Tag Archives: Women in Finance

What to do when your fixed rate home loan term is ending

By Robert Wright /May 19,2023/

Many Australians were fortunate to lock in record low interest rates but this may be drawing to an end.

A large portion of mortgages will be approaching the end of their fixed term, leaving many households paying two to three times their current fixed rate.

In this article, we’ll explain what to expect when your fixed interest rate ends and how to prepare for it.

What happens when your fixed rate home loan ends?

When your fixed term is nearing its end, you’ll need to decide whether to re-fix your loan at a new rate, change to a variable rate or consider switching to a new mortgage provider.

If you don’t do anything before the fixed term lapses, on expiry your mortgage provider generally switches your loan to its standard variable rate, which can be much higher than some of the discounted options available to new customers.

The best thing to do is contact your provider and ask them about your options, including what rates they can offer you.

How to prepare

Consider reviewing your mortgage at least 3 months before the fixed rate expires, as this will give you time to implement changes if required.

Here are some steps to go about this:

1. Negotiate with your current mortgage provider

It’s worth speaking to your current provider in advance to find out what variable rate you’ll be paying. This gives you an opportunity to check out other rates available in the market and think about whether switching providers is a better solution.

You can also see if you can negotiate a better rate as this may save you a lot of effort in moving to a new provider.

2. Research what other mortgage providers are offering

Now is a good time to see how your loan stacks up against other loans out there. This will help you determine if you’re getting a competitive interest rate.

If you do find a better offer, switching providers can be a smart move but it’s important to look at the costs involved in switching, borrowing costs and switching fees, as these can often outweigh the benefits.

Before you make any decisions, crunch the numbers with an online mortgage switching calculator.

3. Consider re-fixing your loan

If you like the predictability that comes with a fixed rate loan, you can re-fix your mortgage with an up to date interest rate.

However, you will be locked into the new fixed interest rate for a period of your loan term, unless you choose to end the contract earlier which may result in break costs.

Be sure to also carefully check out the features of a fixed loan too, such as fee-free extra repayments, redraw and linked offset accounts. Many fixed rate loans do not provide these features.

4. Consider a split loan

If you’re struggling to decide between a variable or fixed rate, or if you’re keen on a combination of flexibility plus certainty, you can choose to have part of your mortgage fixed and part of it variable.

For example, you could have 60% of your loan on a fixed rate and 40% on a variable rate.

This approach can provide the best of both worlds. The variable rate component gives you flexibility, while the fixed portion shelters part of your loan from rising interest rates.

5. Get help from an expert

If you can’t decide which option is best for you, a mortgage expert may be able to steer you in the right direction.

Mortgage experts can look at your finances and recommend some of the best home loan options to suit your specific needs. They’ll also be able to guide you through switching to another provider if that’s the path you choose to take.

Get a home loan health check

A home loan health check could help you to:

- find ways to fine tune your loan

- get more certainty or flexibility on interest rate options

- reduce your repayments

- pay off your loan sooner.

6. Make extra repayments before your fixed rate ends

If it’s possible for you to do so, consider paying off as much of your mortgage as possible before you’re hit with a higher interest rate.

By reducing your mortgage balance before your interest rate increases, you could save a lot of money on interest payments before it moves to the new rate.

How to manage higher repayments

When your fixed mortgage rate finishes and your repayments start increasing, your finances may need to be reviewed to cope with the new reality of rising interest rates.

There are ways to help you save and potentially earn more money, which may compensate for the rate increase.

1. Review your budget

While it may not be an option for everyone, there are expenses you can cut back on such as:

- taking public transport to work to reduce petrol costs and parking

- online shopping habits

- expensive memberships that you don’t regularly use

- taking advantage of government and council rebates to reduce your energy bill

- switching to energy efficient appliances and lightbulbs

- reviewing your utility and insurance providers – there may be better deals on offer which could save you hundreds of dollars.

2. Increase your income

Looking for ways to increase your income can help you manage higher repayments once your fixed rate expires.

Consider asking your manager for a salary raise or look for a higher paying job.

You could also consider starting a side hustle like dog walking or online tutoring to make extra cash. Another option is to rent out a room or parking space.

3. Consider opening an offset account

An offset account is like a transactional savings account linked to your mortgage balance. The funds in this account can reduce the amount of interest you pay on your mortgage, so holding your savings here can be beneficial.

For example, if you have a $600,000 mortgage balance and $100,000 in your offset account, you’ll only be charged interest on $500,000.

Source: IOOF

Five charts on investing to keep in mind in rough times

By Robert Wright /May 19,2023/

Key points

- Successful investing can be really difficult in times like now with immense uncertainty around inflation, interest rates, issues in global banks and recession risks impacting the outlook for investment markets.

- This makes it all the more important to stay focused on the basic principles of successful investing.

- These five charts focus on critical aspects of investing that are insightful in times of market stress: the power of compound interest; don’t get blown off by cyclical swings; the roller coaster of investor emotion; the wall of worry; and market timing is hard.

Introduction

Every so often the degree of uncertainty around investment markets surges and that’s been the case for more than a year now reflecting the combination of high inflation, rapid interest rate hikes, the high and rising risk of recession which has been added to in the last few weeks by problems in US and European banks. And all of this has been against the background of increased geopolitical uncertainties. Falls in the value of share markets and other investments can be stressful as no one wants to see their wealth decline. And so when uncertainty is high a natural inclination is to retreat to perceived safety. As always, turmoil around investment markets is being met with much prognostication, some of which is enlightening but much is just noise. I will be the first to admit that my crystal ball is even hazier than normal in times like the present. As the US Economist, JK Galbraith once said “there are two types of economists – those that don’t know and those that don’t know they don’t know.” And this is certainly an environment where we need to be humble.

But while history does not repeat as each cycle is different, it does rhyme, in that each cycle has many common characteristics. So, while each cycle is different the basic principles of investing still apply. This note revisits once again five charts I find particularly useful in times of economic and investment market stress.

Chart #1 The power of compound interest

This is my favourite chart. It shows the value of $1 invested in various Australian assets in 1900 allowing for the reinvestment of dividends and interest along the way. That $1 would have grown to $246 if invested in cash, to $997 if invested in bonds and to $781,048 if invested in shares up until the end of February. While the average return since 1900 is only double that in shares relative to bonds, the huge difference between the two at the end owes to the impact of compounding or earning returns on top of returns. So, any interest or return earned in one period is added to the original investment so that it all earns a return in the next period, and so on. I only have Australian residential property data back to 1926 but out of interest it shows (on average) similar long term compounded returns to shares.

Key message: to grow our wealth, we must have exposure to growth assets like shares and property. While shares and property have had a rough ride over the last year as interest rates surged, history shows that both will likely do well over the long term.

Chart #2 Don’t get blown off by cyclical swings

The trouble is that shares can have lots of (often severe) setbacks along the way as is evident during the periods highlighted by the arrows on the previous chart. Even annual returns in the share market are highly volatile but longer term returns tend to be solid and relatively smooth, as can be seen in the next chart. Since 1900, for Australian shares roughly two years out of ten have had negative returns but there are no negative returns over rolling 20-year periods.

The higher returns that shares produce over time relative to cash and bonds is compensation for the periodic setbacks they have. But understanding that these periodic setbacks are just an inevitable part of investing is important in being able to stay the course and get the benefit of the higher long term returns shares and other growth assets provide over time.

Key message: short term, sometimes violent swings in share markets are a fact of life but the longer the time horizon, the greater the chance your investments will meet their goals. So, in investing, time is on your side and it’s best to invest for the long term when you can.

Chart #3 The roller coaster of investor emotion

It’s well known that the swings in investment markets are more than can be justified by moves in investment fundamentals alone – like profits, dividends, rents and interest rates. This is because investor emotion plays a huge part. This has been more than evident over the last year with all the swings in markets. The next chart shows the roller coaster that investor emotion traces through the course of an investment cycle. Once a cycle turns down in a bear market, euphoria gives way to anxiety, denial, capitulation and ultimately depression at which point the asset class is under loved and undervalued and everyone who is going to sell has – and it becomes vulnerable to good (or less bad) news. This is the point of maximum opportunity. Once the cycle turns up again, depression gives way to hope and optimism before eventually seeing euphoria again.

Key message: investor emotion plays a huge role in magnifying the swings in investment markets. The key for investors is not to get sucked into this emotional roller coaster. Of course, doing this is easier said than done, which is why many investors end up getting wrong footed by the investment cycle.

Chart #4 The wall of worry

There is always something for investors to worry about it seems. And in a world where social media is competing intensely with old media it all seems more magnified and worrying. This is arguably evident again now in relation to uncertainty about inflation, interest rates and associated recessions risks. The global economy has had plenty of worries over the last century, but it got over them with Australian shares returning 11.7% per annum since 1900, with a broad rising trend in the All Ords price index as can be seen in the next chart, and US shares returning 9.9% pa. (Note that this chart shows the All Ords share price index whereas the first chart shows the value of $1 invested in the All Ords accumulation index, which allows for changes in share prices and dividends.)

Key message: worries are normal around the economy and investments and sometimes they become intense – like now but they eventually pass.

Chart #5 Timing is hard

The temptation to time markets is immense. With the benefit of hindsight many swings in markets like the tech boom and bust and the GFC look inevitable and hence forecastable and so it’s natural to think why not switch between say cash and shares within your super fund to anticipate market moves. This is particularly the case in times of emotional stress like now when much of the news around inflation, interest rates and recession risks seem bad. Fair enough if you have a process and put the effort in. But without a tried and tested market timing process, trying to time the market is difficult. A good way to demonstrate this is with a comparison of returns if an investor is fully invested in shares versus missing out on the best (or worst) days. The next chart shows that if you were fully invested in Australian shares from January 1995, you would have returned 9.3% pa (with dividends but not allowing for franking credits, tax and fees).

If by trying to time the market you avoided the 10 worst days (yellow bars), you would have boosted your return to 12.2% pa. And if you avoided the 40 worst days, it would have been boosted to 17.1% pa! But this is very hard, and many investors only get out after the bad returns have occurred, just in time to miss some of the best days. For example, if by trying to time the market you miss the 10 best days (blue bars), the return falls to 7.2% pa. If you miss the 40 best days, it drops to just 3% pa.

Key message: trying to time the share market is not easy. For most its best to stick to an appropriate well thought out long term investment strategy.

Source: Shane Oliver, AMP

Where is the Recession?

By Robert Wright /May 19,2023/

Key points

- A progress report on inflation: Inflation appears to have peaked, led by improvements in core goods prices and rate sensitive sectors like housing. The policy focus has shifted to labour market normalisation where early signs of progress are emerging.

- Is a soft landing in sight? The Fed remains committed to doing “whatever it takes” to bring inflation to the targeted level. Despite the aggressive tightening we’ve seen so far, alternative data indicators suggest that the economy remains on relatively solid footing.

- Equity market positioning: We are positioned for themes of continued high rates, improving sentiment outside the US and a potential soft economic landing. This is expressed with a preference for value particularly in cyclical sectors including capital goods, consumer durables, autos and airlines.

2022 was a year where extreme macroeconomic and geopolitical events shaped market behaviour. The US Consumer Price Index (CPI) peaked at 9.1%, the highest level in over 40 years. The subsequent policy response saw the US Federal Reserve (Fed) deliver 4.25% of rate hikes across only seven meetings. This was the fastest cycle of rate hikes since the early 1980s, a period of stubborn inflation and aggressive policy action that ultimately ended in a recession.

As we begin 2023, there’s a greater level of clarity around some of the questions that have driven markets over the last year. Recent inflationary data shows improvements in the trajectory of core goods prices and rate sensitive components. Now, the focus of policymakers has shifted towards restoring balance in the labour market and doing “whatever it takes” to bring inflation to the targeted level. As we enter a new phase of tightening beyond peak price pressures, what does alternative data reveal about the path of inflation and the recession that so many are expecting?

A progress report on inflation

In the final months of 2022, long awaited improvements in the trajectory of inflation began to surface. Figure 1 shows the widening gap between current reported inflation and where US CPI is expected to stand in six months based on a broad range of leading economic indicators and text mined commentary on inflation. Peak inflation seems to be behind us and a clearer path towards meeting central bank objectives has started to appear. As observed in the inflation GPS measure, the sentiment of corporate comments around cost pressures and the effects of inflation on margins hasn’t showed signs of deteriorating as the outlook improves.

Figure 1: US Inflation GPS shows continued decline in the trajectory of consumer prices

Current US Inflation vs six month inflation expectations

Source: Refinitiv DataStream, chart by the BlackRock Investment Institute, December 2022. The BlackRock Inflation GPS shows where core (excluding food and energy) consumer price inflation may stand in six months’ time. The GPS models the relationship between rates of core inflation and a broad set of economic indicators including measures of slack, inflation expectations, and other inflation related data such as business surveys and wages. It also incorporates a proprietary Systematic Active Equity signal measured through text mining of commentary on inflation.

Core goods prices, where the initial surge in inflation was the most robust, are showing significant progress. This has continued to play out with the shift in spending from goods to services throughout the economic reopening and the healing of supply chain bottlenecks. Figure 2 shows average freight transportation costs which have fallen back to pre pandemic levels. These costs were previously 14 times greater during the peak of supply chain issues.

Figure 2: Global supply chains have mostly recovered with shipping costs returning to pre COVID levels

Average freight costs for shipping a 40ft container

Source: BlackRock, with data from Bloomberg, as of January 2023. All amounts in USD.

Shelter is another category where alternative data is pointing to a clear disinflationary trend throughout 2023. Shown in Figure 3, the growth rate of new online rental listings in the US has started to decline. The Owners’ Equivalent Rent (OER) component of CPI which captures both new and continuing leases tends to lag this alternative rental data by 6 to 9 months. This suggests that the trend we’re seeing in new leases will increasingly impact CPI data as the year goes on.

Figure 3: The growth rate of new rental leases has started to decline, a trend that will increasingly impact CPI data

Online new rental leases vs. Owners’ Equivalent Rent (OER)

Source: BlackRock, with data from Apartment List and Zillow, January 2023.

For the next phase of the tightening cycle, Fed officials have shifted their focus to labour markets. Wages have remained a persistent driver of broad-based services inflation since the economic reopening began. Historical periods of inflation have shown that reining in wage inflation is a critical step in restoring price stability and preventing long-run expectations from becoming unanchored. In early November, Fed Chairman Jerome Powell identified 3.5% wage growth as a targeted level that would be consistent with the Fed’s 2% inflation objective.

To monitor the trajectory of wage growth, we use online job postings in the US for a real time view of employment cost data ahead of official releases (Figure 4). Wage growth has started to moderate in recent months and shows signs that the labour market is finally beginning to cool. However, more progress is needed to reach the Fed’s target especially in the services sector where inflationary pressures remain the most stubborn.

Figure 4: Wage growth is showing signs of moderating, but more progress is needed

Year over year wage growth for goods vs services roles

Source: BlackRock, with data from Burning Glass Technologies, as of January 2023.

Is a soft landing in sight?

The likelihood of a soft vs hard landing depends on how healthy the economy remains as inflation continues to normalize and how policymakers react to ongoing developments. So what does the data tell us about where the economy is heading?

Let’s first examine the underlying drivers of the readjustment that’s taking place in labour markets. Following COVID-19, a labour shortage emerged as many individuals didn’t immediately return to the workforce. Simultaneously, the economic reopening drove robust demand for workers and a significant increase in job openings, many of which remained vacant due to labour supply constraints. As a result, the recent normalisation in labour markets and wages has mostly come from a decrease in job openings. This differs from past periods of inflation where monetary tightening caused severe job losses and high unemployment that ultimately ended in a recession.

Figure 5 shows the decline that we’ve seen in the number of online job postings as labour demand falls. Most of the pullback in job postings is concentrated in the technology sector. This is also the case for layoffs which remain extremely benign across the broader economy. Importantly, job openings remain elevated in aggregate relative to pre COVID, suggesting that the gap between labour demand and supply can continue to narrow through a decline in job openings rather than severe layoffs.

Figure 5: Falling labour demand has come through declines in job openings, not layoffs

Volume of online job postings normalised to 2020 levels

Source: BlackRock, with data from Indeed.com, as of January 2023.

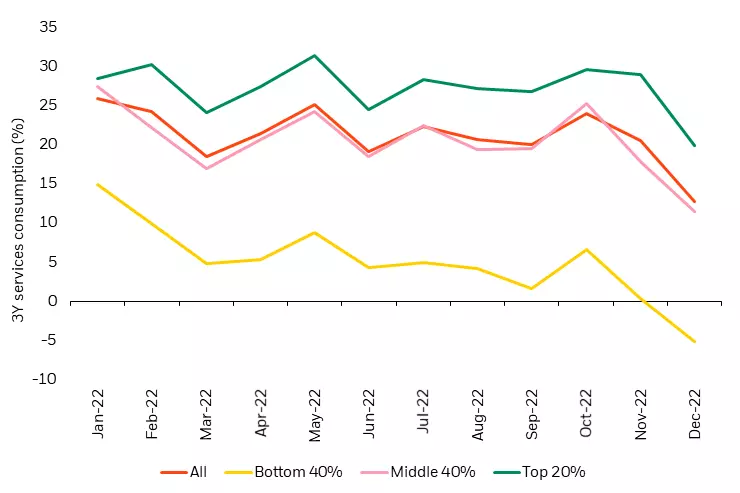

Along with company behaviour, we’re closely monitoring consumer activity for signs of weakness. Figure 6 shows US inflation adjusted consumer spending in the services sector which remains relatively stable and above pre COVID levels despite starting to decline particularly for the lowest income cohort. How has this level of consumer activity been sustainable as savings rates have fallen to historical lows amid higher interest rates? The previous period of unprecedented fiscal stimulus throughout the pandemic has kept the total level of household savings in excess, even long after stimulus payments have tapered off. Furthermore, household interest payments remain well below the pre COVID trend with less debt on consumer balance sheets. The combination of sustained excess savings, lower debt levels, and muted layoff activity has allowed consumer spending to remain relatively resilient over the course of the Fed’s tightening cycle.

Figure 6: US Services spending remains above 2019 levels despite signs of weakness

3Y Discretionary service consumption by income cohort adjusted for inflation

Source: BlackRock, Yodlee/ConsumerEdge, Earnest Research, as of December 2022.

Alternative data reveals an improving picture for inflation, orderly rebalancing of the labour market and a relatively healthy consumer – each currently more supportive of the case for a soft landing than a hard landing.

Market pricing has increasingly shifted towards the expectation for interest rate cuts by the end of 2023 (Figure 7). This can be supported by two opposing viewpoints: 1) the hard landing scenario which expects policymakers to overtighten and engineer a recession, or 2) a scenario where inflation swiftly returns to the 2% target and the Fed is able to begin easing financial conditions. In our view, both of these scenarios are unrealistic. Instead, we believe rates will remain higher for longer rather than a near term policy pivot. Today’s relatively stable economy may remain more resilient to high rates and policymakers are likely to delay easing financial conditions due to the lingering effects of two years of excessive inflation.

Figure 7: Market is currently pricing in rate cuts by the end of 2023

Market implied policy rates

Source: BlackRock, with data from Bloomberg, as of January 19, 2023.

Equity market positioning for Q1, 2023

After a challenging year for equity markets in 2022, the downward trajectory of inflation and continued economic stability point to a slightly more positive outlook in the coming months. How are these insights shaping our positioning across the global equity landscape?

An expanding global opportunity set

Like the US, the outlook for Europe has started to improve despite core inflation remaining at record highs. A warmer than expected winter has relieved some of the pressure from the energy crisis. Wage growth has also started to come down in Europe as labour markets normalise at an even faster pace than in the US. In China, the economic reopening has quickly taken off. Along with relaxed COVID-19 restrictions, there’s been an easing in common prosperity and antimonopoly regulations. This is an added tailwind to the improving sentiment towards Chinese assets, particularly in sectors like education, internet and real estate that were most impacted by these regulatory initiatives.

Sector positioning for a potential soft landing

Our global portfolios maintain a preference for value vs growth based on continued themes of high rates and inflation followed by a potential soft landing. Notably, we’ve seen a shift in the underlying sectors driving the top down leadership of value. What was previously led by the energy sector has shifted to favour cyclical sectors that have been heavily discounted over the last year, including capital goods, consumer durables, autos and airlines where we’re currently overweight. These are well positioned for a continued high interest rate environment where the economy ultimately avoids a deep recession.

Conclusion

As we enter the next phase in the fight against inflation, market focus has shifted to whether policymakers can achieve a durable decline in inflation without causing a recession. Using alternative data to cut through the noise of hard vs soft landing speculation, we see signs of progress in restoring price stability while maintaining economic strength. At the same time, macroeconomic uncertainty remains high and we expect market volatility to persist as conditions evolve. This makes a data centric investment approach crucial to navigating today’s complex environment, allowing us to remain nimble as investors during a time where dynamism matters most.

Source: BlackRock

Can super secure a woman’s future?

By Robert Wright /March 07,2023/

Here are some stark numbers on the difference between men and women at the point when they retire:

- 80% of women are retiring without the super balance they need to fund a comfortable lifestyle.

- On retirement, women’s average superannuation account balance is around $70,000 less than men.

To be balanced, we should remember there are many situations where the shortfall in a woman’s super balance is offset by them sharing their partner’s super but that assumes away a lot of life possibilities – particularly divorce and the early death of a male partner – and also a woman’s sense of financial independence.

Women also live longer than men. A woman who was 45 in 2020 could expect to live till 86 – that’s three years longer than her male counterpart. So female retirees are more exposed to the dreaded FORO – fear of running out.

Why the shortfall?

Why do women have less super than men? There are multiple often intertwined answers.

More women work in low paid fields like hospitality and care services. They’re also more likely to work part time. That’s one reason the lockdowns of the past two years did more damage to female balance sheets.

Many women take time out of the workforce to have children and act as principal caregiver, especially during the early years of their children’s lives. The ASFA (Association of Superannuation Funds of Australia) estimates women accumulate a ‘super baby debt’ of up to $50,000 – they have $50,000 less in their super because they’ve prioritised children. Compulsory super is based on a percentage of your earnings being saved for retirement. So the less you earn over your lifetime the less you save.

Women are also more likely to have time away from work to care for their parents. If Generation X is the ‘squeezed generation,’ looking after the generation before and after, then Generation X women may be the ones squeezed hardest.

Expanding knowledge, shrinking the gap

Closing the knowledge gap is nearly as important as closing the contribution gap.

The first step is understanding where you stand – so checking with your super fund or adviser to understand exactly how much super you have and how much you’ll need to support a comfortable lifestyle.

Many super fund managers have easy to use calculators that answer those questions. For a rule of thumb, ASFA suggests single people need $545,000 in retirement savings to fund a comfortable retirement. Couples need around $640,000. Obviously these numbers are only guides and assume that you fully own your own home at retirement. It’s important you consider your own situation and expectations.

The calculators we discuss above can give you an individual view of the return difference between different investment strategies. Historically, funds that invest more aggressively (i.e. with more in shares and property and less in cash) have tended to outperform over the long term* and that means more money to retire on.

The more you put in…

Women seeking to set themselves up for a truly comfortable retirement need to first get a handle on their super and their retirement objectives, then accustom themselves to taking a little more risk in the investment strategy.

Given that it’s highly tax effective, many would argue that women should be pouring as much money into super as they can afford. Obviously that decision is a highly personal one that must take account of a whole range of factors. Fortunately, Australian governments, left and right, are committed to making super work, so there are some excellent strategies women of all income levels can use to get more gold into their pot. Here’s a very concise look at some of those opportunities.

How you can retire with more

1. Make additional contributions

Simply put, women who are likely to take time out of work should weigh up the benefits of putting more money into super when they can to build up a retirement savings buffer.

Firstly, make sure your employer is contributing in line with their Superannuation Guarantee responsibilities – currently, they need to contribute 10.5% of your income to super on your behalf. (There’s a cap of $27,500 a year on these so called concessional contributions). You can also make salary sacrifice contributions, where you forgo income and direct it into your super. Those contributions also count towards the $27,500 limit.

If you don’t reach the cap in a given year, you can accumulate those unused portions for up to five years. When you have the funds available you can then ‘catch up’ by investing up to your annual $27,500 cap and any unused cap from previous year(s). You can’t use this catch up approach if your super balance is over $500,000 but for many women it’s an excellent way to consider adding to their super even if they’ve had a few years out of the workforce or on part time income.

2. Bring forward contributions

You can also make non-concessional contributions of up to $110,000 a year into your super. These are contributions you make after tax, for example from your savings. For younger women in high paying jobs, putting extra money into super, perhaps by investing a bonus, inheritance or proceeds from a property sale – may be an effective way to load up your super. Or if you do it later in your career, it’s another way to catch up.

The government also allows you to ‘bring forward’ some contributions investing up to three times the annual non-concessional contribution in one year – that’s $330,00. Again, if you have the funds, it may be a good way to make a focused push at increasing your super balance. As of July 2022, this option is available to any women under 75 (previously it was 67). So even women very close to retirement can use this strategy to improve their super situation.

3. Spouse contributions

Couples working together on their super strategies can make up for some of the inherent disadvantages women face when saving for retirement.

Spouse contributions can be part of that approach. They allow one member of a couple to contribute up to $3,000 into the super fund of their spouse and receive a tax offset of up to $540 for doing so. The offset works on a sliding scale depending on the income of the ‘receiving’ spouse. To get the maximum offset the receiving spouse must earn less than $37,000 and there’s no offset once they earn over $40,000, but for many women, beefing up their super via extra contributions may be even more valuable than a tax offset.

Playing as a team

Couples that work together to accumulate the maximum possible super balance can have more flexibility and options in retirement.

One way couples can do this is through managing their individual $1.7 million super balance cap. The cap limits the amount of super you can transfer into a tax-free retirement income stream such as a super pension or annuity.

A twisty path to a beautiful place

As you can see from this list of contribution strategies, there are numerous ways in which women can maximise their super balance and therefore improve their chance of a comfortable retirement lifestyle. But there are also a plethora of limits, caps and complexities to navigate.

*Past performance is not indicative of future performance.

Source: Perpetual