Tag Archives: Investments

A guide to active and passive investing

By Robert Wright /August 23,2024/

Investment funds can be broadly split into two categories – active and passive. And while both options play a part in an investment portfolio, it’s important to understand how each works before allocating money to them.

Basics of passive investing

Passive investing has gained momentum in Australia, and beyond, over the last decade. It could be because this style of investing aims to replicate the returns of a particular market index (for example, the S&P ASX 200 Index).

This means, that when the value of the index rises, so too will the value of the fund. On the flip side, as the value of the index falls, so too does the nature of the fund.

Exchange Traded Funds (ETFs) are some of the most popular passive investments. They are similar to managed funds, in that they involve a trust structure which holds a basket of securities. As described above, the investments in the fund replicate the makeup of the relevant market index. For example, if the index is made up of stocks that include banks, mining businesses, retail companies and supermarkets, the ETFs will also hold these stocks.

Units in ETFs are listed on stock markets and can be traded just like shares.

It’s important to note, that while there are also actively managed ETFs, passive ETFs are most common of the two.

Basics of active investing

In contrast, an active approach to investing involves a fund manager choosing the assets in the fund, depending on the manager’s view of markets and the type of fund it is.

Like passive investments, there are many types of actively managed funds which offer exposure to different asset classes and industries. Rather than track an index, an active fund will target a return above a particular benchmark. An example of this is, every year, an actively managed fund might aim to achieve the same return as the S&P ASX 200 plus two per cent. Another common way of measuring the performance of an active fund is for it to target a premium above the rate of inflation. For example, a fund might aim to achieve inflation plus two per cent per year.

Cost benefit analysis: fees

Cost is one of the major differences between these two styles of funds. Typically, passive investments are lower cost, as investors are not paying for the fund manager’s expertise in choosing the investments in the fund.

Active funds, on the other hand typically charge a base fee and a performance fee to incentivise the fund manager to produce the highest possible return.

Market conditions

It’s important to remember that markets will always go up and down, and actively managed funds still have many benefits (as well as risks) while factoring:

- Funds that track an index only produce the return of the index.

- Fund manager skills can be used to pick investments that have the potential to do well when economic growth is slow and markets are falling.

- Active managers can also avoid stocks and sectors that are not doing well.

It’s very difficult to get a true picture of whether actively managed funds perform better over time versus passive funds. It’s probably more instructive to think about how each style of investing is used in a portfolio.

Styles applied

A core and satellite approach are a common strategy investors use that involves both active and passive investing. In this approach, the core of the fund tends to be made up of passive investments that follow the market, while the satellite part of the strategy is made up of more specialised investments.

There are a number of ways this style can be applied, but a popular technique is to use index or passive funds as the core, such as an ETFs that tracks one or more major market indices.

The satellites are made up of actively managed funds that allow an investor to express specific views by selecting their asset exposure. For instance, an investor may choose to allocate funds to an actively managed fund that comprises technology investments, in the belief this sector will perform well. Or an investor may choose to apportion funds to an actively managed gold fund, taking the view this commodity may provide a hedge against market volatility.

There are almost endless ways of using actively managed funds to express views about how different asset classes and sectors will perform over time.

A balanced perspective

There’s really no right or wrong approach when it comes to investing in active and passive investments. Many investors choose to invest in a combination of the two styles to achieve a level of diversification in their portfolios and to get access to a broad range of asset classes across the risk spectrum.

Source: BT

What is risk appetite?

By Robert Wright /May 28,2024/

Risk is about tolerating the potential for losses. Understanding your risk appetite allows you to make well informed decisions about your money.

For some people, risk means excitement and opportunity. For others, it invokes feelings of fear and discomfort. We all experience a degree of risk in our everyday lives – whether it’s simply walking down the street or having investments in the share market. Everyone has a risk profile that defines their willingness to accept risk. It’s usually shaped by age, lifestyle and goals and is likely to change over time.

Risk is about tolerating the potential for losses, the ability to withstand market movements and the inability to predict what’s ahead[1]. In financial terms, risk is the chance that an outcome will differ from the expected outcome or return. It includes the possibility of losing some or all of your original investment[2]. Often you may not be aware of your risk appetite until you’re facing a potential loss, so loss aversion becomes a significant factor when making decisions related to risk.

What is risk appetite and risk tolerance?

Risk appetite and risk tolerance are used interchangeably but are different.

Risk appetite is a broad description of the amount of risk an investor is willing to accept to achieve their objectives. It’s a statement or series of statements that describes their attitude towards risk taking[3].

Risk tolerance is the practical application of risk appetite3 and considers the degree of variability in returns an investor is willing to bear.

As an investor, you should have a good understanding of your attitude towards risk. If you take on too much risk, you might panic and sell at a bad time. But if you don’t expose yourself to enough risk, you may be disappointed with your returns and potentially unable achieve your objectives.

How do I work out my risk appetite?

Think about how you might answer these questions:

- How much money do I have to invest?

- How much money am I willing to lose?

- How worried would I be if share markets fell dramatically?

- Am I planning to track your investments daily?

- Would I consider investing in different types of investments?

Your age, income and investment objectives all help determine your risk appetite.

Age: generally younger investors with a longer time horizon to invest are more willing to take greater risk with their money to earn higher potential returns. Older investors with a shorter investment timeframe may be more cautious as they’ll need their money to be more readily available and have less time to recover from a loss.

Income: people who earn more money and have a higher disposable income can typically afford to take greater risks with their investments.

Investment objectives: be clear about why you’re investing and when you think you’ll need to withdraw your money, as well as how long you need the money to last. Saving for a holiday or a deposit on a home is quite different from investing for your retirement.

Risk and Return

The relationship between risk and return underpins all financial decisions. The more risk an investor is willing to take, the greater the potential return. However, investors expect to be compensated for taking on this additional risk and should realise that taking on more risk doesn’t guarantee higher returns.

What type of investor are you?

- High: willing to risk losing more money for the possibility of better returns.

- Moderate: willing to endure short-term loss for the prospect of better long-term growth opportunities.

- Conservative: willing to accept lower returns for a higher degree of liquidity or stability.

Whatever your risk appetite, you should always consider both risk and return before making decisions about what to do with your money. Although shares and property are generally considered to be higher-risk investments, even more conservative investments like bonds can experience short-term losses. No investment is completely risk free.

This explains why smart investors typically have a diversified portfolio that includes several different types of investments.

Risk and Diversification

Don’t think that just because your friends invest in shares you should too. If you don’t have a lot to invest or you’ll want to access your money in a few years, shares may not be the right type of investment for you.

By understanding your risk appetite and being honest about what you want to achieve, you’re more likely to be comfortable with your investment decisions. A financial adviser can help you understand your risk appetite, as well as create a portfolio that suits you.

The simplest way to minimise investment risk is through diversification. A well diversified portfolio will usually include different asset classes, like shares, property, bonds and cash, with exposure across different industries, markets and countries. The idea is to reduce the correlation between the different types of investment and have a good balance of assets which move in different directions and at different times. So, if some of your assets perform poorly, others may be performing well, offsetting the poor performers.

Although diversification doesn’t guarantee you won’t suffer a loss, it’s an effective way to minimise risk and help investors realise their financial goals.

Make informed decisions

You should monitor both your risk appetite and your investment portfolio over time.

Your risk appetite is likely to change as you get older, and as your income or family situation changes.

Similarly, you should review your portfolio to ensure the risk level is still suited to your overall investment objectives. Financial markets are constantly changing, which means the underlying assets you’re invested in could change too.

If you’re a confident investor, you should check that it’s still on track to generate the level of return you want and importantly, at a comfortable level of risk. If you prefer to speak with a financial adviser, they too can help you undertake regular reviews and rebalance your portfolio, as necessary.

By understanding your risk appetite, you’re in a better position to make well informed and transparent financial decisions. It will help you identify opportunities to take on more risk where appropriate or see where you’re exposed to unnecessary risk and adjust accordingly. You’ll also avoid being caught up in the emotion of market activity, where panic can lead to a poorly timed and costly decision.

[1] Charles Schwab: How to Determine Your Risk Tolerance Level https://intelligent.schwab.com/public/intelligent/insights/blog/determine-your-risk-tolerance-level.html.

[2] Investopedia https://www.investopedia.com/terms/r/risk.asp.

[3] Australian Government Department of Finance: Defining Risk Appetite and Tolerance https://www.finance.gov.au/government/comcover/education/risk-appetite-and-tolerance.

Source: BT

Will cash remain king?

By Robert Wright /May 28,2024/

Cash has been one of the best performing defensive assets over the past three years. When compared with global bonds (a riskier asset class), a typical portfolio of term deposits would have returned a cumulative 12.6% in comparison to -8.5% for global bonds over the three years to December 2023. With interest rates expected to stay higher for longer, cautious investors would be right to question whether other asset classes are worth the risk. But are the tides changing?

On paper cash still appears to be king; however, these healthy returns are attributed to accelerated inflation and rising interest rates, an environment we may be moving away from. Inflation has been trending downwards for months and rate cuts are predicted to begin before the end of 2024.

In this paper we explain why we believe now is a good time to revisit your asset allocation.

What is a bond?

A bond is a loan made by an investor to a borrower, generally a company or government. Typically, the borrower pays the investor interest (coupons) periodically over the term of the loan and then returns the initial value (principal) of the loan back to the investor at an agreed upon future date.

Bond values are linked to the borrowers perceived ability to pay back the loan as well as interest rates. For example, when interest rates rise, newly issued bonds offer higher coupons, making them more attractive and equivalent existing bonds with lower coupons less attractive, reducing their value.

How do bonds differ from term deposits?

Bonds are expected to provide higher returns over the long term because investors require compensation for assuming investment risk. Bonds also provide the opportunity for capital growth as well as higher income. This compares with term deposits where interest payments are lower but guaranteed by a bank – providing more security. Whilst income is guaranteed, the real value of a term deposit often diminishes over time due to inflation, which erodes your purchasing power (figure 1).

Figure 1 also shows that bonds are subject to greater risk over shorter time horizons which means they won’t be suitable for everyone. Your initial investment can go down in value and when you invest in funds this can be offset through the distributions, reducing your income. This primarily occurs when interest rates are rising and become unpredictable as they have in recent times.

Investors need to determine, with support from their adviser, whether trading term deposits capital guarantee for the potential increased return of a bond investment is suitable to their circumstances.

Why now?

In an environment where inflation is trending down and rates are expected to be cut, long term bonds should perform well as this is the environment when you typically experience the most capital growth (see figure 2). Term deposit rates are also forward looking. In other words, you don’t need to wait for central banks to reduce cash rates before you start to see term deposit returns fall. There are already signs of this happening. Whilst very recent, 1-year term deposit rates came down by 0.05% in January and we expect this trend to continue (although this won’t necessarily be a smooth journey). Whilst seemingly insignificant, this could be meaningful for larger investors. Particularly where capital growth has no role to play and investors don’t require the capital guarantee of cash.

What happens if the economy deteriorates?

If a recession were to occur, interest rates are more likely be cut quicker to encourage spending, resulting in bond prices rising. This would be supported by increased demand as investors move away from higher risk assets such as equities. If we don’t enter a recession and achieve a soft-landing scenario, rates will likely trend down more slowly to bring inflation in line with central banks’ targets; once again favouring bonds due to the inverse relationship between interest rates and bond values.

Conclusion

We believe it is critical to take a diversified approach to investing to help manage portfolio risks through different market conditions. The balance and mix of assets will depend on each investor’s ability and willingness to take on investment risk as well as how much of their capital they need guaranteed.

That said, we believe now is a great time to be reassessing your asset allocation. Investors looking for capital growth who don’t need capital guarantees should consider introducing bonds into, or back into, their investment portfolio and doing so before central banks begin to cut rates.

While cash rates may seem alluring, it is important to remember the distinct roles bonds and cash play in a portfolio. Cash is best reserved for short-term spending needs that require a guarantee as it will not provide the long-term capital growth and inflation protection of other assets.

It may seem daunting as we have been through a period of significant market volatility but over the long term, we have high conviction that bonds will provide better risk adjusted return outcomes for investors who are able to take on the increased risks offered by bonds.

As always, we recommend speaking to your financial adviser to get tailored advice based on your unique circumstances prior to making any investment changes.

Source: Perpetual

Falling inflation – what does it mean for investors?

By Robert Wright /February 16,2024/

Key points

- Inflation is in retreat thanks to improved supply and cooling demand. A further fall is likely this year.

- Australian inflation remains relatively high – but this mainly reflects lags rather than a more inflation prone economy.

- Profit gouging or wages were not the cause of high inflation.

- The main risks relate to the conflict in the Middle East escalating and adding to supply costs; a surprise rebound in economic activity and sticky services inflation; and floods, the port dispute and poor productivity in Australia.

- Lower inflation should be positive for investors via lower interest rates, although this benefit may come with a lag.

- The world is now a bit more inflation prone so don’t expect a return to near zero interest rates anytime soon.

Introduction

The surge in inflation coming out of the pandemic and its subsequent fall has been the dominant driver of investment markets over the last two years – first depressing shares and bonds in 2022 and then enabling them to rebound. But what’s driving the fall, what are the risks and what does it mean for interest rates and investors? This article looks at the key issues.

Inflation is in retreat

Inflation appears to be falling almost as quickly as it went up. In major developed countries it peaked around 8% to 11% in 2022 and has since fallen to around 3% to 4%. It’s also fallen in emerging countries.

Source: Bloomberg, AMP

What’s driving the fall in inflation?

The rise in inflation got underway in 2021 and reflected a combination of massive monetary and fiscal stimulus that was pumped into economies to protect them through the pandemic lockdowns that was unleashed as spending (first on goods then services) at a time when supply chains were still disrupted. So it was a classic case of too much money (or demand) chasing too few goods and services. Its reversal since 2022 reflects the reversal of policy stimulus as pandemic support measures ended, pent up or excess savings has been run down by key spending groups, monetary policy has gone from easy to tight and supply chain pressures have eased. In particular, global money supply growth which surged in the pandemic has now collapsed.

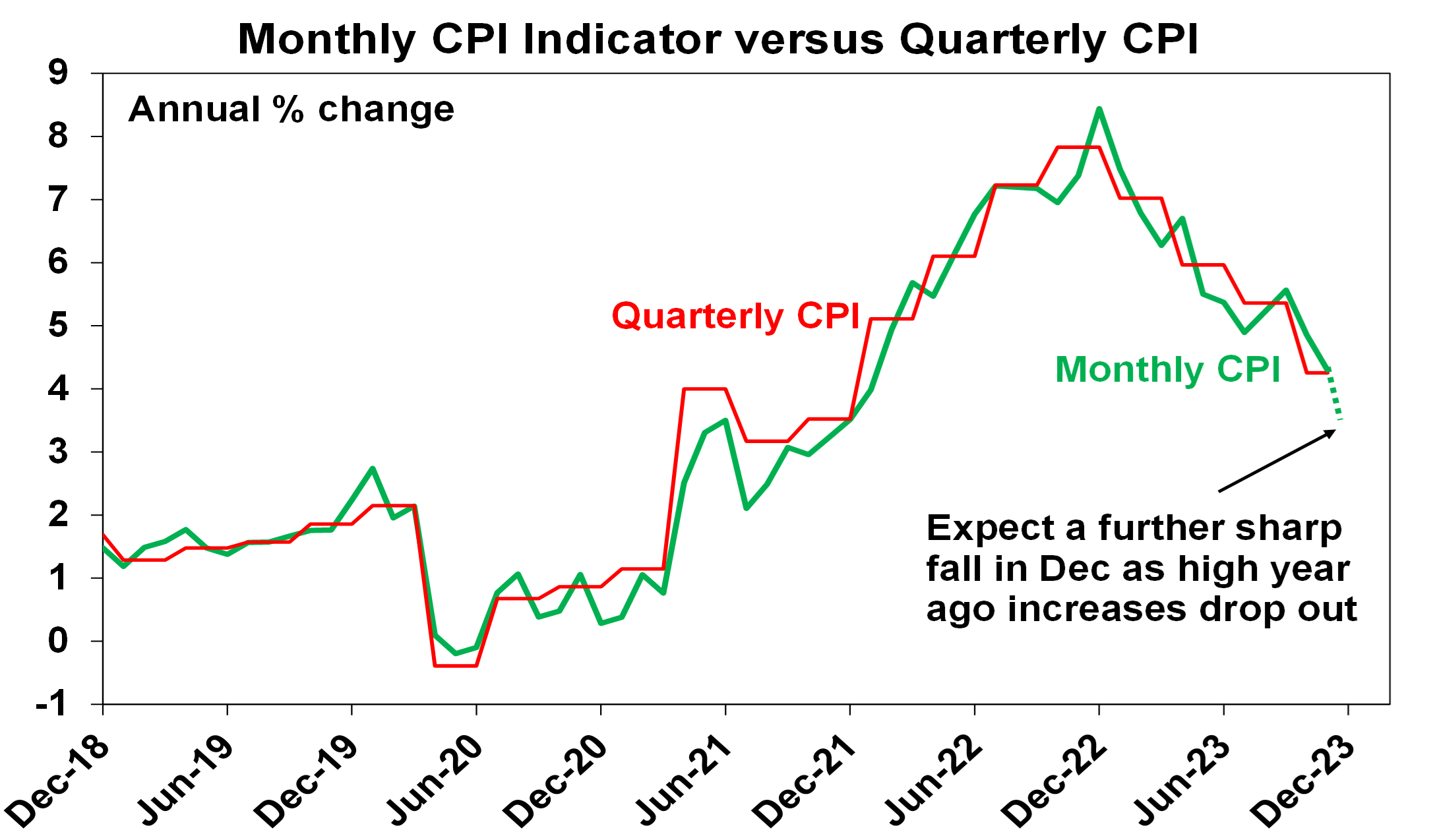

Why is Australian inflation higher than other countries?

While there has been some angst about Australian inflation (at 4.3% year on year in November) being higher than that in the US (3.4%), Canada (3.1%), UK (3.9%) and Europe (2.9%), this mainly reflects the fact that it lagged on the way up and lagged by around 3 to 6 months at the top. The lag partly reflects the slower reopening from the pandemic in Australia and the slower pass through of higher electricity prices. So we saw inflation peak in December 2022, whereas the US, for instance, peaked in June 2022. But just as it lagged on the way up it’s still following other countries down with roughly the same lag. In fact, with a very high 1.5% month on month implied rise in the Monthly CPI Indicator to drop out from December last year, monthly CPI inflation is likely to have dropped to around 3.3% to 3.7% year on year in December last year, which is more in line with other countries.

Source: Bloomberg, AMP

What about profit gouging?

There has been some concern that the surge in prices is due to “price gouging” with “billion dollar profits” cited as evidence. In fact, the Australian Government has set up an inquiry into supermarket pricing. There are several points to note in relation to this. First, it’s perfectly normal for any business to respond to an increase in demand relative to supply by raising prices. Even workers do this (e.g. asking for a pay rise and leaving if they don’t get one when they are getting lots of calls from headhunters). It’s the way the price mechanism works in allocating scarce resources. Second, national accounts data don’t show any underlying surge in the profit share of national income, outside of the mining sector. Finally, blaming either business or labour (with wages growth picking up) risks focusing on the symptoms of high inflation not the fundamental cause, which was the pandemic driven policy stimulus and supply disruption. This is not to say that corporate competition can’t be improved.

Source: ABS, RBA, AMP

What is the outlook for inflation?

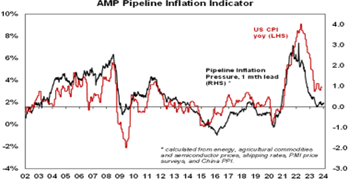

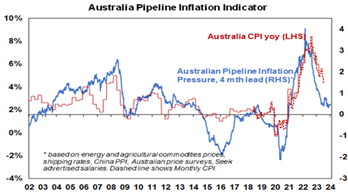

Our US and Australian Pipeline Inflation Indicators continue to point to a further fall in inflation ahead.

Source: Bloomberg, AMP

This is consistent with easing supply pressures, lower commodity prices and slowing demand. It’s not assuming recession, but it is a high risk and if that occurred it would likely result in inflation falling below central bank targets. Out of interest, the six month annualised rate of core private final consumption inflation in the US, which is what the Fed targets, has fallen below its 2% inflation target. In Australia, it’s expected that the quarterly CPI inflation to have fallen to around 3% year on year by year end. The return to the top of the 2% to 3% target is expected to come around one year ahead of the RBA’s latest forecasts.

What are the risks?

Of course, the decline in inflation is likely to be bumpy and some say that the “last mile” of returning it to target might be the hardest. There are five key risks to keep an eye on in terms of inflation:

- First, the escalating conflict in the Middle East has the potential to result in inflationary pressures. Disruption to Red Sea/Suez Canal shipping is already adding to container shipping rates due to extra time in travelling around Africa. So far this has seen only a partial reversal of the improvement in shipping costs seen since 2022 and commodity prices and the oil price remain down. The US and its allies are likely to secure the route relatively quickly such that any inflation boost is short lived. The real risk though, is if Iran is drawn directly into the conflict, threatening global oil supplies.

- Economic activity could surprise on the upside again keeping labour markets tight, fuelling prices and wages, and hence sticky services inflation.

- Central banks could ease before inflation has well and truly come under control in a re-run of the stop/go monetary policy of the 1970s.

- In Australia, recent flooding could boost food prices and delays associated with industrial disputes at ports could add to goods prices. At present though, the floods are not on the scale of those seen in 2022 and it’s expected that any impact from both to be modest (at say 0.2%).

- Finally, and also in Australia if productivity remains depressed, 4% wages growth won’t be consistent with the 2% to 3% inflation target.

What lower inflation means for investors?

High inflation tends to be bad for investment markets because it means higher interest rates; higher economic uncertainty; and for shares, a reduced quality of earnings. All of which means that shares tend to trade on lower price to earnings multiples when inflation is high, and growth assets trade on higher income yields. We saw this in 2022 with bond yields surging, share markets falling and other growth assets pressured.

Source: Bloomberg, AMP

So, with inflation falling, much of this goes in reverse as we started to see in the last few months. In particular:

- Interest rates will start to come down. The Fed is expected to start cutting in May and the European Central Bank (ECB) to start cutting around April, both with 5 cuts this year. There is some chance that both could start cutting in March. The RBA is expected to start cutting around June, with 3 cuts this year.

- Shares can potentially trade on higher price-to-earnings (PEs) than otherwise.

- Lower interest rates with a lag are likely to provide some support for real assets like property.

Of course, the main risk is if economies slide into recession, which will mean another leg down in share markets before they start to benefit from lower interest rates. This is not our base case but it’s a high risk.

Concluding comment

Finally, while inflation is on the mend cyclically, it’s worth remembering that from a longer term perspective we have likely now entered a more inflation prone world than the one prior to the pandemic, reflecting bigger government; the reversal of globalisation; increasing defence spending; decarbonisation; less workers and more consumers as populations age. So short of a very deep recession, don’t expect interest rates to go back to anywhere near zero anytime soon.

Source: AMP