Tag Archives: Managed Funds

Megatrends for 2025 and beyond…

By Robert Wright /February 28,2025/

Megatrends are long-term structural changes that affect the world we live in. Importantly, they shape communities but they also create investment opportunities and risks. Learnings from historical megatrends include: 1) they often solve a problem through innovation; 2) the scope of the megatrend can initially be underestimated; and 3) the duration of a megatrend is typically longer than anticipated. There are numerous megatrends likely to influence markets that investors should consider: the shift to the cloud and generative AI, the ageing population, rising geopolitical tensions and so on. Today we highlight just some of the current megatrends.

The continued growth in “winners take all” dynamics

A megatrend that continues to play out is growth in “winner take all” or at least “winner takes most” dynamics in the global economy. Reduced cross-border frictions, the growth in digital goods and distribution channels, and the increasing importance of scale and network effects have allowed companies to scale to a size almost unimaginable in the past.

The rise of the so called “magnificent seven”, the group of leading US technology companies, is a good example of these forces playing out. This group now accounts for a higher share of global markets than the leading companies of the tech bubble era of the early 2000s. However, unlike that time, their size today has predominantly been fuelled by enormous growth in revenues and profitability, albeit some speculative elements may have played a part more recently.

A key risk for some of these businesses is antitrust. Microsoft, Apple and Alphabet have recently attracted the attention of the antitrust authorities, with increased competition the primary motive. We view that it is a low probability that regulators break up these businesses, meaning the underlying economic forces will continue to allow successful businesses to scale far more quickly and to far larger sizes than historically was the case. This presents a significant opportunity for global investors, as these companies can deliver outsized returns. On the other hand, these trends also increase disruption risks to legacy businesses and industries.

To benefit from the former and guard against the latter, investors should focus on quality companies that have strong and enduring competitive advantages. These advantages typically include scale, pricing power, brand strength, network effects and intellectual property.

Glucagon-like peptide-1s (GLP-1s) and solving obesity

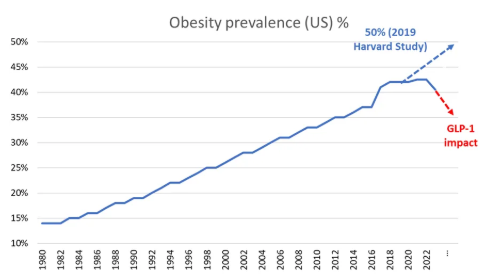

One of the biggest health issues facing developed countries is obesity. The development of the GLP-1 class of weight loss drugs such as Ozempic promises to transform the treatment of obesity and significantly improve health outcomes for societies. GLP-1s stimulate the brain to reduce hunger and act on the stomach to delay emptying, so you feel fuller for longer, have a lower calorie intake and lose weight.

Take up is likely to be strong over coming years as supply constraints ease and continued innovation delivers a more convenient oral pill and mitigates potential side effects such as nausea. Growing clinical evidence of health benefits, such as lower risk of heart problems, will also encourage governments and insurers to cover the cost of the drugs. These developments have dramatically changed the outlook for obesity, with the US recording its first fall in obesity rates since at least the 1970s, a dramatic turnaround from predictions of just a few years ago.

Source: CDC, OECD, WHO, IHME, Harvard

The development also has some significant investment implications. Most obvious are the potential investment opportunities in the drug manufacturers, although given high expectations we need to carefully monitor scientific developments and the pricing environment. There are also several investment risks to consider, with the potential for lower demand for certain medical device companies, food manufacturers and quick service restaurants.

The unrelenting rise in sovereign debt

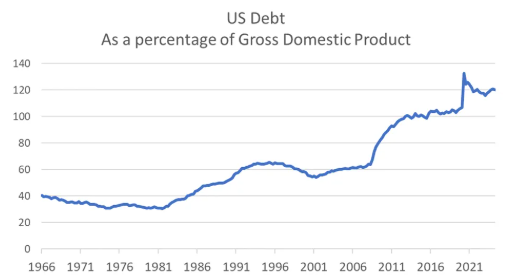

Not all megatrends are positive for investors; one megatrend to be wary of is rising sovereign debt. In many parts of the world fiscal responsibility is no longer a priority as governments focus on more immediate issues and winning elections. In the US the national debt has been rising since the 1980s. In 2010, following the government’s response to the Global Financial Crisis, it first exceeded 90% as a percentage of GDP – the level identified by academics Reinhart and Rogoff as associated with a worsening in growth outcomes. A further spending binge during the 2020 COVID pandemic has resulted in the US national debt rising to more than 120% of GDP.

Source: Federal Reserve Economic Data

With the US Federal budget deficit expected to hit $1.8 trillion in 2024 and both parties promising billions more in spending, debt is likely to continue to build. US national debt has not been a major issue for markets to date, but the risk of a debt crisis, accompanied by rising bond yields and volatile markets, increases as debt levels continue to rise. Many other countries are in a similar position, with debt to GDP exceeding 100% in the UK, France, Spain, Italy and Japan. Australia is relatively well placed with the national debt at 38% of GDP.

What does this mean for investors? Governments have three ways to “solve” excessive national debt: (1) austerity – cutting spending and raising taxes; (2) default; or (3) financial repression – printing money to inflate the problem away. The first is politically unpalatable and appears unlikely, the second would be an outright disaster and can be avoided by countries that issue debt in their own currency such as the US. Thus, the most likely outcome is money printing, or central bank financing of budget deficits in more technical terms, resulting in a period of structurally higher inflation.

While it’s impossible to be precise in terms of the timing of a potential debt crisis, investors can seek to protect themselves by investing in real assets, such as property and equities, with a focus on high quality companies with pricing power that can protect investors in times of high inflation.

These are just a few of the megatrends shaping markets today and in the future. As investors, a long-term focus and active management are key to both taking advantage of the opportunities these trends provide and avoiding risks that may arise.

Source: Magellan

The ins and outs of geared share funds

By Robert Wright /February 28,2025/

Geared share funds are high risk and high reward. When share markets are doing well, the returns can be very high, but the opposite is also true. We look at the pros and cons, and the role of geared share funds in a diversified investment strategy.

Geared share funds can be a great way for investors to invest in shares – and share in the rewards – when the share market performs well over long periods of time.

Geared share funds magnify both positive and negative returns, so they’re considered high risk, high return investment options.

But exactly what is a geared share fund, and are they for everyone?

Let’s take a look at the ins and outs of this unique investment option.

What is a geared share fund?

Geared share funds accept money from investors and borrow money to invest alongside investors’ capital. The fund uses the pool of investors’ money and borrowed money to buy shares.

They amplify both positive returns and negative returns on the shares in which the fund invests.

On the upside, geared share funds generate higher returns than overall share market returns when markets are rising. Conversely, the value of your investment will drop further than equivalent investment options without internal gearing.

They are best explored as part of a long term, diversified investment strategy.

How do geared share funds work?

When you invest money in a geared share fund, the fund will borrow money to invest on your behalf, alongside your investment.

For example, for every $1,000 you invest in the fund, the geared share fund may borrow another $1,000. That would give you $2,000 of exposure to the shares in which the fund invests. So in addition to the returns generated from your capital, you also receive all the returns from the borrowed funds (less the cost of borrowing).

The fund’s gearing, or borrowing, effectively magnifies the returns of the underlying investments, whether they are gains or losses.

Geared share funds generally perform well when the share market is growing at a higher rate than the interest charged on borrowed money.

Geared share funds borrow at institutional interest rates, which are generally lower than those offered to individual investors.

Pros of geared share funds

- The gearing, or borrowing, is done within the fund: unlike a margin loan, the fund, rather than the investor, is responsible for repaying its loans. This model allows investors to keep a long term view on their investments, rather than worry about day to day performance of their investments.

- Investor exposure is limited to their invested capital: while the fund borrows on behalf of its investors to buy shares, if the share market falls, and the fund’s loans need to be repaid, individual investors will never lose more than their invested capital.

- Gains are magnified by gearing: when the shares in which the fund invests go up, the return to the investor may be much higher than if they had simply purchased an equivalent fund without gearing.

- Franking credits are magnified by gearing: when a geared fund invests in Australian shares, the gearing will also magnify the level of franking credits payable as part of income distributions.

- Long term gains magnify long term share performance: investors seeking to invest for a decade or more, and who are willing to ride out short term market falls, can do very well with geared share funds. The compounding effect of the additional returns from gearing is very powerful over the long term.

Cons of geared share funds

- Fees are relatively high: fees are charged not just on the $1,000 you invest, but also on the $1,000 that the fund borrows on your behalf. Fees reduce your return.

- Losses are magnified by gearing: when the shares in which the fund invests go down, losses will be much higher than if you simply purchased the same shares with the same initial investment.

- Short term share market falls can lead to big investment losses: investors who need to take out their capital at a particular point in time, or who are not prepared to wait for markets to recover, can suffer big losses if this coincides with a fall in markets.

When to consider geared share funds

Geared funds can play an important role within a diversified portfolio for investors looking for above average investment performance over the long term by accelerating their Australian and/or global share allocations.

Investors who can ride out short term market volatility and do not need to take out their money in the short term, may benefit from the long term returns that geared share funds can offer. Geared funds should therefore be particularly attractive to superannuation investors who cannot access their capital until retirement.

Investors who are risk averse and who may need to cash in their investment in the short term, may not find geared share funds a suitable investment.

Investors should always seek financial advice to ensure investments are suitable for their objectives, investment horizon, and personal circumstances.

Source: CFS

What is a distribution?

By Robert Wright /November 20,2024/

A managed fund generates income from its investments – for example, through share dividends, interest on cash or fixed interest investments in the fund, or any gains made when fund investments (like shares) are sold. So in short, a distribution is profit or income made by a fund and paid to investors.

How are distributions paid?

Managed investment funds are required to pay all realised income and capital gains to investors for the financial year. Income can be paid monthly, quarterly, half yearly or yearly, depending on the fund. You may receive your distribution as a cash payment, for instance as a payment to your designated bank account, or as an amount that is reinvested back into the fund. As an investor, you should also receive a statement that outlines the amounts and types of income generated by the fund and distributed to you, which may be helpful at tax time.

How are distributions calculated?

- The income of all individual investments in a fund for a given time period is calculated taking into account things like share dividends or interest payments.

- The fund’s deductible expenses (things like management fees and other payables) are then subtracted, leaving the total amount of income that can be paid out.

- That amount is then divided by the total number of units in the fund to provide an amount of distribution per unit. For example, if the distribution for a fund was $1 per unit and an investor owned 100 units in the fund, they would receive a distribution of $100.

What does the unit price have to do with distributions?

When you invest in a fund, you’re pooling your money with other investors to access a professionally managed portfolio of investments overseen by skilled investment managers. In exchange, you’re allocated a number of units that correspond to how much money you’ve invested – based on the fund’s unit price at the time of investment.

Why does the unit price fall after a distribution?

When you receive a distribution for the income generated by a fund’s investments, the value of the fund reduces by the amount of the total distribution. This results in a lower unit price because income from the fund’s investments is being paid from the fund to investors, reducing the total value of the fund’s assets – a figure that is divided by the total number of units owned in the fund to determine the unit price. This doesn’t mean you’ve lost money on your investment or that your investment in a particular fund has changed – rather, you retain the same number of units in the fund, which has simply decreased in value by the amount of the distribution paid to you. Distributions that are reinvested back into a fund are used to acquire more units in it. This means the value of your investment should not fall as you will be allocated additional units.

Why aren’t distributions paid to super funds?

While managed investment options (funds) outside of super pay distributions to investors, investment options within super do not. That’s because there is a different structure and purpose for super, which members can’t access until retirement. Generally, super balances fluctuate higher and lower over time depending on the contributions members make and the performance of the funds their super is invested in. Investment options within super contribute to super balances through the unit price, which changes daily based on the performance of each fund’s investments. Effectively, the distribution amount is retained in your super and forms part of your super balance, which over time can be used to acquire more investments in the options your super is invested in.

Source: Colonial First State

Decoding cognitive biases: what every investor needs to be aware of

By Robert Wright /August 23,2024/

Common human biases that investors should understand when it comes to investing is extremely important. These biases are ingrained in human nature, leading to tendencies to oversimplify, rely on quick thinking or exhibit excessive confidence in judgments, which may lead to investment mistakes. By gaining insight into these biases, investors may be able to make better decisions to help reduce risk and improve their investment outcomes in the long-term.

Numerous cognitive biases can affect how decisions are made. The key to mitigating these biases lies in recognising their presence, identifying when they might arise and then either making appropriate adjustments or obtaining help to moderate their impact.

Seven cognitive biases that might arise at various stages of an investor’s investing journey.

- Herding: The tendency to follow and mimic the actions of a larger group.

- Confirmation bias: The preference for information that confirms one’s existing beliefs or hypotheses.

- Overconfidence effect: Excessive confidence in one’s own investment decisions and abilities.

- Loss aversion: When the fear of loss is felt more intensely than the elation of gains.

- Endowment effect: Overvaluing assets because they are owned.

- Neglect of probability: Disregarding the actual likelihood of events and often overemphasising rare occurrences at the expense of more probable outcomes.

- Anchoring bias: The tendency to rely too heavily on a past reference or a single piece of information when making decisions.

Herding

The herd mentality occurs when people find reassurance and comfort in a concept that is widely adopted or believed by many others. In recent times, we have seen the herd mentality with the events that surrounded the GameStop stock event. Where many people saw the rise in stock prices and without proper investment research followed the trend of many others and invested.

This impacted a lot of investors who bought the stock due to the fear of missing out and the hype it created. We believe, to be a successful investor, you must be able to analyse and think independently. Speculative bubbles are typically the result of herd mentality. Herd mentality in investing can overshadow rational decision making and could increase the risk of financial losses.

Investors need to recognise the feeling of pressure to conform to popular opinion or follow the crowd and instead consider conducting research and analysis before making decisions, as well as seeking alternative views to challenge the consensus.

Confirmation bias

Confirmation bias is the tendency to favour information that corroborates pre-existing beliefs or theories. In our view, confirmation bias can lead to significant errors in investing. Investors may develop an inflated sense of certainty when they encounter consistent evidence supporting their choices. This overconfidence can create an illusion of infallibility, with an expectation that nothing can go wrong.

Overconfidence bias

Overconfidence bias in investing is where investors overestimate their knowledge, intuition and predictive capabilities, often leading to poor financial decisions. This bias can present itself through various ways such as excessive trading, under-diversification and the general disregard for potential risks.

Investors with overconfidence bias tend to believe they can time the market or have the ability to pick the winning stocks better than most, which in turn may also result in overtrading and increased transaction costs. Overconfidence can also lead to a lack of proper risk assessment and analysis, as investors might underestimate the likelihood of negative events or industry dynamics affecting their investments.

An example of overconfidence bias occurred during the dot-com bubble of the late 1990s and early 2000s. Many investors were overly optimistic about the growth potential of internet related companies. This led to inflated stock prices as more and more people invested in these companies without proper evaluation of their actual worth.

Loss aversion

Loss aversion is where a real or potential loss is perceived as much more severe than an equivalent gain. The pain of losing is often far greater than the joy in gaining the same amount.

This overwhelming fear of loss can cause investors to behave irrationally and make bad decisions, such as holding onto a stock for too long or too little time. For example, an investor whose stock begins to tumble, despite clear signs that recovery is unlikely, may be unable to bring themselves to sell due to the fear of loss in the portfolio. On the flip side, when a stock in the portfolio surges, they may quickly cash out, not wanting to see the possibility of those profits disappearing.

When an investor clings onto failing stocks, departs with successful stocks too quicky and fear governs their investment decision, it’s known as the disposition effect. It’s a direct consequence of loss aversion, leading investors to make overly cautious choices that ultimately undermine their financial goals.

So, understanding this bias may help investors make rational decisions to grow their portfolios while managing risk effectively.

Endowment effect

Closely related to the concept of loss aversion is the endowment effect. This effect arises when individuals place a greater value to items because they own them, as opposed to identical items that they do not own. It’s a cognitive bias where ownership elevates the perceived value of an item beyond its objective market value.

For example, an investor may develop a strong attachment to a particular stock. It could be the very first stock they ever invested in, or they may favour the company for a particular personal reason such as aligning with their values. If this stock begins to fall and financial experts are advising to sell, because of the value bias this investor has they may be unwilling to sell. The investor perceives the stock’s value as greater than what the market dictates, purely because of ownership. It is a delicate balance that is needed to be able to determine between attachment and sound financial decision making and can be challenging for some investors.

To help mitigate the endowment effect, investors should regularly review their portfolios and consider the help of a financial adviser. Establish clear, predefined criteria for selling assets, aligned with financial goals. Develop a detailed investment plan with specific financial goals, a well defined investment strategy is crucial to prevent emotional decision making. Understanding and focusing on long-term investment goals can also help in maintaining objectivity.

Neglect of probability

Humans often overlook or misjudge probabilities when making decisions, including investment decisions. Instead of considering a range of possible outcomes, many people tend to simplify and focus on a single estimate. However, the reality is that any outcome an investor anticipates may just be their best guess or most likely scenario. Around this expected outcome, there’s a range of potential results, represented by a distribution curve.

This curve can vary widely depending on the specific characteristics of the business involved. For instance, companies which are well established and have strong competitive positions, tend to have a narrower range of potential outcomes compared to less mature or more volatile companies, which are more susceptible to economic cycles or competitive pressures.

Another error investors may make is to overestimate or misprice the risk of very low probability events. That does not mean that ‘black swan’ events cannot happen but that overcompensating for very low probability events can be costly for investors.

Anchoring bias

Anchoring bias is the inclination to excessively rely on a previous reference or a single piece of information when making decisions. Numerous academic studies have explored the impact of anchoring on decision making. Typically, these studies prompt individuals to fixate on a completely random number (such as their birth year or age) before asking them to assign a value to something. The findings consistently demonstrate that people’s responses are influenced by the random number they focused on prior to being asked the question.

Looking at a recent share price is a common way investors may anchor their decisions. Some people even use a method called technical analysis, which looks at past price movements to predict future ones. However, just because a stock’s price was high or low in the past doesn’t tell us if it’s a good deal now.

Source: Magellan