times of high inflation.

These are just a few of the megatrends shaping markets today and in the future. As investors, a long-term focus and active management are key to both taking advantage of the opportunities these trends provide and avoiding risks that may arise.

Source: Magellan

The ins and outs of geared share funds

By Robert Wright /February 28,2025/

Geared share funds are high risk and high reward. When share markets are doing well, the returns can be very high, but the opposite is also true. We look at the pros and cons, and the role of geared share funds in a diversified investment strategy.

Geared share funds can be a great way for investors to invest in shares – and share in the rewards – when the share market performs well over long periods of time.

Geared share funds magnify both positive and negative returns, so they’re considered high risk, high return investment options.

But exactly what is a geared share fund, and are they for everyone?

Let’s take a look at the ins and outs of this unique investment option.

What is a geared share fund?

Geared share funds accept money from investors and borrow money to invest alongside investors’ capital. The fund uses the pool of investors’ money and borrowed money to buy shares.

They amplify both positive returns and negative returns on the shares in which the fund invests.

On the upside, geared share funds generate higher returns than overall share market returns when markets are rising. Conversely, the value of your investment will drop further than equivalent investment options without internal gearing.

They are best explored as part of a long term, diversified investment strategy.

How do geared share funds work?

When you invest money in a geared share fund, the fund will borrow money to invest on your behalf, alongside your investment.

For example, for every $1,000 you invest in the fund, the geared share fund may borrow another $1,000. That would give you $2,000 of exposure to the shares in which the fund invests. So in addition to the returns generated from your capital, you also receive all the returns from the borrowed funds (less the cost of borrowing).

The fund’s gearing, or borrowing, effectively magnifies the returns of the underlying investments, whether they are gains or losses.

Geared share funds generally perform well when the share market is growing at a higher rate than the interest charged on borrowed money.

Geared share funds borrow at institutional interest rates, which are generally lower than those offered to individual investors.

Pros of geared share funds

- The gearing, or borrowing, is done within the fund: unlike a margin loan, the fund, rather than the investor, is responsible for repaying its loans. This model allows investors to keep a long term view on their investments, rather than worry about day to day performance of their investments.

- Investor exposure is limited to their invested capital: while the fund borrows on behalf of its investors to buy shares, if the share market falls, and the fund’s loans need to be repaid, individual investors will never lose more than their invested capital.

- Gains are magnified by gearing: when the shares in which the fund invests go up, the return to the investor may be much higher than if they had simply purchased an equivalent fund without gearing.

- Franking credits are magnified by gearing: when a geared fund invests in Australian shares, the gearing will also magnify the level of franking credits payable as part of income distributions.

- Long term gains magnify long term share performance: investors seeking to invest for a decade or more, and who are willing to ride out short term market falls, can do very well with geared share funds. The compounding effect of the additional returns from gearing is very powerful over the long term.

Cons of geared share funds

- Fees are relatively high: fees are charged not just on the $1,000 you invest, but also on the $1,000 that the fund borrows on your behalf. Fees reduce your return.

- Losses are magnified by gearing: when the shares in which the fund invests go down, losses will be much higher than if you simply purchased the same shares with the same initial investment.

- Short term share market falls can lead to big investment losses: investors who need to take out their capital at a particular point in time, or who are not prepared to wait for markets to recover, can suffer big losses if this coincides with a fall in markets.

When to consider geared share funds

Geared funds can play an important role within a diversified portfolio for investors looking for above average investment performance over the long term by accelerating their Australian and/or global share allocations.

Investors who can ride out short term market volatility and do not need to take out their money in the short term, may benefit from the long term returns that geared share funds can offer. Geared funds should therefore be particularly attractive to superannuation investors who cannot access their capital until retirement.

Investors who are risk averse and who may need to cash in their investment in the short term, may not find geared share funds a suitable investment.

Investors should always seek financial advice to ensure investments are suitable for their objectives, investment horizon, and personal circumstances.

Source: CFS