Tag Archives: Wealth Accumulation

What happens to your super when you retire?

By Robert Wright /November 21,2025/

Superannuation is one of the important pillars of savings in retirement for most Australians. After years of working and contributing to your super fund, retirement is when you are finally able to access it. Whether retirement is just around the corner or still a few years away, it’s worth understanding your options.

In this article, we’ll walk you through your options on what do with your super when you retire, how is it taxed and what happens if there’s any left when you pass away.

When can you access your super?

You can usually access your super when you reach your preservation age (currently age 60) and retire. Alternatively, you can start accessing it once you turn 65, even if you’re still working.

There are other special circumstances where you might be able to access it earlier, like severe financial hardship or permanent disability but generally speaking, retirement is the key trigger.

Your options once you have access to your super

Once you retire and meet a condition of release, your super becomes accessible for you to withdraw but that doesn’t necessarily mean you have to withdraw and use all of it.

You’ve got a few main options and you may prefer a combination of these:

- Leave it in your super fund (Accumulation phase)

Yes, you can actually choose to leave your super where it is, in its accumulation phase even after you retire.

If you don’t need to access the money straight away, you can leave your super invested in the fund’s accumulation account. Your money can keep growing (taxed at 15% on earnings) and you can access it when you’re ready.

So, while this may suit short-term plans, it may usually not be the most tax effective option when compared to other options like starting a superannuation pension in retirement, which is often tax free and funded with money from your superannuation savings.

- Take a lump sum

Where access to funds is required, you may prefer withdrawing a lump sum from super. This can help you in various ways like paying off a mortgage, clearing credit cards or personal loan debt, covering medical costs, funding travel expenses or investing elsewhere (e.g. property, shares outside of super).

However, this decision should be carefully considered as withdrawing a lump sum or lump sums can reduce how long your super lasts. It’s also worth considering how that money will be managed outside super, as it may be subject to different tax treatment or may impact any Centrelink entitlements like the Age Pension.

- Start a superannuation pension (account-based income stream)

An account-based pension lets you convert your accumulated super into a regular income stream. However, once an income stream is started with a set balance, you cannot add more monies to the ongoing account-based pension unless the pension is commuted and restarted again. If you need access to your superannuation savings, starting an income stream is a popular option which can be tax effective.

Where access to the super savings is required, an income stream can be a good option because:

- You can receive regular and flexible payments (monthly, quarterly, etc).

- You can choose how much to set as regular income for your pension payment (subject to government set minimum limits).

- Earnings are tax free once you’re in pension phase.

- Payments can be adjusted as your needs change.

- You keep control over your investment strategy.

You can still withdraw lump sums if needed but many people like the idea of a steady income, much like a salary. However, consider that the ongoing income payments can reduce your account balance over time.

- Can a lifetime annuity help?

One of the biggest concerns for retirees is running out of money.

If you want income for life, no matter how long you live, lifetime income streams such as a lifetime annuity can help you achieve that.

Unlike an account-based pension (which relies on how long your money lasts), a lifetime annuity is more like an insurance product. You invest a lump sum from your super and in return, receive a regular income for the rest of your life.

Some retirees consider using a combination of a pension and an annuity – the pension provides flexibility and the annuity can provide peace of mind. However, lifetime annuities are designed to be held for life. Although there may be flexibility to access a lump sum if needed, there may be break cost considerations.

Can I combine these options?

Absolutely and many retirees choose to do so.

You might prefer to consider:

- Leaving some of your super invested in accumulation phase.

- Taking a lump sum to pay off debts.

- Starting a super pension to draw regular income.

- Using part of your super to start a lifetime annuity.

The right mix will depend on your lifestyle, goals, health, family situation and other sources of income, including the Age Pension. There are many more options we have not discussed.

The Age Pension and Super: How they can work together

The Age Pension is a government payment designed to help eligible Australians in retirement. As of 2025, you can apply for the Age Pension from age 67.

There are also concessions and benefits that come with it, such as reduced utility bills and medical costs, so it’s well worth checking your eligibility.

Eligibility is also based on your means – your income and assets. Centrelink includes your super in the assets and income tests. However, the assessment can differ if your super is converted into an income stream like a lifetime annuity.

Age Pension, combined with other sources of super based income like an account-based pension and/or a lifetime annuity, can help make your money last longer. It acts as a safety net if your super runs down over time. This can be a powerful way to stretch your retirement savings further.

How is my super taxed when I retire?

The earnings on your super are usually taxed at a maximum rate of 15% whilst the super remains in accumulation phase. Where an account-based pension is started, the earnings in the pension phase are tax free.

If you’re age 60 or over, any withdrawals from your super (lump sum or income) are usually tax free if you’ve permanently retired.

However, if you’re under 60 or receiving certain types of benefits (like defined benefit pensions), tax rules may be a little different. It’s worth speaking to a financial adviser to understand your situation.

How do I make my super last?

Australians are living longer than ever, and therefore it is important to strategise and ensure that your retirement savings can last for a long time.

Here are a few strategies to consider:

- Budget and plan – Work out how much income you need as opposed to how much you want. Consider your spending habits and lifestyle goals to help ensure you don’t withdraw more than you need. Work out how long your super will last.

- Stay invested – Your money doesn’t have to stop working for you when you retire. Draw appropriate amounts based on your retirement objectives and consider keeping the balance invested in an option that suits your risk tolerance and goals.

- Mix your income sources – Layering your income can help your super last longer. One way you could consider meeting your essential expenses throughout retirement, the Age Pension can work together with a secure, lifetime income stream, such as a lifetime annuity, to provide regular income payments for life. Once your essential expenses have been met through a combination of the Age Pension and a lifetime income stream, you could meet your additional desired expenditure goals with income from an account-based pension.

- Review your investments – Ensure they match your risk tolerance and income needs in different phases of your retirement.

What happens to my super when I die?

If you don’t use all your super before you pass away, the remaining balance is generally paid out to your beneficiaries, either as a lump sum or income stream (depending on your instructions and their eligibility) or your estate.

This is known as a death benefit and it can be left to your spouse or partner, your children, certain dependant or interdependents or your estate. It can either be paid as a lump sum or can be paid as an income stream. The tax treatment depends on who receives the benefit. For example, a lump sum payment to a spouse is tax free.

To make sure your wishes are followed, it’s important to nominate your beneficiaries with your super fund. You can make a binding death benefit nomination to ensure your super goes exactly where you want it to. Otherwise, your super fund will decide (within legal guidelines).

Steps toward a stronger retirement

Super can be one of the most flexible and tax effective ways to fund your retirement but simply reaching retirement age doesn’t mean your financial decisions stop. In fact, how you choose to access and manage your super can shape your lifestyle for decades to come.

Whether you choose a lump sum, a regular income or a combination, planning ahead is essential. Think about how long your money needs to last, how to make the most of your tax benefits and how to combine super with other income sources like the Age Pension. A financial adviser can help you tailor your retirement needs with the right options.

Super is more than just savings. The right strategy can help your super last longer, support your quality of life, and give you peace of mind.

Source: Challenger

Navigating market volatility

By Robert Wright /May 23,2025/

Financial markets have been erratic lately, understandably causing some concern for those of us with super and investments. While dips and major market events are a common feature of investing, markets generally trend upwards over time.

Most super funds invest in sharemarkets to help your money grow over in the long term. So when markets see-saw, so do super and investment balances and returns.

While this can be worrying, it’s important to remember that although the value of investments may go up and down at different times, markets tend to recover and grow over the long term. So it’s important to keep your long-term investment goals in mind.

What’s happened recently?

On 3 April, President Donald Trump announced the US would place tariffs on goods imported into the US from countries around the world. This included a 10% tariff on goods from Australia, which was the minimum rate announced on the day.

Major global economies and markets had been preparing for the announcements, but the tariffs imposed on some countries were bigger than expected. Other countries have also responded by putting similar tariffs on US goods coming into their markets.

As a result, share markets in the US and elsewhere fell sharply in the days afterwards, including the Australian Stock Exchange.

What is a tariff?

A tariff is a tax added to the cost of goods imported from a particular country or countries. It is paid to the government where the goods are being imported.

Tariffs are often used to protect domestic industries by increasing the price of foreign-made competitor products, or to raise revenue.

The cost of those items to the public will generally increase by a similar amount to the tariff.

What does this mean for markets and investments?

The US tariffs are expected to slow global trade and push up the price of some things, which could cause inflation to rise.

This could result in the Reserve Bank of Australia cutting the interest rate several times this year to prevent the economy from slowing down too much.

In the short term, you may see a negative effect on the performance of investments.

Short term volatility in response to political announcements and other geopolitical events is a common feature of investment markets.

While difficult to forecast, history shows us that markets do recover from disruptive influences – for example, from the Global Financial Crisis and the COVID-19 pandemic.

What led to this?

Since Trump’s second presidency began, uncertainty has emerged about US policy in the areas of tariffs, defence and other critical areas of government spending.

In recent months, shares have been quite weak, particularly US technology stocks. This group of stocks was optimistically priced after two years of strong growth, and therefore most at risk of uncertainty in the US market.

This has unsettled businesses amid concerns the US economy could slow. It has also fed into uncertainty in global investment markets, including the Australian sharemarket.

What does this mean for me?

As global financial markets move up and down, the value and returns of your super and investments may also change in the short term.

While this can be concerning, history shows that markets rise over time. So it’s important to keep your long-term savings and investment goals in mind and carefully consider before making any changes to your investment strategy.

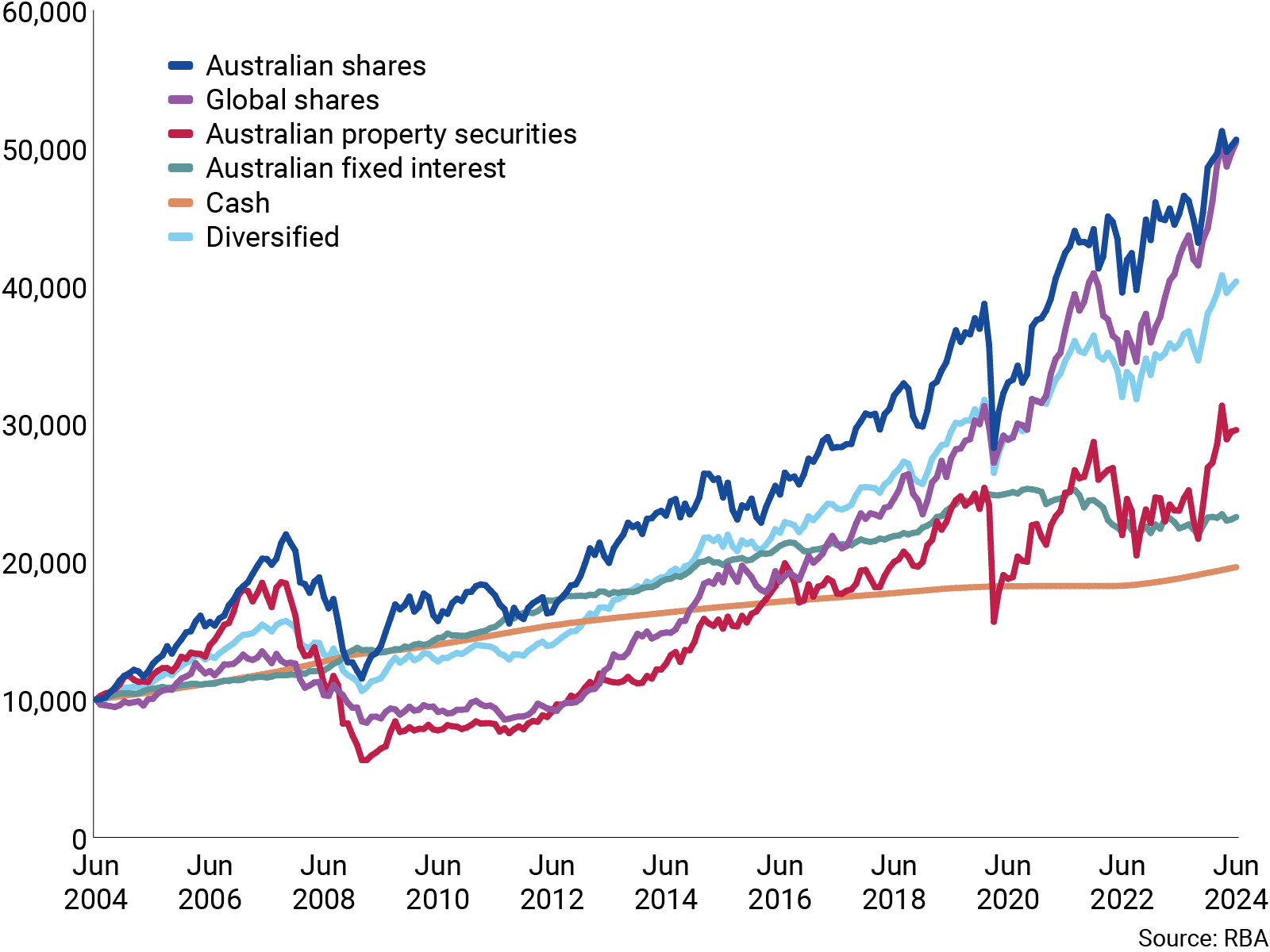

It’s understandable at times like these that some members think about changing how their money is invested. As this chart shows, the long-term trend across major investment types is positive, with shares experiencing more volatility but generating higher returns than more conservative options such as cash.

While past performance is not a guarantee of future performance, historically more time invested in the sharemarket has meant a higher return on investment.

How different investment types have performed over 20 years

It’s also worth noting that investment performance has generally been strong over the past two years, meaning the value of your investments or super may have been relatively high.

Do I need to do anything?

As with any significant market event, it’s best to avoid impulse reactions, but to take a long-term view.

Source: CFS

Spouse super contributions – what are the benefits?

By Robert Wright /May 23,2025/

If your partner is earning a low income, working part-time, or currently unemployed, boosting their super could be a smart financial move for both of you.

When your partner isn’t earning much, or is out of work, their super might not be growing enough to support them in retirement. By contributing to their super, you may not only help them but also enjoy some tax benefits yourself.

We’ll explore how the spouse contributions tax offset works and how it differs from contribution splitting.

The spouse contributions tax offset

Are you eligible?

To be entitled to the spouse contributions tax offset:

- You need to make a non-concessional contribution to your spouse’s super. This means you add money from your after-tax income and don’t claim a tax deduction for it.

- You must be married or in a de facto relationship together and are not living apart or separately.

- You must both be Australian residents.

- Your spouse’s income should be $37,000 or less for the full tax offset, and under $40,000 for a partial tax offset.

- Your spouse is under 75 years of age, and their total superannuation balance is less than the general transfer balance cap ($1,900,000 for 2024-25) as at 30 June of the prior year.

What are the financial benefits?

If eligible, you can generally make a contribution to your spouse’s super fund and claim an 18% tax offset on up to $3,000 through your tax return.

To be eligible for the maximum tax offset, which works out to be $540, you need to contribute a minimum of $3,000 and your partner’s annual income needs to be $37,000 or less. If their income exceeds $37,000, you’re still eligible for a partial offset. However, once their income reaches $40,000, you’ll no longer be eligible for any offset, but can still make contributions on their behalf.

Are there limits to what can be contributed?

You can’t contribute more than your partner’s non-concessional contributions cap, which is $120,000 per year for everyone, noting any non-concessional contributions your partner may have already made.

However, if your partner is under 75 and eligible, they (or you) may be able to make up to three years of non-concessional contributions in a single income year, under bring-forward rules, which would allow a maximum contribution of up to $360,000.

Another thing to be aware of is that non-concessional contributions can’t be made once someone’s super balance reaches $1.9 million or above as at 30 June 2024. So you won’t be able to make a spouse contribution if your partner’s balance reaches that amount. There are also restrictions on the ability to trigger bring-forward rules for certain people with large super balances (more than $1.66 million in 2024-25).

There are also different super balance limits in place if you want to take advantage of the bring-forward rules.

How contributions splitting differs

Another way to increase your partner’s super is by splitting up to 85% of your concessional super contributions with them, which you either made or received in the previous financial year. Concessional super contributions can include employer and or salary-sacrifice contributions, as well as voluntary contributions you may have claimed a tax deduction for.

What rules apply for contribution splitting?

To be eligible for contributions splitting, your partner must be between age 60 (preservation age) and 65 (and not retired).

Are there limits to how much can be contributed?

Amounts you split from your super into your partner’s super will count toward your concessional contributions cap, which is $30,000 per year for everyone.

On top of this, unused cap amounts accrued in the last 5 years can also be contributed, if they’re eligible. Note, this broadly applies to people whose total super balance was less than $500,000 on 30 June of the previous financial year.

Do all super funds allow for this type of arrangement?

You’ll need to talk to your super fund to find out whether it offers contributions splitting, and it’s also worth asking whether there are any fees.

What else you and your partner should know

- If either of you exceeds super contribution caps, additional tax and penalties may apply.

- The value of your partner’s investment in super, like yours, can go up and down, so before making contributions, make sure you both understand any potential risks.

- The government sets rules about when you can access your super. Generally, you can access it when you’ve reached age 60 (preservation age) and retire.

- While you can’t personally make further non-concessional contributions into your super once you have a total super balance of $1.9 million or above (as at 30 June of the previous financial year), it’s still possible to make contributions to your partner’s super (noting the caps).

Where to go for more information

Your circumstances will play a big part in what you both decide to do. And, as the rules around spouse contributions and contributions splitting can be complex, it’s a good idea to chat to your financial adviser to make sure the approach you and your partner take is the right one.

Source: AMP

The ins and outs of geared share funds

By Robert Wright /February 28,2025/

Geared share funds are high risk and high reward. When share markets are doing well, the returns can be very high, but the opposite is also true. We look at the pros and cons, and the role of geared share funds in a diversified investment strategy.

Geared share funds can be a great way for investors to invest in shares – and share in the rewards – when the share market performs well over long periods of time.

Geared share funds magnify both positive and negative returns, so they’re considered high risk, high return investment options.

But exactly what is a geared share fund, and are they for everyone?

Let’s take a look at the ins and outs of this unique investment option.

What is a geared share fund?

Geared share funds accept money from investors and borrow money to invest alongside investors’ capital. The fund uses the pool of investors’ money and borrowed money to buy shares.

They amplify both positive returns and negative returns on the shares in which the fund invests.

On the upside, geared share funds generate higher returns than overall share market returns when markets are rising. Conversely, the value of your investment will drop further than equivalent investment options without internal gearing.

They are best explored as part of a long term, diversified investment strategy.

How do geared share funds work?

When you invest money in a geared share fund, the fund will borrow money to invest on your behalf, alongside your investment.

For example, for every $1,000 you invest in the fund, the geared share fund may borrow another $1,000. That would give you $2,000 of exposure to the shares in which the fund invests. So in addition to the returns generated from your capital, you also receive all the returns from the borrowed funds (less the cost of borrowing).

The fund’s gearing, or borrowing, effectively magnifies the returns of the underlying investments, whether they are gains or losses.

Geared share funds generally perform well when the share market is growing at a higher rate than the interest charged on borrowed money.

Geared share funds borrow at institutional interest rates, which are generally lower than those offered to individual investors.

Pros of geared share funds

- The gearing, or borrowing, is done within the fund: unlike a margin loan, the fund, rather than the investor, is responsible for repaying its loans. This model allows investors to keep a long term view on their investments, rather than worry about day to day performance of their investments.

- Investor exposure is limited to their invested capital: while the fund borrows on behalf of its investors to buy shares, if the share market falls, and the fund’s loans need to be repaid, individual investors will never lose more than their invested capital.

- Gains are magnified by gearing: when the shares in which the fund invests go up, the return to the investor may be much higher than if they had simply purchased an equivalent fund without gearing.

- Franking credits are magnified by gearing: when a geared fund invests in Australian shares, the gearing will also magnify the level of franking credits payable as part of income distributions.

- Long term gains magnify long term share performance: investors seeking to invest for a decade or more, and who are willing to ride out short term market falls, can do very well with geared share funds. The compounding effect of the additional returns from gearing is very powerful over the long term.

Cons of geared share funds

- Fees are relatively high: fees are charged not just on the $1,000 you invest, but also on the $1,000 that the fund borrows on your behalf. Fees reduce your return.

- Losses are magnified by gearing: when the shares in which the fund invests go down, losses will be much higher than if you simply purchased the same shares with the same initial investment.

- Short term share market falls can lead to big investment losses: investors who need to take out their capital at a particular point in time, or who are not prepared to wait for markets to recover, can suffer big losses if this coincides with a fall in markets.

When to consider geared share funds

Geared funds can play an important role within a diversified portfolio for investors looking for above average investment performance over the long term by accelerating their Australian and/or global share allocations.

Investors who can ride out short term market volatility and do not need to take out their money in the short term, may benefit from the long term returns that geared share funds can offer. Geared funds should therefore be particularly attractive to superannuation investors who cannot access their capital until retirement.

Investors who are risk averse and who may need to cash in their investment in the short term, may not find geared share funds a suitable investment.

Investors should always seek financial advice to ensure investments are suitable for their objectives, investment horizon, and personal circumstances.

Source: CFS